HP Faces Earnings Test After Six-Day Rally, Is AI PC Penetration the Deciding Factor?

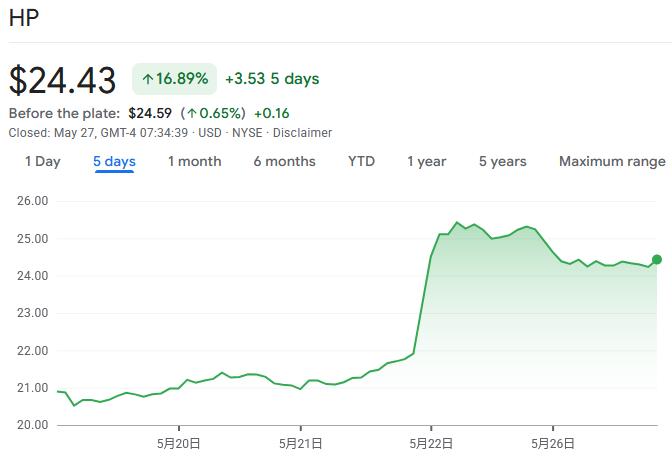

TradingKey - After a six-day winning streak, HP ( HPQ) shares saw a pullback on May 26. Market attention is now focused on the company's fiscal 2026 second-quarter earnings report, due after the bell on May 27, with AI PC penetration serving as a key metric to validate market expectations.

The immediate catalyst for this rally was rival Lenovo Group. Lenovo's earnings report on May 21 showed revenue growth hitting a five-year high, with nearly 40% of sales derived from AI-related products. The market interpreted this as a sign that the entire PC industry is entering an AI-driven replacement cycle, and as a top-tier player, HP is naturally expected to benefit.

As two global PC market leaders, HP and Lenovo share significant overlap in target customers, distribution networks, and product refresh cycles. Lenovo's robust performance has led investors to form similar expectations for HP's upcoming results.

Analysts surveyed by FactSet currently project that HP will report adjusted earnings of 71 cents per share on revenue of $14 billion for its fiscal second quarter ended in April.

Investors and traders are closely watching revenue and management guidance for the next quarter. Given the significant prior gains in the stock price, any figure that falls short of expectations could serve as a trigger for a short-term reversal.

AI PC Penetration Rate Becomes Key

Although HP has exceeded earnings expectations only once in the past eight quarters, the market's focus this time has shifted beyond traditional financial metrics toward AI PC penetration data.

In the previous fiscal quarter, AI-capable PCs accounted for approximately one-third of HP's shipments. If commercial market penetration shows a significant increase this time, it will fundamentally alter the market's assessment of its growth potential; conversely, the recent share price surge driven by Lenovo's strong AI business performance might be proven an overreaction.

At its previous Imagine event in New York, HP introduced on-device AI features like HP IQ and launched a PC portfolio targeting high-load and local AI workloads; these moves are expected to drive a dual increase in the proportion of high-end model shipments and the average selling price (ASP).

Given management's EPS guidance of $0.70–$0.76 for the current quarter compared to the consensus estimate of $0.71, HP's modest revenue recovery relies on product mix upgrades and the release of commercial replacement demand to offset pressures from component cost fluctuations and promotional activities.

If HP IQ achieves higher penetration in the business and creator laptop series, coupled with upgrades in NPU computing power and screen specifications on new-generation platforms, HP is expected to maintain competitiveness in the high-end segment and drive the release of gross margin elasticity in its Personal Systems business.

However, current market consensus suggests a 12.57% year-over-year decline in EBIT for this quarter. Short-term profitability remains dependent on the pace of expense control and channel discount intensity; product upgrades alone are insufficient to fully offset cost and promotional pressures, and attention must also be paid to the dilutive effect of new product stocking cycles on gross margins within the quarter.

Cost pressure

Soaring memory costs are becoming a severe challenge widely faced by the technology hardware industry. As a core component for running artificial intelligence, memory demand has far outstripped current supply capacity as global companies accelerate the deployment of AI infrastructure, directly driving up product prices and squeezing profit margins for equipment manufacturers across the industry.

HP management had warned as early as February, when reporting first-quarter fiscal results, that full-year performance could be "near the lower end of the guidance range" due to the continuous rise in memory costs.

To address cost pressures, technology hardware manufacturers such as HP have been raising product prices to pass on the burden. Evercore ISI analyst Amit Daryanani noted in a research report on May 22nd that despite multiple rounds of price increases for PC products, market demand has remained resilient, and the strength of demand since the beginning of the year has been underestimated by the market. He maintained an "In-Line" rating on HP with a price target of $20.

HP is also actively advancing internal optimizations to enhance profitability. The company has launched a multi-year cost-cutting plan aimed at saving $1 billion annually by 2028, involving measures such as organizational streamlining and process automation, with an expected workforce optimization of 4,000 to 6,000 positions.

Referencing the market consensus estimate of $0.71 in earnings per share for this quarter and a net margin of 3.77% in the previous fiscal quarter, marginal improvements on the expense side will have a significant leveraging effect on profit margins. If channel promotional intensity weakens and freight costs decline, coupled with the optimization of administrative expenses, HP's net margin is expected to achieve a quarter-over-quarter recovery.

However, it should be noted that if seasonal PC promotions continue or memory prices experience periodic upward trends, the company's gross and net margins still face downward pressure, requiring management to dynamically balance market share and profit targets within the quarter.

Furthermore, investors are closely monitoring progress regarding HP's management changes. In early February this year, HP announced that then-CEO Enrique Lores was stepping down, with board member Bruce Broussard taking over as interim CEO. The market is currently still waiting for the latest news from the company regarding a permanent successor.

Wall Street Divided on HP

Current institutional sentiment toward HP is generally cautious, with core disagreements centered on PC demand trends, component cost pressures, and the pace of cost optimization implementation.

Morgan Stanley ( MS) has repeatedly lowered its price target for HP and maintained a weak rating, arguing that the company's outlook on PC industry headwinds and memory price inflation is overly optimistic. It notes uncertainty in short-term margin recovery and suggests that more explicit cost reduction and product mix upgrades are needed to support its valuation.

Bank of America ( BAC) has also issued a warning, noting that due to PC demand volatility and cost pressures, HP's fiscal year 2026 earnings still face downside risks. With a high likelihood of pressure on margins, the bank suggests focusing on marginal changes in cost optimization and channel policies.

From a valuation perspective, HP's current forward P/E ratio is in the single digits, with a dividend yield near 5%—well above the S&P 500 average of approximately 1.05%. This data suggests the market has largely priced out optimistic expectations for its growth prospects.

Over the past twelve months, HP's share price has fallen by approximately 24%, compared to a 27% gain in the S&P 500. Despite a recent rebound, HP's stock remains down about 5% year-to-date.

A relatively optimistic view comes primarily from JPMorgan Chase ( JPM ), which raised target price ranges for the hardware sector, believing some manufacturers will benefit from cost improvements and product mix upgrades, potentially leading to upward revisions in medium-to-long-term earnings growth expectations. However, it favors other names within the sector and maintains a relatively moderate stance on HP.

Recommended Articles