Up 231%, Is RTX Proving Why It Was a Mistake for Honeywell to Replace RTX in the Dow Jones Industrial Average?

Key Points

Investor expectations for pure-play stocks like RTX tend to be more straightforward than those of companies with a lot of moving parts.

Honeywell's spinoffs could pay off even if it gets removed from the Dow.

All 30 Dow stocks were industry leaders at one point, but that's no longer the case.

- 10 stocks we like better than Honeywell International ›

The Dow Jones Industrial Average (DJINDICES: ^DJI) made headlines on May 14 after closing above 50,000. But the Dow would be even higher if Honeywell International (NASDAQ: HON) hadn't replaced Raytheon Technologies -- now RTX (NYSE: RTX) -- on Aug. 31, 2020. The change was part of a broader shake-up that swapped Salesforce for ExxonMobil and Amgen for Pfizer.

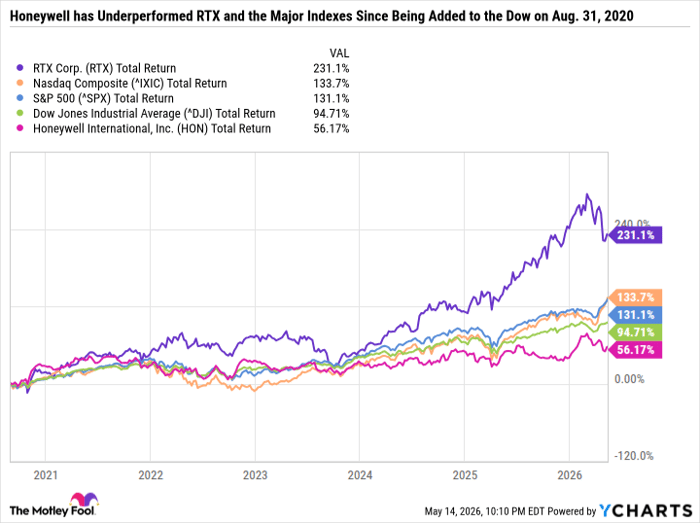

Between Aug. 31, 2020, and market close on May 14, Honeywell has delivered a mere 56.2% total return, compared with RTX's whopping 231.1%.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Here's why Honeywell was added to the Dow, why it has failed to live up to expectations, why its spinoffs could unlock growth, and why the index can sometimes make changes that don't pan out.

Image source: Getty Images.

Honeywell fit the Dow's tech-focused mold

The Dow has become far less of an "industrial" index, as its name implies, and more representative of the broader market, which is dominated by tech stocks. In 2024, Amazon replaced Walgreens Boots Alliance, Nvidia took Intel's seat, and Sherwin-Williams replaced chemical giant Dow Inc.

Although RTX and Honeywell are both industrial stocks, Honeywell was viewed as a much more innovative and diversified company in 2020. Its operational technology, products, components, and services span the aerospace industry, commercial buildings, industrial manufacturing, healthcare, oil and gas, military, and more. Honeywell Forge is an enterprise performance management and software-as-a-service suite that integrates with the physical world, bringing the Industrial Internet of Things (IIoT) to legacy industries. In sum, Honeywell had bold plans for rapid innovation across its segments by making existing industries smarter and more digitally connected.

Honeywell had been booted from the Dow in 2008 because of its relatively small earnings and revenue. Under that criteria, Honeywell had a strong case for being added back to the index now that it had grown into a multifaceted, highly influential conglomerate.

It was an exciting investment thesis, but it didn't pan out as investors hoped.

RTX Total Return Level data by YCharts

From innovative industrial giant to industry laggard

Honeywell spent years underperforming the broader market, with weak earnings and free-cash-flow growth. Supply chain and inflationary pressures were partly to blame, but Honeywell didn't do a good job with what it could control.

In November 2024, activist investor Elliott Investment Management amassed a more than $5 billion position in the stock and sent a letter to Honeywell's board of directors explaining why Honeywell should break up its conglomerate structure after years of underperforming its peers. Elliott argued that Honeywell's inefficiencies far outweighed the benefits of diversification from its conglomerate structure. Honeywell listened and, in December 2024, stated that it was open to a breakup.

Elliott's theory has proven correct (so far). Honeywell spun off Solstice Advanced Materials on Oct. 20, 2025. It's already gained 79.4%.

Last month, Honeywell said it now expects to spin off Honeywell Aerospace under the Nasdaq ticker symbol HONA on June 29, with the remaining business focusing on industrial and building automation.

The hope is that Honeywell will follow a similar path to GE by giving shareholders exposure to the three nimbler stand-alone companies rather than the bulky, centralized entity. On April 2, 2024, GE completed its split into three separate companies. GE Vernova, GE Aerospace, and GE HealthCare Technologies are now worth a combined $625.3 billion -- which is many multiples more than the pre-split value.

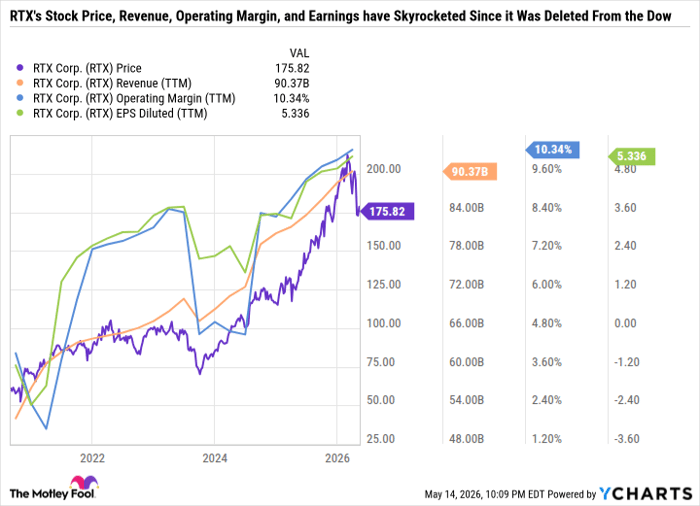

Honeywell was added to the Dow at a time when it was one of the largest U.S. industrial companies by market cap and had immense innovation potential. But its conglomerate structure held it back. Meanwhile, RTX maintained a focused investment thesis as a pure-play defense contractor. Reliable government contracts, paired with geopolitical tensions, have allowed RTX to steadily increase earnings while maintaining high margins and passing along profits to shareholders through a growing dividend.

RTX data by YCharts

Since Honeywell Aerospace is spinning off from Honeywell Automation, the automation business would likely be the one that remained in the Dow, at least for now. And under that new structure, RTX is more deserving of being in the index.

Not all blue chip stocks are buys

Honeywell's underperformance since being added to the Dow is a reminder that the index makes mistakes. It also reflects the value the market is putting on focused, innovative growth companies and its rejection of the conglomerate model.

The key takeaway for long-term investors is that just because a company has exposure to an exciting theme doesn't mean it will capitalize on it. Executing on a vision means having the right structure and management team. Honeywell's stodginess was its downfall. And its push toward digitalization and IIoT failed to meaningfully impact its bottom line.

The Dow is an excellent starting point for identifying industry leaders, many of which pay dividends. But investors should be aware of the market dynamics that existed when a component was included in the Dow, versus where the company is today. That context can help distinguish Dow stocks with clear runways for future growth from those that may deliver mediocre returns.

Should you buy stock in Honeywell International right now?

Before you buy stock in Honeywell International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Honeywell International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $469,293!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,381,332!*

Now, it’s worth noting Stock Advisor’s total average return is 993% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 16, 2026.

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Amazon, Amgen, GE Aerospace, GE HealthCare Technologies, GE Vernova, Honeywell International, Intel, Nvidia, Pfizer, RTX, and Salesforce. The Motley Fool recommends Sherwin-Williams. The Motley Fool has a disclosure policy.

Recommended Articles