Fed June Rate Decision Preview: Stubborn Inflation Fuels Hawkish Expectations, How Will US Stocks, Dollar and Gold React?

TradingKey - The Federal Reserve is scheduled to hold its FOMC meeting from June 16 to 17, Eastern Time, and will release its interest rate decision and updated economic projections on June 17. The current target range for the federal funds rate is 3.50% to 3.75%. Given the latest U.S. CPI and non-farm payroll data, the most likely outcome of the June meeting is to maintain interest rates unchanged while signaling a more hawkish policy stance.

The latest U.S. non-farm payroll data shows that 172,000 jobs were added in May, significantly exceeding market expectations. The unemployment rate held steady at 4.3%, while average hourly earnings rose 0.3% month-on-month and 3.4% year-on-year. Furthermore, employment figures for March and April were upwardly revised by a combined 93,000. The labor market's continued resilience suggests the Federal Reserve sees no immediate need to cut interest rates prematurely to support the economy.

Subsequently, the latest U.S. CPI data for May revealed a month-on-month increase of 0.5%, pushing the year-on-year figure to 4.2%, up from 3.8% in April. Energy prices surged 3.9% month-on-month and 23.5% year-on-year, with gasoline prices spiking 7.0% monthly and 40.5% annually. This indicates a resurgence in U.S. inflation, primarily driven by energy shocks linked to tensions in the Middle East, rising oil prices, and transportation risks.

However, the structure of the CPI is not entirely out of control. Core CPI in May rose 0.2% month-on-month, lower than April's 0.4%, while the year-on-year core rate edged up slightly to 2.9% from 2.8% in April. For the Federal Reserve, this suggests that while inflationary pressures remain high, they currently resemble an energy-driven supply shock rather than a total loss of control over core services and the wage-price spiral. Consequently, the Fed has reason to remain cautious rather than hiking rates immediately.

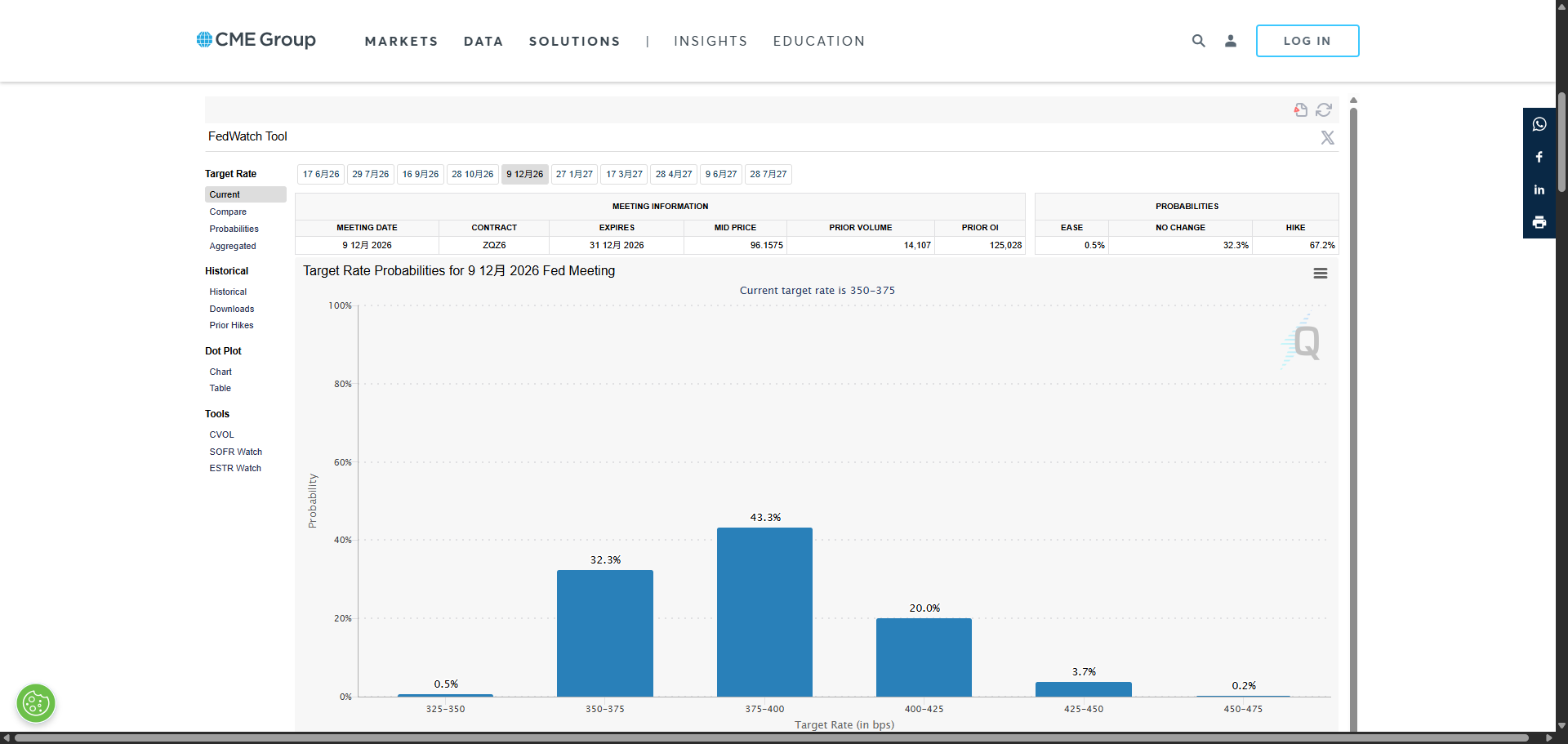

For investors, the primary focus regarding the June FOMC decision should be on the policy statement, the dot plot, and the Chairman's press conference. Investors should watch for the removal of previous language leaning toward rate cuts and whether the dot plot shows more officials supporting a rate hike this year. According to the CME FedWatch Tool, following the CPI release, the market's implied probability of a rate hike in June and July remains below 2%, though expectations for a hike later in the year persist, with the probability of a December move still exceeding 60%.

Market expectations for Fed interest rates, Source: CME Group

How did U.S. stocks, the U.S. dollar, and gold react in the short term following the Federal Reserve’s June interest rate decision?

For U.S. stocks, the base-case scenario is that pressure outweighs surprises. If the Fed maintains interest rates but removes its easing bias, upwardly revises inflation forecasts, and hints that rate hikes remain possible this year, high-valuation tech stocks and the AI sector may continue to face pressure, and the Nasdaq will continue its correction. U.S. stock valuations are currently high, and the market is sensitive to rising interest rates. If the Fed adopts a dovish tone, highlighting cooling core CPI, U.S. stocks might see a short-term bounce; however, as long as rate-cut expectations are not restored, any rebound is more likely to be a technical recovery rather than a trend resumption.

Nasdaq Index Weekly Chart, Source: TradingView

For the U.S. dollar, robust employment and CPI data remain supportive. If the Fed shifts toward a 'hawkish pause,' the U.S. Dollar Index is likely to remain strong, especially relative to currencies with low growth and low interest rate expectations. The dollar is only likely to retreat if the Fed explicitly emphasizes that energy inflation is a transitory shock and downplays the risk of rate hikes this year.

Gold Price Weekly Chart, Source: TradingView

For gold ( XAUUSD ), rising inflation is inherently positive for gold's inflation-hedging properties, but the market is currently more focused on real interest rates. If the Fed sends more hawkish signals, driving up Treasury yields and strengthening the dollar, the opportunity cost of holding gold will rise, and gold prices may continue to face downward pressure, retesting the $4,000 psychological level or even falling to the $3,900 support level. Conversely, if the Fed emphasizes cooling core inflation and sets aside rate-hike considerations, real rates could fall, and gold may stage a corrective rebound.

Recommended Articles