I Recently Bought an Artificial Intelligence (AI) Stock That I Predict Will Double by the End of 2026

Key Points

Upstart developed an AI algorithm that analyzes potential borrowers to determine their credit-worthiness.

The company is on track to generate a record amount of revenue in 2026, and management is bullish about 2027 and 2028.

Upstart stock is trading at an attractive valuation, and I predict it could double before this year is over.

- 10 stocks we like better than Upstart ›

Upstart Holdings (NASDAQ: UPST) developed an artificial intelligence (AI)-powered algorithm that analyzes more than 2,500 data points to determine the credit-worthiness of a potential borrower. The algorithm gradually becomes more predictive as it ingests more data, further increasing its edge over traditional assessment methods that have relied on Fair Isaac's FICO credit scoring system for the past 30 years.

Upstart isn't a lender. Instead, it uses its algorithm to originate loans, which are then sold to its funding partners, mainly banks. This business model is capital-light, which is why the company is generally quite profitable despite the early-stage nature of its business.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Upstart stock is down by 33% this year as investors worry the sharp spike in oil prices -- caused by the conflict in Iran -- will hit household budgets and reduce demand for credit. I used this as a buying opportunity and scooped up a few shares for my portfolio in March. Here's why I think there's room for the stock to double before 2026 is over.

Image source: Getty Images.

AI is taking lending into a new era

Upstart originates unsecured personal loans, car loans, and home equity lines of credit (HELOCs). The company originated 425,356 loans during the first quarter of 2026, which was up 77% from the year-ago period.

Thanks to Upstart's AI-powered approach, it can approve or deny applications practically instantly, whereas it would take a human assessor days or even weeks to analyze an equivalent amount of data on each prospective borrower. Plus, during the first quarter, 91% of funded (approved) loans were fully automated using AI, meaning they didn't require any human intervention.

Personal loans are Upstart's bread and butter, accounting for the majority of its originations. But its HELOC and automotive segments grew by 250% and 300%, respectively, during the first quarter, so they are quickly becoming significant pieces of the business. For customers who want a HELOC, Upstart can take them from the application phase to the signing phase in just six days, which is much faster than the industry average of 40 days. Therefore, I expect this will be a very lucrative market for the company in the long run.

At Upstart's AI day meeting last year, Executive Chairman Dave Girouard said AI could replace all human-driven credit assessment processes within the next decade. More than $25 trillion in loans is originated worldwide across all categories every year, generating a whopping $1 trillion in fee income, so this is an enormous opportunity for Upstart.

Upstart is on track for a record year

Upstart generated a record $308 million in revenue during the first quarter, representing 44% growth from the year-ago period. The company had a net loss of $6.6 million on a generally accepted accounting principles (GAAP) basis due to a sharp increase in operating expenses, as management invested aggressively in growth. It was the only loss in the past four quarters, so this isn't the norm.

Besides, after excluding one-off and noncash expenses, Upstart actually delivered $40 million in adjusted (non-GAAP) earnings before interest, taxes, depreciation, and amortization (EBITDA) during the quarter, which is the company's preferred measure of profitability.

Upstart is forecasting $1.4 billion in revenue during 2026, which would be a record. But it gets better, because management thinks revenue could grow at a compound annual rate of 35% through 2028, which would result in more than $2.5 billion in revenue that year.

Here's why I think Upstart could double by the end of 2026

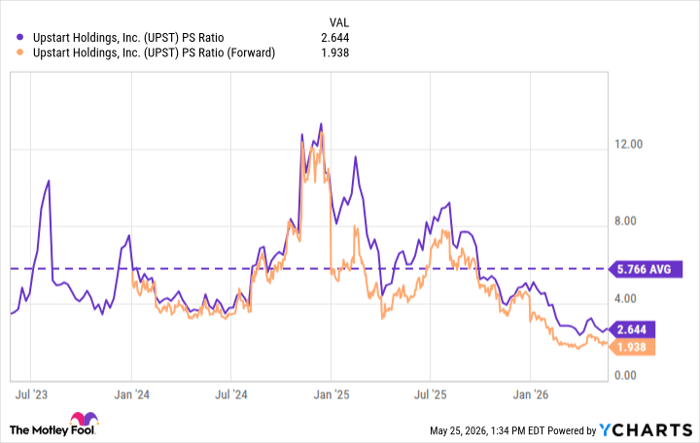

Based on Upstart's trailing-12-month revenue of $1.1 billion, its stock is trading at a price-to-sales (P/S) ratio of 2.6. That is a steep discount to its three-year average of 5.7, suggesting the stock is undervalued right now.

Moreover, if we assume Upstart generates $1.4 billion in revenue this year as expected, then its forward P/S ratio is just 1.9.

UPST PS Ratio data by YCharts

That means Upstart stock would have to climb by 36% by the end of this year just to maintain its current P/S ratio, and it would have to soar by a whopping 200% to trade in line with its three-year average P/S ratio of 5.7. I think the likely outcome will be somewhere in between, which is why I feel the stock could double.

I intend to hold this stock for the long term, because if AI does take over credit assessment on a global scale, then Upstart will be staring down the barrel of a trillion-dollar annual revenue opportunity. Capturing even a fraction of the market could lead to blistering returns for shareholders.

Should you buy stock in Upstart right now?

Before you buy stock in Upstart, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Upstart wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $477,813!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,320,088!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 27, 2026.

Anthony Di Pizio has positions in Upstart. The Motley Fool has positions in and recommends Upstart. The Motley Fool recommends Fair Isaac. The Motley Fool has a disclosure policy.

Recommended Articles