Nu Holdings Stock Is Falling. Here's Why I'm Buying Shares.

Key Points

It's seeing slightly higher loan losses, but that is factored into the company's business model.

The digital bank's growth opportunity is huge in Brazil, Mexico, and other countries.

The stock looks cheap, and management is about to begin buying back shares.

- 10 stocks we like better than Nu Holdings ›

Few stocks are as misunderstood as Nu Holdings (NYSE: NU). The digital bank, which focuses on Latin America, is poised to generate substantial profits in the years to come, but it keeps being downgraded by Wall Street due to misinterpretations of its lending business.

Shares are now down 37% from their highs, while revenue grew 42% year over year last quarter. Here's why I'm buying more shares of Nu Holdings after this recent dip.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Increasing loyalty in Brazil

As of last quarter, the company had 135 million customers, most of them in Brazil. Over half of adults in the country have an account with the digital bank, which aims to bring modern banking tools to those whom legacy banks previously disregarded, keeping them out of the financial system.

At the same time, Nu's revenue from existing customers in Brazil is lower than that of the average bank. Management intends to change this by increasing product penetration through services like instant payments, lending, investing, and credit cards.

For example, management just launched a premium credit card for wealthier customers called Nubank Ultravioleta, using a model similar to American Express' by adding services around credit card spending. This and other initiatives are why average monthly revenue per customer just hit a record of $15.90, growing 23% year over year.

Investors are pessimistic about the digital bank's increase in nonperforming loans (NPLs) that are 15 to 90 days past due, which rose to 5% last quarter. However, this is a seasonality issue in Brazil and was only up from 4.8% in the same period a year ago. While you don't want to minimize this figure, it is the price of doing business with lower-income earners, which is factored into the interest rate charged on loans.

Net income was up 41% year over year last quarter to $871 million.

Image source: Nu Holdings.

Hitting its stride in Mexico

The company's expansion into Mexico is driving strong growth. It recently hit 15 million active customers in the country and is closing in on $1 billion in annual revenue, having launched its business in 2021. Mexico is much further behind Brazil in digital payments and credit card adoption, giving Nu Holdings the same runway it had in Brazil a decade ago.

Market share in Mexico is still minuscule, but it is seeing huge customer adoption and steady growth in monthly revenue per customer. As these work in tandem, revenue in Mexico should continue to grow rapidly. Plus, its business just turned profitable in the country, which will turn it from a drag on net income over the last few years to a benefit over the next few.

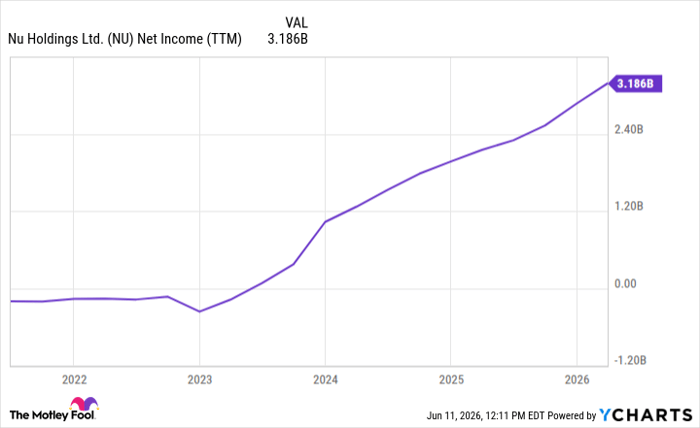

NU Net Income (TTM) data by YCharts; TTM = trailing 12 months.

Returning capital to shareholders

Over the past 12 months, Nu Holdings' net income was $3.2 billion. I expect further growth from the steady increase in revenue per customer in Brazil and the growth inflection underway in Mexico. The cherry on top is the company's rapid growth in Colombia and its planned expansion into the U.S. once it obtains a banking license here.

This should help net income climb to $5 billion and even above $10 billion in the years ahead, especially once you factor in the operating leverage inherent in a scaled-up national bank with no overhead costs from physical branches.

After its drawdown, Nu stock now trades at a market cap of $57 billion. To take advantage of this lower price, management is repurchasing stock in a new $1 billion program, which will help to reduce shares outstanding and grow earnings per share . A market cap of $57 billion is cheap for a business poised to eventually generate $10 billion or more in annual net income; you just need a time horizon longer than a year. That's why I am buying more shares of Nu Holdings stock.

Should you buy stock in Nu Holdings right now?

Before you buy stock in Nu Holdings, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nu Holdings wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $433,268!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,259,391!*

Now, it’s worth noting Stock Advisor’s total average return is 935% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 13, 2026.

American Express is an advertising partner of Motley Fool Money. Brett Schafer has positions in Nu Holdings. The Motley Fool has positions in and recommends American Express and Nu Holdings. The Motley Fool has a disclosure policy.

Recommended Articles