Earnings Beat Yet 14% Plunge, Ciena Drags Down Optical Communications Sector; Too High Expectations or Too Large a Bubble?

TradingKey - Optical networking equipment maker Ciena ( CIEN.US) delivered a stunning earnings report for the second quarter of fiscal 2026, yet the market voted with its feet, sending the stock price down nearly 14%.

Better-than-expected growth undercut by high expectations

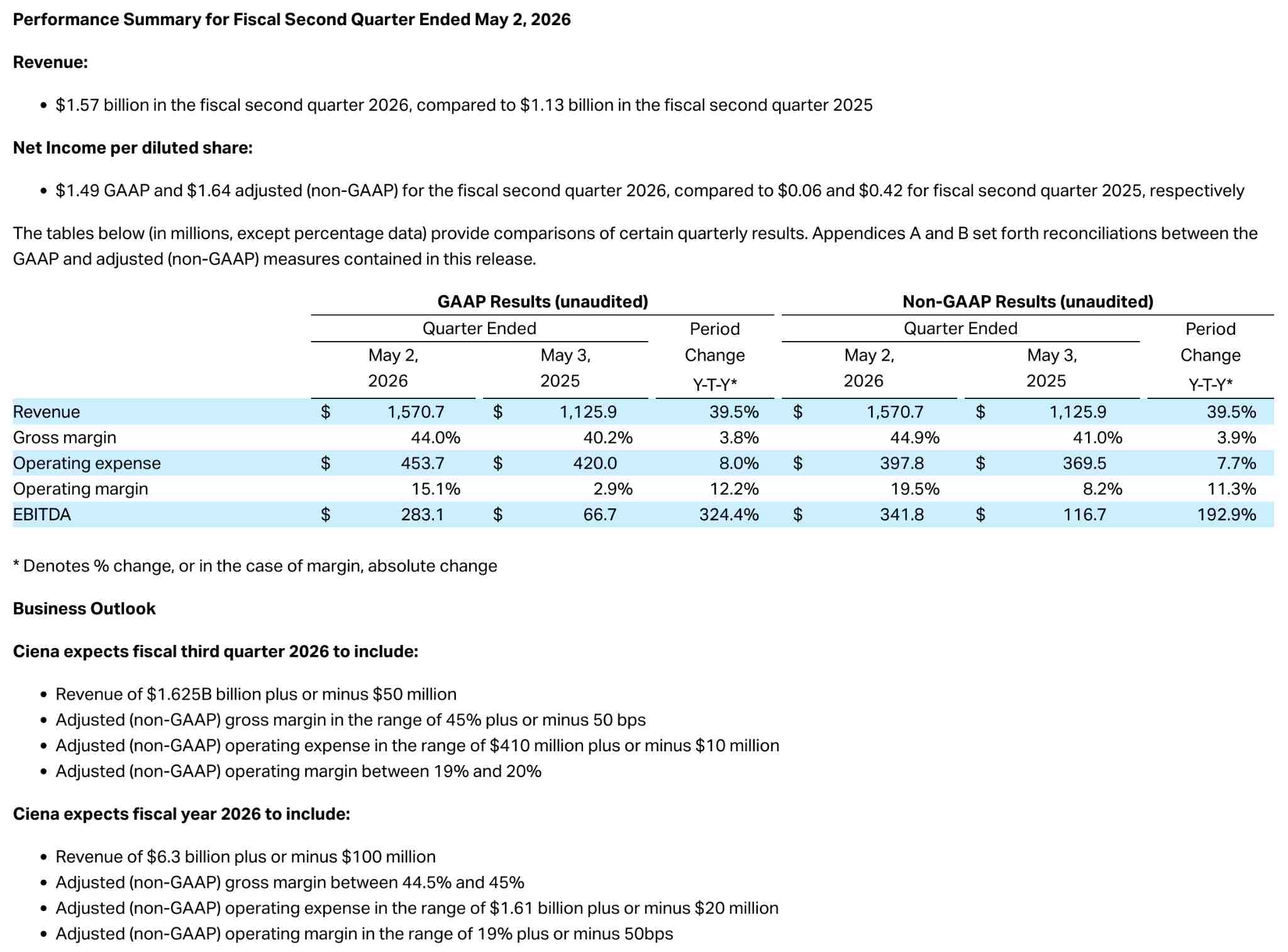

Ciena reported its second-quarter fiscal 2026 financial results before the U.S. market open on Thursday.

The earnings report showed that Ciena's quarterly revenue reached $1.57 billion, up approximately 40% year-over-year and nearly 4.7% above market expectations. Adjusted earnings per share (EPS) were $1.64, a 290% surge year-over-year, exceeding the expected $1.46 by more than 12%. Gross margin rose to 44.9% from 41% in the prior year, while operating margin soared to 19.5% from 8.2%.

[Ciena Announces Q2 FY2026 Financial Results, Source: Investor.ciena.com]

The core performance driver was robust demand for optical networking from AI data centers. Direct sales to cloud service providers grew 69% year-over-year, the service provider business increased 27%, and the routing and switching business jumped 88%, driven by DCOM solutions. Backlog increased by over $600 million quarter-over-quarter to $7.7 billion, with a book-to-bill ratio of 1.4, indicating demand far outstripping supply capacity.

Guidance also exceeded expectations. Ciena raised its full-year revenue growth guidance to approximately 32%, a significant increase from the previous 28%, with a full-year revenue range of $6.2 billion to $6.4 billion; the midpoint of this range is higher than the top end of the previous guidance. Q3 revenue guidance of $1.575 billion to $1.675 billion was also above market estimates. From a fundamental perspective, this was undoubtedly a better-than-expected earnings report, characterized by accelerating revenue growth, significant profit expansion, and comprehensive upward revisions to guidance, with no signs of deteriorating fundamentals.

However, after the results were released, the stock turned down by more than 9% in pre-market trading and ultimately closed down 13.66%. In the 90 days leading up to the report, Ciena's share price had more than doubled, surging over 600% over the past year. Investors had already priced in a massive beat; expectations for Ciena had been pushed to the extreme. Since the reported data only slightly beat market expectations—falling short of capital market expectations—the stock experienced a "buy the rumor, sell the news" reaction, mirroring the post-earnings plunge previously seen with Broadcom (AVGO.US).

Structural Risks Overlooked by the Market

Market analysis suggests that Ciena's previous gains were excessive and its valuation is severely overextended. Prior to the earnings report, Ciena's forward P/E ratio was as high as 90x, and with a gain of over 600% over the past year, its valuation has reached historically extreme levels. Analysis from Simply Wall St indicates that the current share price is significantly overvalued relative to its fair value. Although 13 of 20 analysts issued a buy rating, the consensus target price is only $464, which is approximately 26% lower than the pre-earnings level of about $620.

Furthermore, Ciena's primary structural risk lies in its high customer concentration, with its two largest cloud clients accounting for about one-third of the quarterly revenue. Supply chain bottlenecks continue to constrain revenue upside, and supply tightness is expected to persist at least until fiscal year 2027.

Competition in front-end optics is intensifying. In mid-May, the CEO of Lumentum updated the capacity forecast through 2028 to being sold out within two quarters, which fueled a rally across the entire AI optical communications sector. Ciena's latest earnings triggered a sympathy sell-off across the sector; Lumentum, Marvell, and Nokia all saw intraday declines of more than 5%, while POET Technologies dropped nearly 7%, leading to a collective correction for the entire optical communications sector.

Allocation Window Following Sentiment Clearing

TD Cowen analysts, while maintaining a $675 price target, explicitly warned that investors may be overly optimistic about the speed at which Ciena can convert long-term optical transport tailwinds into actual financial gains.

The bullish thesis rests on the fact that demand for AI data center interconnects has yet to hit a ceiling, with backlogs and book-to-bill ratios at historical highs and visibility extending into 2027. A correction of approximately 14% has partially cleared previous sentiment bubbles, and several institutions' price targets continue to provide upside guidance. CEO Gary Smith noted during the earnings call that hyperscale cloud providers have increased their 2026 capital expenditure plans and expect this trend to persist through 2027 and beyond.

Bearish concerns focus on high customer concentration, with two major cloud customers contributing approximately one-third of the quarter's revenue. It remains unclear when supply chain constraints will substantively ease, and the large-scale contribution of the new RLS HyperRail product will not materialize until 2027. Current valuations have already front-run future growth rates, meaning any signals of demand deceleration could trigger further valuation compression.

Ciena's plunge does not stem from deteriorating fundamentals; rather, the market judged that growth data—even if exceeding expectations—was insufficient to support further re-rating given overly high expectations. Furthermore, the fact that institutions are raising their price targets suggests that the mid-term narrative remains intact.

For long-term investors, this correction may serve as a window to observe the mid-to-long-term certainty of the AI optical networking infrastructure sector. However, for short-term traders, current price levels are still in the early stages of a valuation reset; coupled with an unclear external environment, volatility risks have yet to be fully exhausted.

Recommended Articles