Boom or Bubble? This Is Where Micron Technology Stock Could Be in 5 Years

Key Points

The memory industry that Micron Technology serves has experienced boom-and-bust cycles in the past.

However, the ongoing boom in the memory industry seems durable, primarily due to the huge supply gap created by AI.

Micron could easily beat Wall Street's growth expectations and soar nicely over the next five years.

- 10 stocks we like better than Micron Technology ›

The memory industry has been booming for the past three years, propelled by the proliferation of artificial intelligence (AI), which has created demand for larger, faster memory across multiple applications.

Micron Technology (NASDAQ: MU) has been a major beneficiary of the memory boom. Micron stock has shot up by 935% over the past three years, driven by a big jump in its revenue and earnings. Investors, however, may now be wondering if the memory specialist has now entered bubble territory, especially considering that it has been historically susceptible to oversupply in the memory industry that has seen its share of boom and bust cycles.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

For example, Micron had a forgettable fiscal 2023 (which ended in August 2023). Its revenue halved that year, and it swung to a loss, driven by a drop in demand for smartphones and personal computers (PCs) that led to an oversupply of memory chips. The supply glut led to a sharp decline in memory prices in 2023, which explains why investors may be worried about a similar scenario unfolding in the future.

But will that indeed be the case? Or will the memory market continue to benefit from the robust investments in AI data centers, fueling more upside in Micron stock over the next five years? Let's find out.

Image source: Micron Technology.

The ongoing memory boom cycle is durable

The current memory boom seems long-lasting. Running AI workloads in data centers requires faster and bigger memory chips to ensure that various types of chips can perform their tasks optimally. For instance, a graphics processing unit (GPU) will not work at its full potential if it doesn't receive the required data set quickly. This explains why AI data centers rely on high-bandwidth memory (HBM) chips, which move huge volumes of data rapidly while keeping energy consumption in check.

Not surprisingly, HBM demand has simply taken off. According to a third-party estimate, HBM revenue could increase by 58% in 2026 to almost $55 billion. The size of the HBM market could reach an estimated $130 billion by 2030, suggesting the current memory boom is indeed durable. What's more, the incredible demand for HBM is straining the availability of memory chips needed in other applications, such as smartphones and PCs.

Tom's Hardware noted in an article in December 2025 that HBM consumes nearly thrice the wafer capacity of the traditional DDR5 dynamic random-access memory (DRAM). Memory manufacturers have been prioritizing HBM over DRAM, which is quite logical considering that data centers are poised to consume 70% of the memory supply this year.

Also, the long-term growth forecast for HBM suggests that data center demand will continue to dominate the memory industry. In fact, Micron's customers are already entering into long-term supply agreements lasting up to five years, as they look to secure their future needs. Given that HBM consumes far more wafer capacity than conventional DRAM chips used in smartphones and PCs, it is easy to see why industry watchers believe the shortage of memory chips will last until 2030.

Of course, memory manufacturers are investing in new fabrication facilities to fill the supply shortage. However, building a new fabrication plant is a long process that could take two to four years, according to various estimates. So, there isn't a quick fix to the supply constraint the memory industry is facing, which means the favorable pricing environment powering Micron's stunning growth is sustainable.

Micron Technology stock could make investors significantly richer over the next five years

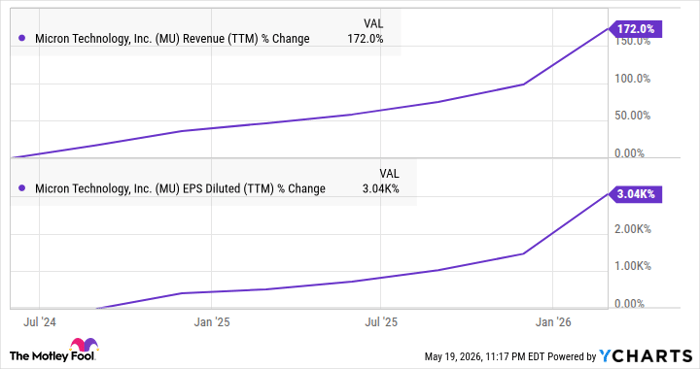

Micron Technology returned to revenue growth and profitability from 2024 and has witnessed a solid surge in these metrics over the past couple of years.

Data by YCharts

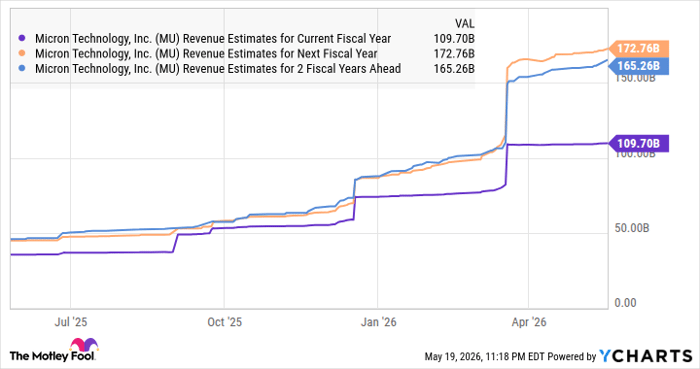

The secular growth of the memory market suggests it still has room to grow. Analysts are expecting its revenue to nearly triple in the current fiscal year (which will end in August 2026) from last year's reading of $37.4 billion.

Data by YCharts

The forecast for next year is quite solid as well, though a dip is anticipated in fiscal 2028. But that is unlikely to be the case due to the reasons discussed above. Even if memory manufacturers build enough capacity to meet HBM demand from AI data centers, they will need to increase supply to meet the pent-up conventional memory demand for smartphones and PCs.

I say this because the memory supply constraint and higher prices are leading to sharp drops in smartphone and PC shipments. As such, Micron's revenue growth is unlikely to slow down after next year. Assuming that the company's top line grows at a conservative annual rate of 15% in fiscal years 2028, 2029, and 2030, its revenue could reach $263 billion after five years (using the next fiscal year's estimate of $172.8 billion as the base).

If Micron trades at 5.5 times sales after five years (in line with the tech-focused Nasdaq Composite index's sales multiple), its market cap could reach $1.45 trillion in five years. That's a potential jump of 83% from current levels. However, this AI stock could easily deliver much bigger gains as it should ideally trade at a premium valuation given the healthy growth it is likely to deliver through 2030.

Should you buy stock in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $475,063!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,369,991!*

Now, it’s worth noting Stock Advisor’s total average return is 994% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 22, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

Recommended Articles