Can Pfizer's Dividend Survive the Patent Cliff? This $10.5 Billion Cancer Bet Could Hold the Answer.

Key Points

Pfizer’s net income is under pressure, and likely will be for the foreseeable future.

Although its replenished pipeline and portfolio should help, Pfizer paid a sizable price for this growth.

A recent deal with a Chinese biopharma offers a more affordable way for Pfizer to grow its top and bottom lines.

- 10 stocks we like better than Pfizer ›

If you keep regular tabs on pharmaceutical giant Pfizer (NYSE: PFE), then you know it hasn't yet restored the revenue lost due to the wind-down of the COVID-19 pandemic; the world just doesn't need its vaccine (Comirnaty) or its infection treatment (Paxlovid) as much as it did in 2022, when the company's top line surged to just over $100 billion. Last year's reported revenue was only $62.6 billion.

You may also know that Pfizer's top-selling drugs, like the blood thinner Eliquis and cancer treatments Ibrance and Xtandi, will lose their patent protection next year, while the patent for its pneumonia vaccine Prevnar 13 is even nearer its end. These three drugs alone accounted for over $20 billion of 2025 revenue.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Connect the dots: Investors worried that Pfizer may not be able to continue paying its dividend aren't unwarranted in their concern. Shares have performed accordingly.

A recent deal struck with China-based biopharma outfit Innovent Biologics (OTC: IVBXF), however, should alleviate at least some of this worry. And it should ease most of the concerns income investors have right now, if this partnership serves as a model for future ones.

Taking the obvious steps

It's not as if Pfizer has been ignoring its march toward some key patent cliff, for the record. It's been acting. In November 2025, the drugmaker completed its acquisition of Metsera, garnering its anti-obesity drug candidates. In 2023, it shelled out $43 billion for Seagen, bringing a handful of promising cancer drugs to the table. The 2022 purchases of Global Blood Therapeutics, Biohaven Pharmaceutical Holding, and ReViral began the recent refill of the company's pipeline and portfolio.

And there's confidence in these acquisitions. With plans to start roughly 20 pivotal drug trials this year, CEO Albert Bourla commented during last month's first-quarter earnings conference call: "Our recent settlement agreements resolving infringement of patent related to Vyndamax [for the treatment of transthyretin-mediated amyloid cardiomyopathy] have the potential to change the growth profile of the company significantly post-2028. This gives us greater confidence that starting in 2029, we will enter a five-year period of high-single-digit revenue CAGR [compound annual growth rate]."

The agreement inked with Innovent Biologics, though, is different from any of the company's recent acquisitions in that it isn't an outright acquisition at all. It's a partnership that will reward the two participants' shared success, without imposing the risk of punishing a suitor for spending too much on what might end up being a disappointing drug lineup.

Different strengths

The cooperation ultimately involves 12 different promising cancer drugs, eight of which have been developed by Innovent, and four of which will come from Pfizer. The two companies will co-develop and co-market any of these drugs that ultimately win approval here and/or abroad. Importantly, Innovent Biologics enjoys access to China's market that Pfizer may not, while Pfizer has a strong reach in most other parts of the world that Innovent might not be able to break into on its own.

Image source: Getty Images.

It's the dollar amounts of the partnership that are so encouraging, or more specifically, the way potential future payments are structured. Although it's being billed as a $10.5 billion deal, Pfizer only owes Innovent $650 million up front. The other $9.85 billion will only be paid as -- and if -- developmental, regulatory, and commercialization milestones are met. In other words, both pharmaceutical companies have an incentive to continue doing their best work.

That's in contrast with Pfizer's expensive acquisition of Seagen, or the $10 billion deal it made for Metsera. Both purchases prompted some criticism over their steep prices, as well as the relatively early developmental stages of each target company's drugs. In fact, Pfizer recently ended early-stage trials of Seagen's SGN-BB228 (PF-08046049) and antibody-drug conjugate PF-08046045, vindicating these criticisms.

Bigger dividend yield, bigger risk

This sort of (almost) 50-50 developmental dealmaking with Innovent Biologics isn't unheard of within the drug development arena, although it is less common. The question remains, however: How does Pfizer's agreement with Innovent boost its ability to continue paying its dividend?

While the exact fiscal specifics are still unknowable at this point, the intuitive answer is also the right one: This partnership is a win for Pfizer (and for Innovent), because it gives both partners a chance at future cash flow without forcing either to pony up a bunch of money to outright own a drug portfolio that might not provide adequate payback on its price tag. It wouldn't be wrong to think of this as a hedge.

Just don't lose perspective. To offset the $60.5 billion worth of long-term debt that's costing it $670 million in interest expense every quarter -- debt that's nearly doubled just since the end of 2022, even though revenue has fallen 40% during this time -- Pfizer will need to make at least a couple more similar deals to truly solidify its ability to fund the dividend while not undermining its ability to grow its business. It's struggling to do both right now.

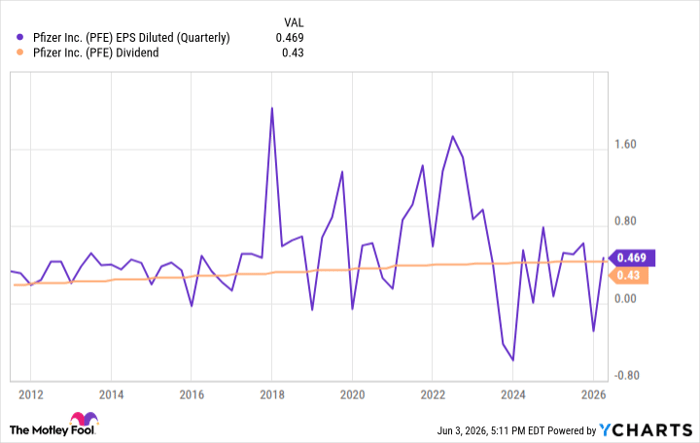

PFE EPS Diluted (Quarterly) data by YCharts.

Yes, Pfizer and its dividend can survive the patent cliff on the horizon. But the "five-year period of high-single-digit revenue CAGR" that Bourla mentioned can't get the job done efficiently on its own, since most of this revenue is also likely to require stepped-up spending (including clinical trials and marketing) to drive it.

Partnerships like the one with Innovent Biologics are how Pfizer can produce much-needed lower-cost revenue growth. It just needs more of them. Only time will tell if we get them, though, making Pfizer stock a somewhat riskier income prospect than some investors will want to take a shot on.

Of course, with a forward-looking dividend yield of 6.7%, at least they're being well compensated for taking on a little more risk.

Should you buy stock in Pfizer right now?

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $443,191!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,258,838!*

Now, it’s worth noting Stock Advisor’s total average return is 941% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 6, 2026.

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Pfizer. The Motley Fool has a disclosure policy.

Recommended Articles