【US Pre-Market】Three Major Futures Decline Across the Board, Memory Chip and Optical Communication Sectors Weaken, ADP and Warsh Speeches Debut Together

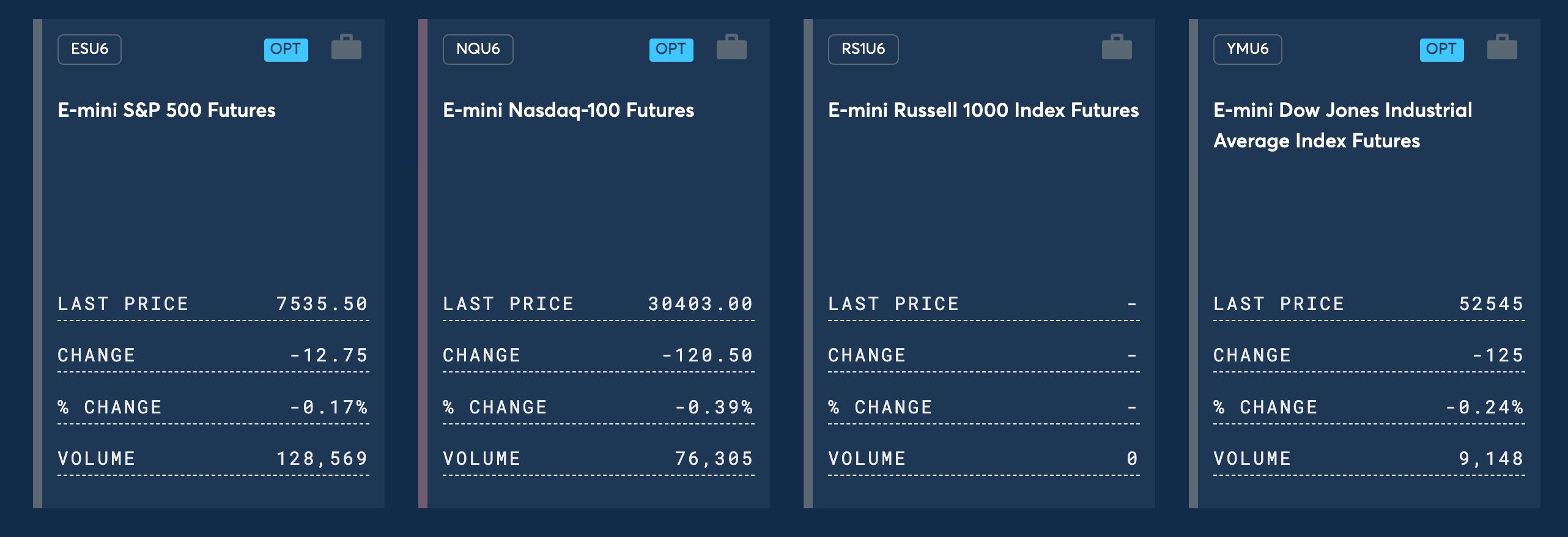

TradingKey - On July 1, Eastern Time, during pre-market trading, the three major US stock index futures fell collectively. As of press time, Dow Jones Industrial Average futures fell 0.24%, S&P 500 index futures dropped 0.17%, and Nasdaq 100 index futures slid 0.39%. Overall market sentiment was weak, with the semiconductor and storage sectors acting as the main drag on the broader market.

[Source: CME Group]

Asia-Pacific stock markets closed mixed today. The Nikkei 225 Index closed up 0.59% at 70,474.96 points; South Korea's KOSPI Index closed down 2.04% at 8,303.41 points, weighed down by heavyweights Samsung Electronics, which fell 5.8%, and SK Hynix, which fell 3.4%; Taiwan's Weighted Index closed up 1.94% at 47,018.99 points.

In commodities, gold and silver prices extended their declines. As of press time, spot gold ( XAUUSD) was trading at $3,990 per ounce, having dropped over 1% at one point during the day; spot silver ( XAGUSD) was at $58.06 per ounce, down about 0.9%.

International oil prices continued to slide. As of press time, WTI crude oil futures were trading at $68.69 per barrel, down nearly 1.18%; Brent crude oil futures were at $72.15 per barrel, down about 1.1%. Both hit their lowest levels since February 27. Influenced by indirect technical talks held between US and Iranian officials in Doha today, market concerns over the Middle East situation eased, putting downward pressure on oil prices.

In the crypto market, Bitcoin fell below the $59,000 mark. As of press time, it was trading at approximately $58,597 per coin, while Ethereum was at $1,572 per coin. The US Dollar Index edged slightly higher, trading around 101.34.

Unusual Market Movements

The memory chip sector continued to edge lower pre-market. Affected by "Big Short" Michael Burry's disclosure of a new round of short bets on the AI and semiconductor sectors, coupled with the ongoing fermentation of class-action lawsuits against Samsung, SK Hynix, and Micron ( MU ), as of press time, Micron Technology fell over 2% pre-market, SanDisk ( SNDK) fell nearly 4%, and Seagate Technology ( STX) fell nearly 1.5%.

The optical communications sector weakened pre-market. Corning ( GLW) experienced profit-taking for two consecutive days after surging 15.67% on Monday to hit a historic high, at one point falling over 5% pre-market, now narrowing to a 2.3% decline. Marvell Technology ( MRVL) fell about 1.6%, and Coherent ( COHR) and Lumentum ( LITE) fell nearly 1.5%.

As for Big Tech, during pre-market trading, Microsoft ( MSFT) rose over 1.5%, with reports indicating that Microsoft is planning a new round of layoffs; SpaceX ( SPCX) rose 1.69%; Meta ( META ), Tesla ( TSLA ), Apple ( AAPL ), and Nvidia ( NVDA) remained virtually flat.

Nike ( NKE) fell 3.3% pre-market to $39.68. The company's fourth-quarter revenue was $10.97 billion, beating analyst expectations of $10.86 billion; adjusted earnings per share were 20 cents, beating the expected 13 cents; net income increased from $211 million in the same period last year to $1.07 billion, primarily driven by a one-time benefit from tariff refunds. However, revenue in the Greater China region declined year-on-year, marking the eighth consecutive quarter of negative growth.

Market News

Fed Chair Warsh's "debut" at the global central banking forum. According to the official schedules on the websites of the Federal Reserve and the European Central Bank, at 21:00 Beijing time tonight, Fed Chair Warsh will attend the "Policy Panel" event and deliver a speech at the European Central Bank's Forum on Central Banking in Sintra, Portugal. Joining him on the panel will be ECB President Christine Lagarde, Bank of England Governor Andrew Bailey, and Bank of Canada Governor Tiff Macklem. This marks Warsh's first public appearance on the international stage since taking office, and the market is highly focused on his latest statements regarding the inflation outlook and the interest rate path.

US and Iranian officials hold indirect talks in Doha today. On July 1 local time, US and Iranian officials held indirect technical talks in Doha, the capital of Qatar, with Qatar and Pakistan serving as mediators. Affected by this, international oil prices continued to slide, with both WTI and Brent crude hitting new lows since February 27.

"The Big Short" Michael Burry discloses new round of short bets on AI and semiconductors. Michael Burry, the real-life inspiration behind the movie "The Big Short," disclosed a new round of bearish bets on Tuesday, building short positions around the artificial intelligence and semiconductor sectors. In a Substack post, he stated that he shorted Tesla at $416.22, while also establishing new short positions against Nvidia, Applied Materials ( AMAT) and the iShares Semiconductor ETF ( SOXX ). Burry has previously warned multiple times about bubble risks in the AI boom.

Tesla's Q2 delivery data to be released after today's market close; market focuses on whether sales can beat expectations. The consensus analyst expectation compiled by FactSet is approximately 465,000 vehicles, higher than the 444,000 vehicles in the same period last year. This data will directly test the effectiveness of Tesla's balance between price-cut promotions and market demand, and will also influence investors' judgment of the overall demand in the electric vehicle industry. Tesla's stock price has continued to rise recently, surging more than 8% on Monday.

SoftBank completes $10 billion follow-on investment in OpenAI. SoftBank Group announced in a statement on July 1 that it had completed a $10 billion follow-on investment in OpenAI on that day through the SoftBank Vision Fund 2, and plans to complete a third investment of $10 billion on October 1.

Japan's first round of AI subsidies, totaling 387.3 billion yen, lands with Noetra. Japan's Ministry of Economy, Trade and Industry announced on June 30 that it has selected Noetra, a new company established and led by SoftBank, as the recipient of subsidies for domestic AI research and development. The subsidy program will span five years (fiscal years 2026-2030), providing 387.3 billion yen in financial support to Noetra in fiscal year 2026, with aid expected to expand after fiscal year 2027 based on performance, bringing the total estimated subsidy to 1 trillion yen. Formerly known as "Japan AI Foundation Model Development," Noetra will fully launch its AI R&D in July, focusing on "physical AI" that can be applied to robotics and smart devices.

Key Events Calendar

Eastern Time | Event |

July 1, 8:15 AM | U.S. June ADP Private Employment Data (Expectations: +78,000 to +125,000, Previous: +118,000) |

July 1, 9:00 AM | Fed Chairman Warsh attends the ECB Forum on Central Banking "Policy Panel" and delivers a speech |

July 2, 8:30 AM | U.S. June Nonfarm Payrolls Report (Market Expectations: +115,000, Unemployment Rate: 4.3%) |

July 7 | SpaceX officially included in the Nasdaq 100 Index (funds tracking the index are expected to buy approximately $4.3 billion in stock) |

The collective weakness in the memory chip and optical communication sectors reflects growing market divergence over the sustainability of the AI semiconductor rally. The new round of short bets by "Big Short" Michael Burry has resonated with the ongoing correction in the semiconductor sector. Meanwhile, SoftBank's $10 billion follow-on investment in OpenAI and the implementation of Japan's first round of AI subsidies confirm, from another perspective, that capital and policy levels remain highly optimistic about the long-term prospects of AI. Tonight, the ADP employment data and Warsh's speech will debut together, providing the market with dual guidance on employment resilience and the path of monetary policy.

Recommended Articles