TradingKey’s The Week on Wall Street: Iran Truce Cools Inflation, Fed Hawks Rate, but U.S. Stocks Still End Week Higher

Previous Week’s Market Review & Analysis

TradingKey - The geopolitical ceasefire between the United States and Iran on Monday, June 15, marked a major breakthrough, reopening the Strait of Hormuz and sending Brent crude down 4.8 percent to around 83 dollars per barrel, which significantly eased global inflation anxieties. Domestically, May retail sales surged by a better-than-expected 0.9 percent month-over-month, with the core control group rising 0.7 percent, demonstrating resilient consumer spending. Meanwhile, May industrial production edged up 0.1 percent, showing steady domestic manufacturing improvement supported by tariffs and energy sector activity, despite falling slightly short of consensus estimates.

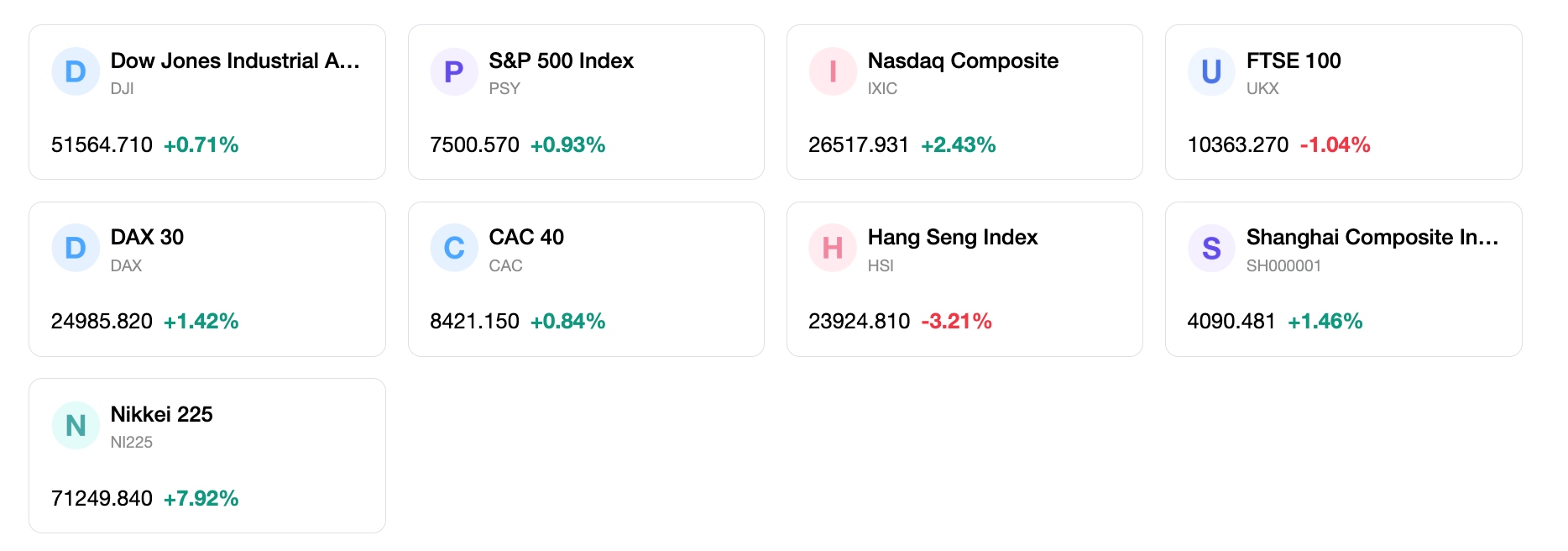

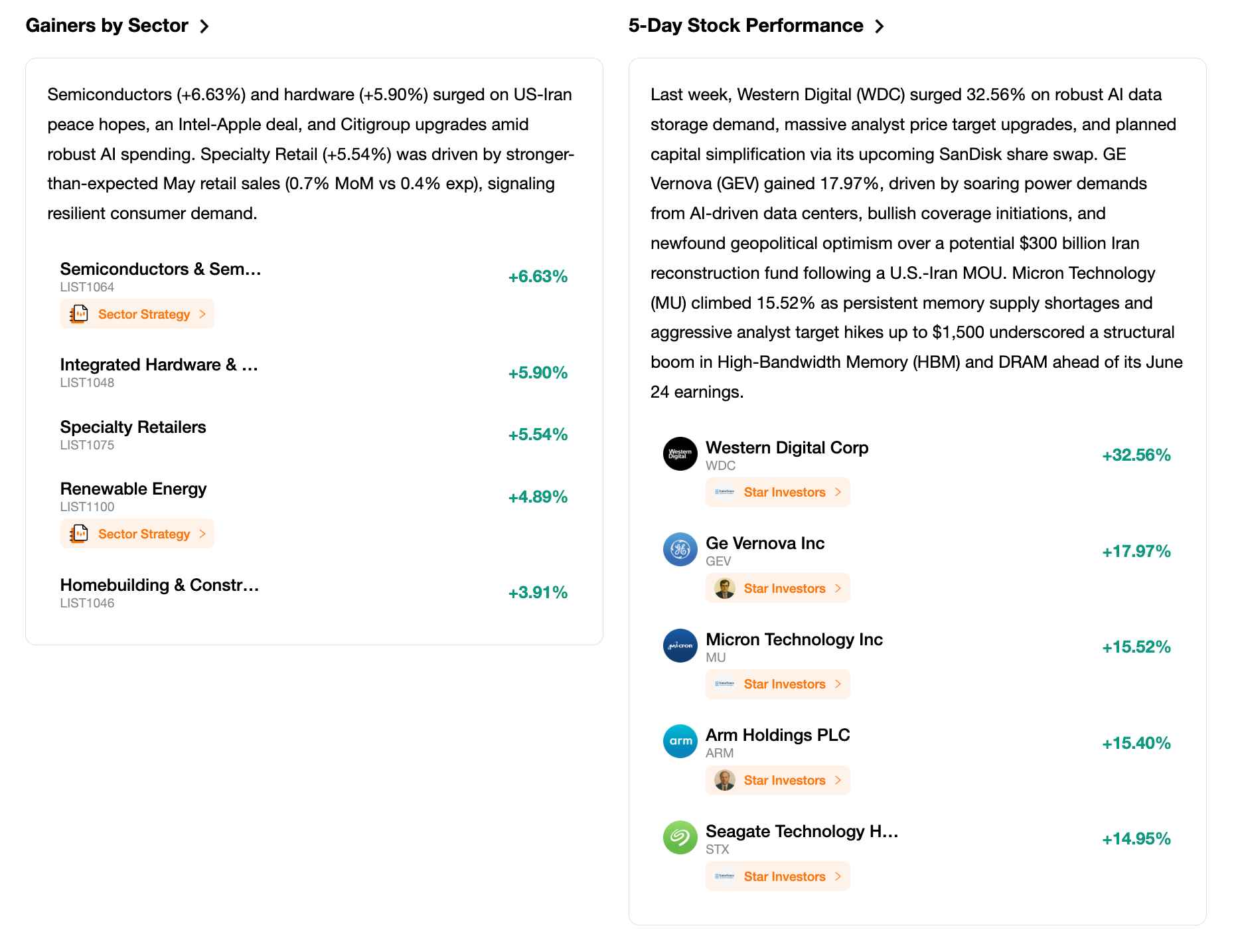

In a holiday-shortened trading week ending Thursday, June 18, before the Juneteenth National Independence Day holiday on Friday, June 19, major U.S. stock indexes posted solid weekly gains. The S&P 500 rose 0.9 percent over the period to close at 7,500.58, marking its eleventh positive week in twelve, while the Nasdaq Composite jumped 2.4 percent to end at 26,517.93, driven by a late-week technology resurgence. The Dow Jones Industrial Average finished in positive territory, closing at 51,564.70 after a minor gain of 0.14 percent on Thursday. Semiconductor stocks experienced high volatility, undergoing a sharp pullback on Wednesday following hawkish monetary signals, but rebounded strongly on Thursday as the iShares Semiconductor ETF jumped over 6 percent, led by a 10.6 percent surge in Intel and a 3 percent rise in Nvidia.

The Federal Open Market Committee meeting on June 17 was the week's focal event, marking Kevin Warsh's debut as Federal Reserve Chair. While the Fed unanimously held the policy rate target range steady at 3.50 percent to 3.75 percent, the updated Summary of Economic Projections delivered a hawkish shift. The median dot plot projected a rate hike by year-end 2026, targeting 3.75 percent, a complete reversal from the rate cuts projected in March. Chair Warsh demonstrated a distinct shift in communications, drastically shortening the official policy statement to just 132 words, stripping away previous forward guidance on rate cuts, and explicitly stating the Committee’s absolute commitment to price stability.

Market sentiment oscillated between geopolitical relief and monetary caution. Risk appetite surged early on the Middle East ceasefire and falling oil prices, but briefly soured on Wednesday as investors digested the Fed's hawkish rate projections. However, sentiment rebounded sharply on Thursday, catalyzed by the Trump administration's announcement of a partnership between Intel and Apple to manufacture chips domestically, which triggered substantial inflows into technology and semiconductor equities. Meanwhile, Treasury yields saw modest upward pressure as fixed-income markets adjusted to a higher-for-longer rate horizon, while post-IPO profit-taking saw recently listed SpaceX trim recent gains.

Overall, the U.S. equity market is operating under a logic of resilient growth colliding with restrictive monetary policy. The underlying economic cycle remains robust, characterized by a healthy labor market, steady manufacturing activity, and strong consumer demand, which effectively mitigates immediate stagflation risks. Although the Federal Reserve's hawkish stance acts as a valuation headwind, the cooling of energy-driven inflation from the geopolitical truce is expected to eventually alleviate price pressures. In the interim, strong corporate fundamentals and targeted policy support in high-tech manufacturing are offsetting restrictive rate dynamics, keeping the broader upward trend intact.

Next Week's Key Market Drivers & Investment

Looking ahead to the week of June 22, several critical economic data releases will take center stage. On Thursday, June 25, investors will parse May Personal Income and Spending data, Durable Goods Orders, and the final estimate of first-quarter gross domestic product. The most critical release occurs on Friday, June 26, with the publication of the May Personal Consumption Expenditures price index, the Federal Reserve's preferred inflation gauge, alongside the final reading of the University of Michigan Consumer Sentiment survey. Additionally, housing and regional manufacturing data will provide further growth clues, including the Richmond Fed Manufacturing Index on Tuesday, June 23, and May New Home Sales on Wednesday, June 24.

The market narrative next week is expected to pivot squarely back to inflation dynamics and Fed policy expectations. Investors will closely dissect the PCE deflator to see if core inflation metrics are beginning to moderate or if the hawkish dot-plot shift was fully justified. While the recent plunge in crude oil prices following the Strait of Hormuz reopening will take time to feed into core services inflation, it should begin to cool headline numbers and bolster consumer confidence. Consequently, any upside surprise in core PCE inflation will likely solidify expectations for a year-end rate hike, pushing Treasury yields higher and testing current equity valuation multiples.

In terms of portfolio allocation, we recommend maintaining a balanced and quality-focused stance, emphasizing sectors with robust pricing power and secular tailwinds. Large-cap technology and domestic semiconductor companies remain attractive, particularly those positioned to benefit from localized chip-manufacturing mandates and strong enterprise spending. Tactically, investors should consider exposure to industrial leaders and defense contractors, while selectively adding to high-quality consumer discretionary names that demonstrate resilient demand. Additionally, financial institutions stand to benefit from a steepening yield curve and elevated net interest margins under a higher-for-longer monetary regime.

Several key risks warrant close attention in the upcoming week. First, any setbacks or diplomatic hurdles in the ongoing sixty-day negotiations regarding Iran's nuclear program could trigger a sudden reversal in crude oil prices, reigniting energy-driven inflation fears. Second, a hotter-than-expected core PCE print on Friday could cause a sharp repricing of interest rate expectations, leading to a broader sell-off in growth sectors. Finally, high valuation multiples across tech megacaps leave the market vulnerable to localized profit-taking, and potential supply-chain implementation bottlenecks for major domestic manufacturing projects could dampen short-term corporate enthusiasm.

Markets Weekly

5-Day Index Performance

Recommended Articles