The JPMorgan Equity Premium Income ETF Doesn't Interest Me, but It Might Work for You

Key Points

Equity and index options are speculative instruments that can produce surprisingly big returns.

The outsize potential of options requires taking on outsize risk, and comes with some sort of trade-off.

The big trade-off with JEPI is above-average short-term cash flow in exchange for below-average total returns (particularly after taxes).

- 10 stocks we like better than JPMorgan Equity Premium Income ETF ›

Income investors willing to look a bit off the beaten path might have come across the JPMorgan Equity Premium Income ETF (NYSEMKT: JEPI) in their search; its monthly dividend payments and yields of up to 10% are certainly attractive.

As is the case with all investment choices, however, this one comes with trade-offs ... trade-offs that don't work for me. But that doesn't necessarily mean this fund isn't right for you.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

What's the JPMorgan Equity Premium Income ETF?

It's a somewhat unusual instrument.

Image source: Getty Images.

In simplest terms, JEPI is a large-cap equity fund, but with a major twist. That twist is that it generates recurring short-term income by selling -- or "writing" -- call options, using its stakes in stocks like Alphabet, Apple, and Johnson & Johnson as a kind of collateral for these somewhat risky options trades. Selling these "covered" calls, however, also means the fund is occasionally forced to sell some of its stock holdings at below-market prices.

Options are essentially bets that a stock or index will rise or fall to a particular price within a specific time frame. Options contracts are bought and sold just like stocks, at ever-changing prices that reflect their underlying stock or index's ever-changing value. Although options can be used to force the contract's seller (JPMorgan's fund, in this case) to buy or sell a stock or index at the contract's specified price, most speculators will simply buy call options when they're anticipating bullishness, or purchase put options when they're feeling bearish. The ultimate intent is the same either way. That's selling these options for a profit later, assuming the expected move's been made. If it hasn't taken shape as hoped, that trade will almost certainly be a loss.

That's not the only way to trade options, though. You can also sell options without actually first owning them, and either buy them back in the future at (hopefully) a lower price, or simply let them "expire," or run out of time before there's a reason to utilize them, leaving you free and clear with the full amount of money you pocketed when you first sold that contract. It's not unusual for the sale of one-month call option contracts to generate cash income on the order of 5% to 10% of the underlying stock holding's total value.

This latter strategy is the one that JEPI's managers are utilizing. As was noted, this fund holds sizable positions in several large-cap companies. As the right opportunities surface during any given month, the fund will sell call options to generate cash income, effectively using its stock holdings as collateral in case the trader on the other side of the option contract decides to exercise their right to buy those shares at the option contract's specified price. JPMorgan's hope, of course, is that all of the covered calls the fund sells will expire worthless, allowing the ETF's portfolio to not only keep all of the proceeds from the option it sells, but also keep all its shares of the stocks it owns.

It doesn't always work out that way, of course; sometimes the fund is forced to sell these shares at a below-market price to make good on the options contracts it sold.

Even when it does happen, however, it doesn't necessarily mean writing covered calls is a net-losing strategy. It can and does generate cash income, funding the aforementioned monthly dividends with annualized yields ranging from 5% to as much as 10%. And sometimes more.

That's the case for owning JPMorgan Equity Premium Income ETF.

Here's why I still don't.

The downside of JEPI

As savvy as the premise seems, there's a handful of details that might make you rethink taking on a stake in this ETF.

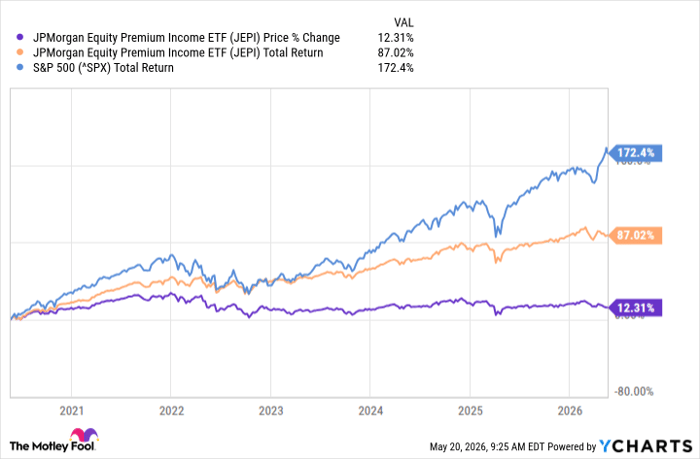

First and foremost, it habitually underperforms ... with or without its dividends factored into the calculation.

See, there's a lot of buying and selling of stocks and options, which slowly but steadily chips away at a portfolio's total value due to a combination of slippage, trading costs, and the occasional, but inevitable, bad luck. While a covered call strategy can mute some of the market's net downside when it's falling, regularly selling covered calls in a bull market will always force you out of your existing stock trades at below-market prices. That's what "covered" means in this sense, in fact -- if the party on the other side of the call contract you sold short wants to take delivery of the stock in question, they can require you to sell your shares at the option's specified price below the current market price. That's the big risk here.

JEPI data by YCharts

Another drawback of JEPI is the inconsistency of the dividend it pays. Although its recently reported 30-day yield is an impressive 9.8%, the $0.45-per-share dividend it paid at the beginning of this month wasn't nearly as healthy back in February when it was only $0.34 per share, which was well down from last June's $0.54.

Blame the nature of options prices, mostly. The more volatile the market is, the better their pricing. The tamer the market, the lower options prices get. The fund's managers have no control over this.

Then there's the less obvious potential problem with the JPMorgan Equity Premium Income ETF that could impact at least some investors. That's its taxable turnover. Last year's total turnover rate was a massive 172% of the ETF's total portfolio value, making it one of the market's least tax-friendly holdings...

... that is, if it's not held in a tax-sheltering retirement account. Strategically speaking, of course, there's little benefit in holding such an ETF inside an IRA. You can achieve better net returns with an ordinary large-cap index fund like the SPDR S&P 500 ETF Trust or the Vanguard S&P 500 ETF -- even if you're regularly selling pieces of it to produce income -- with no additional tax liability.

Most investors probably want something simpler

This isn't to suggest there's never a case to be made for owning a stake in the JPMorgan Equity Premium Income ETF. Some investors will have a very specific reason to do so, like a prolonged bear market during which you want to limit your net downside while also generating regular (albeit unpredictable) income.

Those cases will be few and far between, though. If you feel like you're facing one, just triple-check to be sure JEPI is actually how you want to meet your particular need. In most instances, there will almost always be a better solution.

And in a more philosophical sense, always remember the more complicated a strategy is and the more activity it requires, the more potential failure points it brings to the table. Simpler is almost always better just because there are fewer variables that can go awry.

Should you buy stock in JPMorgan Equity Premium Income ETF right now?

Before you buy stock in JPMorgan Equity Premium Income ETF, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and JPMorgan Equity Premium Income ETF wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $481,750!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,352,457!*

Now, it’s worth noting Stock Advisor’s total average return is 990% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 21, 2026.

James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Vanguard S&P 500 ETF. The Motley Fool recommends Johnson & Johnson. The Motley Fool has a disclosure policy.

Recommended Articles