TradingKey The Week on Wall Street: Ceasefire Hopes, AI Boom Lift US Stocks to New Highs; Inflation and Policy Risks Remain

Market Review and Analysis

TradingKey - US markets were closed on Monday, May 25, for Memorial Day. Geopolitical optimism surrounding US-Iran diplomatic talks continued to influence markets, with hopes for a ceasefire or deal regarding the Strait of Hormuz. Kevin Warsh, who was sworn in as Federal Reserve Chair on Friday, May 22, commenced his tenure, with markets closely watching for signals on interest rate policy amidst persistent inflation. The 10-year Treasury yield, which had surged earlier, eased on deal hopes but remained elevated. US Q1 GDP (second estimate) was revised lower to a 1.6% annualized increase. May consumer confidence edged downward. April PCE inflation data was a key release this week, following April CPI printing at a three-year high of 3.8%.

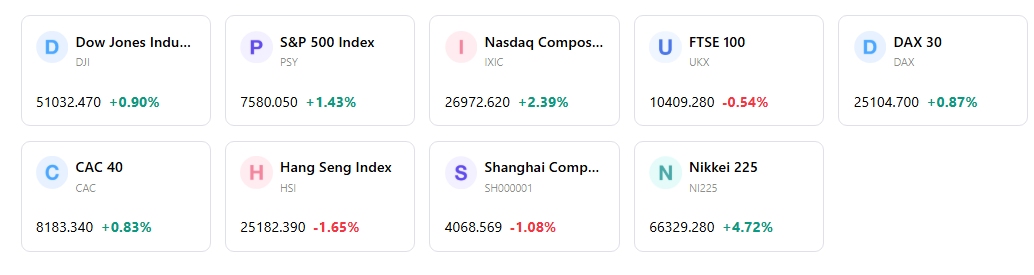

The S&P 500, Nasdaq, and Dow Jones Industrial Average all reached record closing highs this week. On Tuesday, May 26, the S&P 500 rose 0.6%, the Nasdaq composite climbed 1.2%, and the Dow Jones slipped 0.2%. By Tuesday, May 28, the S&P 500 gained 0.58%, the Nasdaq composite rose 0.91%, and the Dow Jones Industrial Average increased 0.05%. The rally was fueled by AI enthusiasm, strong corporate earnings expectations, and hopes for a Middle East peace deal.

Kevin Warsh, the new Federal Reserve Chair, began his term following his swearing-in on May 22, with his first FOMC meeting scheduled for mid-June. Economic data released this week included the revised Q1 GDP, which showed a 1.6% annualized increase, and April PCE inflation data, which was highly anticipated. Reports of a potential 60-day US-Iran ceasefire extension on May 28 spurred market gains.

US consumer confidence edged downward in May. Consumer sentiment hit an all-time low of 44.8 by mid-May, with inflation expectations rising to 4.8% for one year ahead.

The market demonstrated resilience, with major indices reaching new record highs driven by continued optimism around AI, positive corporate earnings sentiment, and the evolving geopolitical landscape regarding the US-Iran conflict. This occurred despite persistent inflation pressures and declining consumer sentiment.

Next Week’s key market drivers and Investment Outlook

Earnings reports are expected from companies such as Hewlett Packard Enterprise (HPE) (June 1), Palo Alto Networks (PANW) (June 2), Broadcom (AVGO) (June 3), CrowdStrike (CRWD) (June 3), and Medtronic (MDT) (June 3). The next Federal Open Market Committee meeting is scheduled for June 16-17.

The market will continue to process the implications of new Fed Chair Kevin Warsh's stance on monetary policy, particularly concerning inflation and potential interest rate adjustments. Geopolitical developments, specifically around the US-Iran situation and its impact on oil prices, will remain a significant determinant of market direction. Continued strong corporate earnings, especially from AI-related sectors, are expected to provide ongoing support for equity valuations.

Investors are advised to favor equities over core fixed income, with a positive outlook for developed market equities, particularly in the US. Technology and semiconductor sectors are expected to continue leading, with software names showing potential for outperformance. Close attention should be paid to corporate revenue trends as the AI-driven earnings boom matures.

Primary risks include the persistence of elevated inflation, which could lead to a more restrictive Federal Reserve policy and impact interest rate expectations. Geopolitical tensions, particularly any escalation in the Middle East, could cause oil prices to rebound and introduce market volatility. Elevated Treasury yields remain a potential headwind for equity performance. Additionally, declining consumer sentiment poses a risk to future consumer spending and overall economic growth.

Markets Weekly

5-Day Index Performance

Recommended Articles