Prediction: D-Wave Quantum Stock (QBTS) Will Be Worth This Much by the End of 2026

Key Points

D-Wave Quantum has made headlines as a pioneer in quantum computing technology.

The company's technology has garnered commercial traction, but adoption remains extremely limited.

D-Wave's weak financial profile and lofty valuation are reminiscent of the way tech stocks were priced during the dot-com bubble.

- 10 stocks we like better than D-Wave Quantum ›

There is a version of the narrative around D-Wave Quantum (NYSE: QBTS) that reads like science fiction turned into an investable reality. Then there is the version where investors look at the cold, hard financial profile of the company.

Right now, retail investors are trading on the first version of the story. But smart investors should focus on the second, and avoid following the optimistic crowd into D-Wave Quantum.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

What does D-Wave Quantum do?

Quantum computers operate in a way that is counterintuitive, and wildly different from how the classical computers that we are all familiar with do. While traditional devices hold and process all of their data in bits as binary code -- 1s and 0s -- quantum systems process information using "qubits," which can also hold complex probability states through a property called superposition. Precisely how they capitalize on that property to perform computations is a level of detail most investors can skip -- but the key point is that, in theory, quantum computers should be able to rapidly perform unusual and extremely complex computations that would take a traditional supercomputer years (or centuries) to complete.

D-Wave is following an unusual strategy in its industry: It's focused specifically on a technology called quantum annealing. On one hand, quantum annealing machines will be unsuitable for a host of workloads that more general-purpose quantum computers could handle. On the other hand, what they are ideally suited for are optimization problems, and those come up heavily in some of the most obvious use cases for quantum computing, including drug discovery, logistics optimization, financial modeling, and cryptography.

The artificial intelligence (AI) connection is obvious: As demand for more powerful computing systems rises alongside model training and inference, quantum computing advocates are framing the technology as the next frontier beyond traditional GPU superclusters.

Examining D-Wave's financial performance

D-Wave's financial profile is where enthusiasm collides with reality. During the first quarter of 2026, the company closed a record $33.4 million in bookings -- up 1,994% year over year. D-Wave also signed a $20 million agreement with Florida Atlantic University to install one of its Advantage2 quantum computers. Sounds impressive, right?

Well, consider this: Despite record bookings and flashy agreements, D-Wave only recognized $2.8 million of revenue during the first quarter. This represented an 81% year-over-year decline. Operating losses, meanwhile, came in at $46.8 million -- nearly 10 times as much as in the first quarter of last year.

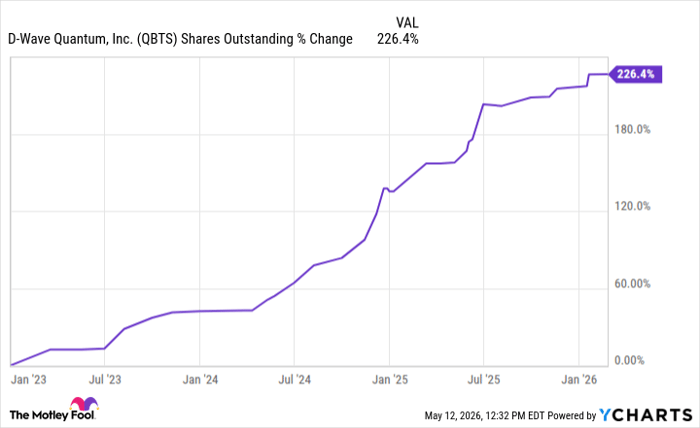

On top of all of this, the number of shares outstanding has grown by nearly 226% since the start of the AI revolution -- signaling a pace of dilution that sacrifices the positions of existing shareholders to fund operations, even as the company has no clear path to profitability.

QBTS Shares Outstanding data by YCharts.

With a market cap hovering near $8 billion, negligible revenue, and expanding losses, the implied price-to-sales (P/S) ratio of approximately 295 seems unjustified. D-Wave does not sport a growth premium; rather, its share price is rooted in a faith-based valuation.

Echoes of the dot-com boom

Investors who lived through 1999 and 2000 have seen this movie before. Back then, Cisco was the infrastructure darling that was building the pipes of the internet. The company's technology and use cases were real, and the stock ran to a frothy valuation, implying the good times would never end.

But when the bubble burst, Cisco's shares fell by roughly 83% from their peak, and the stock didn't return to that peak until December 2025. The parallel with D-Wave is not that quantum computing is vaporware. It's that the market is pricing D-Wave as though quantum computing is already generating record profits and dominating AI ecosystems.

None of these things is true right now. But what is true is that a company generating inconsistent and nominal revenue is valued in the billions. A single disappointing quarter or yet another capital raise could fuel a rotation out of this speculative tech stock and trigger the kind of harsh de-rating that leaves investors holding the bag. By year's end, I think shares of D-Wave could be trading for under $10.

Should you buy stock in D-Wave Quantum right now?

Before you buy stock in D-Wave Quantum, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and D-Wave Quantum wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $469,293!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,381,332!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 18, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Cisco Systems. The Motley Fool has a disclosure policy.

Recommended Articles