This Artificial Intelligence (AI) Stock Appeared Destined for the $1 Trillion Club. Here's Why It Lost Momentum.

Key Points

Oracle's data centers are highly sought after by artificial intelligence (AI) powerhouses like OpenAI, because of their fast processing speeds and low cost.

Oracle has an order backlog worth $638 billion from customers who are waiting for more data centers to come online, but I see a few issues with that number.

Oracle stock is down 44% from last year's record high, but it isn't necessarily cheap.

- 10 stocks we like better than Oracle ›

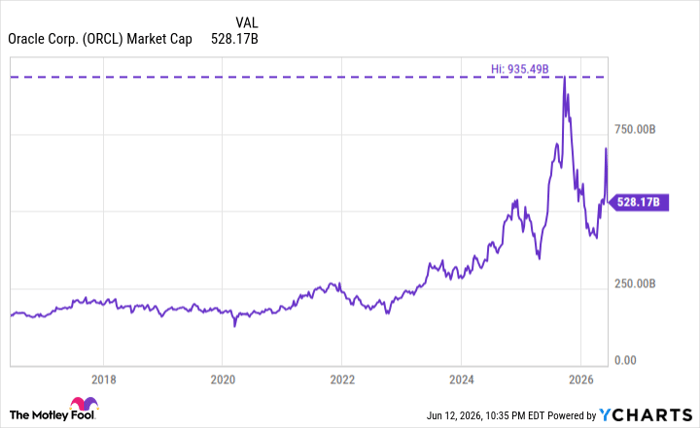

As I write this, 12 publicly listed American companies have a market capitalization of $1 trillion or more, with SpaceX being the newest member of the prestigious club. Software and cloud infrastructure giant, Oracle (NYSE: ORCL), was tantalizingly close to joining them late last year when its market cap topped $935 billion, but its stock has since hit a wall.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

ORCL Market Cap data by YCharts

Oracle operates some of the fastest, and most cost-efficient data centers for artificial intelligence (AI) training and inference workloads, and it has a gigantic order backlog for computing capacity worth $638 billion. However, there is a real possibility that some of Oracle's top customers won't be able to fulfill their obligations, so investors are treading with caution.

Oracle stock is down 44% from its all-time high, and here's why the dip might not be a buying opportunity.

Image source: The Motley Fool.

A leader in the AI infrastructure race

Oracle is building data centers as fast as it can to fill demand for computing capacity from its AI customers, which include OpenAI, Meta Platforms, and Elon Musk's xAI, to name a few. It fills these data centers with thousands of specialized chips called graphics processing units (GPUs), which are supplied by Nvidia and Advanced Micro Devices.

Oracle has a few advantages over other cloud providers. First, it prioritizes automation in its data centers, so it can bring them online much faster than competitors who rely on human-centric infrastructure management. Second, it uses proprietary remote direct memory access (RDMA) networking technology, which shifts data between GPUs faster than traditional Ethernet networks.

These attributes result in faster processing speeds and lower costs, which is a winning combination for AI developers who often pay for computing capacity by the minute.

Oracle has also built some enormous GPU clusters, allowing developers to tap into more than 131,000 of the latest chips from Nvidia and AMD. This is a key reason why companies at the forefront of the AI revolution -- like OpenAI -- use Oracle's infrastructure.

A big chunk of Oracle's backlog is from one customer

Oracle generated $19.2 billion in total revenue during its fiscal 2026 fourth quarter (ended May 31), which was a 21% increase from the year-ago period. Oracle Cloud Infrastructure (OCI) contributed $5.8 billion, which grew at a significantly faster pace of 93%, highlighting the significant demand for data center capacity.

But the headline number in this report was Oracle's $638 billion in remaining performance obligations (RPO), which soared by 363% year over year. RPO reflects the value of signed contracts for services that haven't been delivered yet, so it's similar to an order backlog. Oracle says the $638 billion figure is a good indication of future revenue, but investors should be aware of a few issues.

First, according to a report by The Wall Street Journal from last September, around $300 billion of Oracle's RPO was attributable to OpenAI alone. The start-up raised $122 billion from investors in March, but it only has around $25 billion in annualized revenue and is still posting losses. Therefore, it's unclear how the company will fulfill this enormous commitment to Oracle, especially since it has agreements of similar size with other cloud providers like Microsoft.

Second, Oracle only expects to convert 12% of its RPO into revenue over the next 12 months, followed by a further 34% in the 24 months after that. In other words, less than half of its RPO could become actual revenue over the next three years, which is a very wide window in an industry moving as quickly as AI. Since we are already witnessing cracks in the demand picture, RPO might not be the best indicator after all.

Third and finally, Oracle is carrying over $122 billion in long-term debt, and it just announced plans to raise another $40 billion through a mix of debt and equity. The company is investing heavily to build more AI data centers, which creates a risky situation for investors if that big RPO number doesn't turn into revenue.

Oracle stock looks fairly valued

Oracle generated generally accepted accounting principles (GAAP) earnings of $5.83 per share during fiscal 2026, placing its stock at a price-to-earnings (P/E) ratio of 31.6. That is a slight discount to the Nasdaq-100 index, which trades at a P/E of 34.6, so Oracle might be close to fair value relative to a basket of its big-tech peers.

However, Wall Street is only forecasting 7.7% earnings growth in fiscal 2027, so there might not be a whole lot of room for upside in its stock over the next 12 months. The Street is expecting much faster growth of 45.7% in fiscal 2028, but it's tough to rely on that prediction with any confidence right now given some of the issues I highlighted earlier.

In summary, investors might want to take a wait-and-see approach to Oracle. If the company continues to deliver positive results over the next few quarters, then there might be an opportunity to take a long-term position in its stock at the right price.

Should you buy stock in Oracle right now?

Before you buy stock in Oracle, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Oracle wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $433,268!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,259,391!*

Now, it’s worth noting Stock Advisor’s total average return is 935% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 14, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool has a disclosure policy.

Recommended Articles