Nvidia Is Still a Top Buy in the Stock Market. Here's Why.

Key Points

Nvidia's clients are starting to announce their 2027 capital expenditure plans.

The chipmaker's stock doesn't look terribly expensive from a forward earnings perspective.

- 10 stocks we like better than Nvidia ›

Given that it's already the world's largest company, it's natural to wonder how much larger Nvidia (NASDAQ: NVDA) can get. I think the answer is fairly simple: much larger. Though hyperscalers have already set new records year after year with how much they are devoting to capital expenditures, the future still looks like it will bring even higher spending, which bodes well for a company that is supplying so much of the key hardware for artificial intelligence (AI).

I think Nvidia's still a top buy, and it all has to do with future demand and its current pricing.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

The AI build-out is just getting started

This year, the big four AI hyperscalers plan to spend around $650 billion on data center investments.

That's a ton of money, but this year's growth has already been fairly accounted for in stock prices; the question is, what will 2027 hold? From Nvidia's internal projections, it holds a lot more. It estimates that global data center capital expenditures will reach $3 trillion to $4 trillion annually by the time 2030 rolls around, up from about $600 billion in 2025. That's a major ramp-up, and Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) just confirmed part of it. During its latest earnings call last month, management noted that it will make a "substantial increase" in capital expenditures in 2027 compared to 2026. While other hyperscalers haven't made similar statements yet, it's still early. It won't surprise me to hear similar commentary from them during next quarter's results.

The runway is still massive for AI spending, and with Nvidia being a major supplier in this industry, it's set to benefit. However, the market is really only projecting one year's worth of strong growth into its stock price.

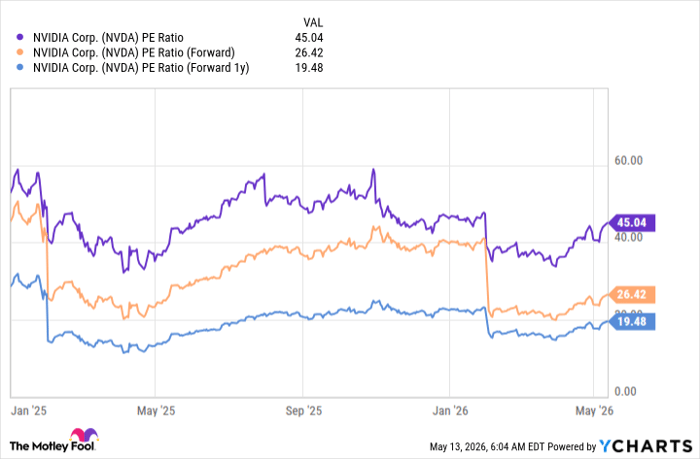

NVDA PE Ratio data by YCharts

With a price-to-earnings ratio of 45, Nvidia is clearly expensive based on that valuation metric. But on a forward earnings basis, which considers expected growth this year, it trades at a more reasonable ratio of 26. When you use next year's expected earnings, that figure falls to 19. Moreover, Wall Street analysts have consistently underprojected Nvidia's growth rate, so this metric may be underselling Nvidia's potential.

Regardless, I think positive news regarding 2027's capex will push the stock higher throughout the rest of the year, especially as more companies divulge their plans, which makes Nvidia a solid stock to buy today.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $472,205!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,384,459!*

Now, it’s worth noting Stock Advisor’s total average return is 999% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 15, 2026.

Keithen Drury has positions in Alphabet and Nvidia. The Motley Fool has positions in and recommends Alphabet and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles