SK Hynix vs. Micron: Which Memory Chip Is the Better Investment?

TradingKey - On April 9, industry sources revealed that SK Hynix's 1c DRAM yield has risen to 80%, with more than half of its production capacity switching to the new process this year and monthly output reaching 190,000 wafers by year-end as EUV equipment investment triples. This technology is the core of the next-generation HBM4E and will be used in NVIDIA ( NVDA )'s "Vera Rubin Ultra" AI accelerator, set for launch in the second half of next year, with the company planning to deliver samples within this year.

Earlier, on March 25, SK Hynix confidentially filed for a listing with the U.S. SEC, aiming to debut on the U.S. stock market via ADRs with a target listing date in the second half of 2026.

These moves coincide with a memory chip super-cycle: in the first quarter of 2026, DRAM contract prices skyrocketed by over 90% quarter-on-quarter, and NAND prices rose by more than 50%. Following Samsung's record quarterly profits on April 7, the South Korean semiconductor sector rallied the next day, with SK Hynix's share price gaining nearly 15% in a single day. SK Hynix's U.S. listing is more than just fundraising; it is a strategic layout for valuation recovery and technological positioning.

I. Why is SK Hynix's valuation lower than Micron's?

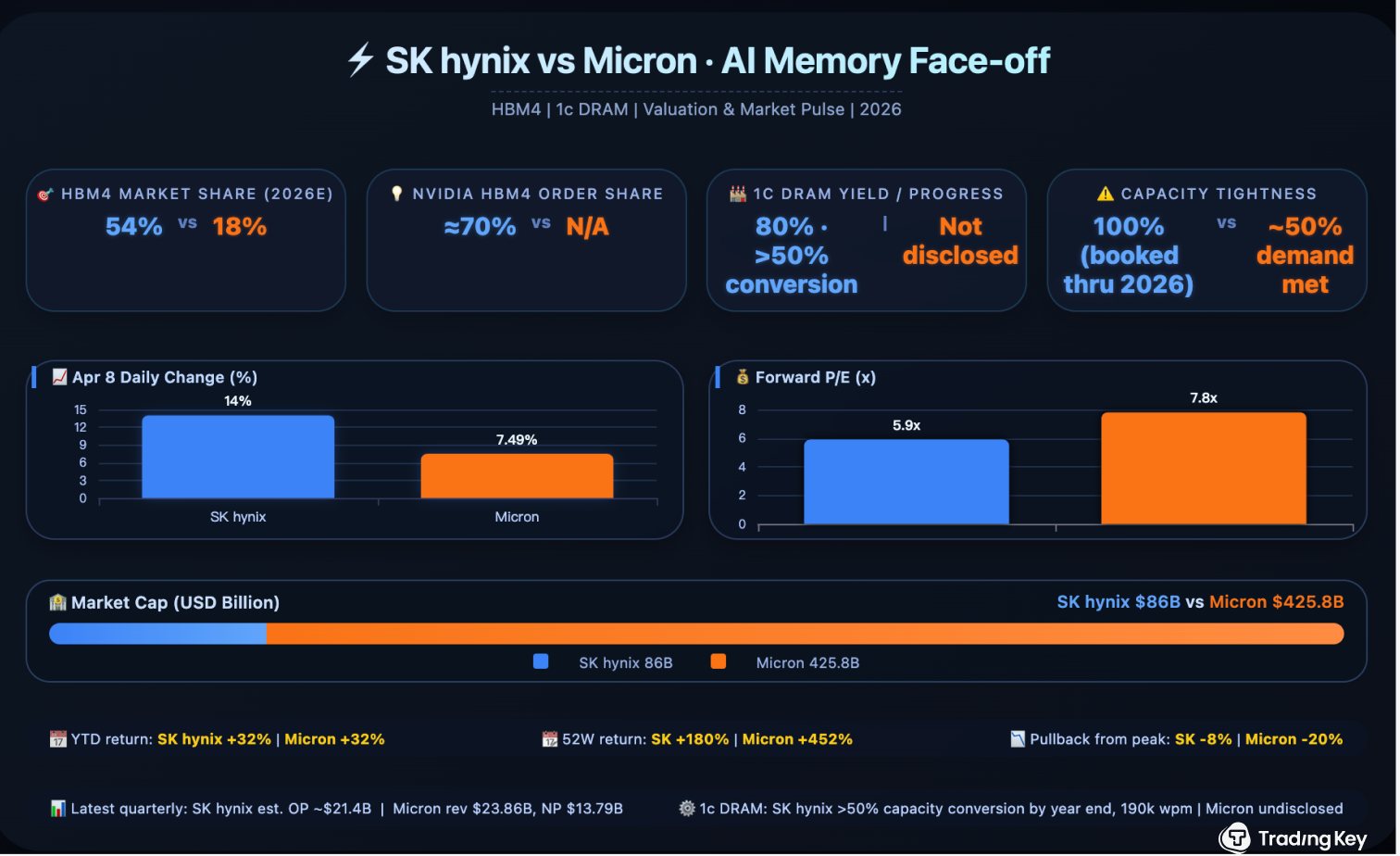

SK hynix holds a technological lead, yet its valuation on the South Korean stock market is lower than that of Micron ( MU ). Micron’s forward P/E ratio is approximately 7.8x, while SK hynix’s is only 5.9x—meaning for every $1 in earnings, Micron’s stock is valued at $7.80, whereas SK hynix’s is worth just $5.90. This is the so-called "Korea Discount," caused by factors including a retail-dominated market, opaque corporate governance at large conglomerates, and geopolitical risks.

However, SK hynix’s fundamentals are strong. It is expected to capture a 54% share of the next-generation HBM4 memory market by 2026 and has already locked in about 70% of the orders for Nvidia’s next-generation AI platform. If this U.S. listing succeeds, U.S. institutional investors will be able to buy its shares directly, and its valuation could align with its U.S. peers, similar to TSMC’s trajectory.

The plan involves issuing approximately 2%–3% in new shares to raise $9.6 billion to $14.4 billion. Since the amount of previously canceled treasury stock is roughly equal to the new issuance, the dilution for existing shareholders will be limited.

II. Why did SK Hynix shares surge nearly 15% in a single day?

On April 8, SK Hynix closed up nearly 13% (hitting nearly 15% intraday) at 1.033 million won. The immediate catalyst was Samsung's Q1 operating profit of 57.2 trillion won (up 800% year-over-year), setting a record for South Korean companies, coupled with the temporary U.S.-Iran ceasefire and easing geopolitical risks.

The deeper logic is that SK Hynix's DRAM, NAND, and HBM capacity is fully booked through the end of 2026. Microsoft ( MSFT ), Google ( GOOGL) and other cloud providers are even willing to pay 10%-30% down payments to secure three-year long-term contracts. Memory chips are transforming from cyclical commodities into 'infrastructure-grade' scarce resources. Hana Securities has raised its full-year operating profit forecast for SK Hynix by 47% with a target price of 1.6 million won.

III. How is SK Hynix widening its lead over Micron and Samsung?

HBM is the "crown" of AI chips, and 1c DRAM is the brightest jewel in that crown, directly determining the performance ceiling of HBM4 and HBM4E.

SK Hynix recently disclosed several key figures:

- Yield rate has reached 80% . For 10nm-class DRAM, an 80% yield indicates that the technology is highly mature and fully ready for mass production.

- Transitioning over half of production capacity within the year. SK Hynix plans to transition more than half of its DRAM production lines to the 1c process this year, aiming to secure a monthly capacity of approximately 190,000 wafers by year-end. This is an aggressive expansion plan.

- Investment in EUV lithography equipment has increased roughly threefold compared to the original plan. This equipment is an essential tool for producing 1c DRAM, and the increased investment shows the company's full confidence in this technology.

So, what is the connection between 1c DRAM and SK Hynix's AI business? The answer lies in HBM4E.

HBM (High Bandwidth Memory) is the "partner" of AI chips, responsible for delivering data to Nvidia's GPUs at high speeds. Each generation of HBM requires more advanced, power-efficient, and faster base DRAM chips. SK Hynix's 1c DRAM is precisely the core material being prepared for the next-generation HBM4E.

And who is the largest customer for HBM4E? Nvidia. Nvidia plans to launch its next-generation AI accelerator, the "Vera Rubin Ultra," featuring HBM4E in the second half of next year. SK Hynix must complete sample development within this year to keep pace with Nvidia.

80% yield, conversion of over half of production capacity within the year, and 190,000 wafers of monthly capacity— these three figures together send a clear signal: SK Hynix is not just providing lip service to its technological lead; it is committing substantial capital to convert that advantage into tangible production capacity. Once this capacity is unleashed, it will further widen the gap with Micron and Samsung.

IV. SK Hynix vs. Micron: Which is the Better Investment?

SK Hynix holds a clear lead in the HBM sector. . In the fourth quarter of 2025, SK Hynix accounted for 57% of global revenue in the HBM market, more than double that of Micron. For the next-generation HBM4, it has secured approximately 70% of Nvidia's orders, with its global market share projected to reach 54% by 2026, compared to just 18% for Micron.

SK Hynix holds a clear lead in the HBM sector. . In the fourth quarter of 2025, SK Hynix accounted for 57% of global revenue in the HBM market, more than double that of Micron. For the next-generation HBM4, it has secured approximately 70% of Nvidia's orders, with its global market share projected to reach 54% by 2026, compared to just 18% for Micron.

The gap may be even wider in 1c DRAM process technology. . SK Hynix has disclosed an 80% yield rate and aggressive capacity conversion plans, which positions it more favorably for the upcoming HBM4E competition. While Micron is also advancing its cutting-edge DRAM, it has yet to release progress data at a comparable level.

In the standard DRAM market, Micron is hot on its heels. . Micron's revenue for the most recent quarter reached $23.86 billion, a massive 196% year-over-year increase, with traditional DRAM being the primary contributor. The company provided very optimistic guidance for the next quarter, forecasting revenue as high as $34.25 billion. Micron's actual gross margin for the last quarter was approximately 75%, and the company expects it to rise to around 81% in the next quarter.

SK Hynix boasts superior technology, a fuller order book, and more aggressive capacity expansion, yet its valuation remains lower. This valuation mismatch is the most direct reason SK Hynix is seeking a U.S. listing.

5. Why is SK Hynix in a hurry to go public?

1: Industry reaching the peak of a supercycle

In the first quarter of 2026, DRAM prices surged by more than 90%, with a further increase of approximately 60% expected in the second quarter. Analysts believe this price rally has only just entered its "middle phase," and the real earnings explosion point may occur between the fourth quarter of 2026 and the second quarter of 2027. Going public during the industry peak allows for maximum capital raising and attracts the most attention.

2: Breakthrough in 1c DRAM technology; HBM4E launch imminent

Nvidia is set to launch the "Vera Rubin Ultra" featuring HBM4E in the second half of next year. As a major supplier, SK Hynix must complete capacity preparations before then. Building new factories, purchasing extreme ultraviolet (EUV) lithography equipment, and expanding R&D teams all require significant capital. The $9.6 billion to $14.4 billion raised through the IPO can be directly funneled into expanding 1c DRAM and HBM4E production capacity.

SK Hynix CEO Kwak Noh-jung stated that the company intends to use this listing to ensure it can make long-term, strategic investments under any circumstances and respond promptly to global customer orders. The company has also set a goal for "net cash to exceed 100 trillion won"—a massive leap from the current 12.7 trillion won, making the IPO a critical step.

3: Customer order books are full

SK Hynix accounts for approximately 70% of the HBM4 supply for Nvidia's next-generation AI platform, Vera Rubin, far exceeding the market's previous expectation of 50%. Now, as 1c DRAM yields improve, its market share is also expected to remain leading for the subsequent Vera Rubin Ultra platform.

Meanwhile, North American cloud giants such as Microsoft, Google, and Amazon are signing long-term agreements with SK Hynix, willing to pay a premium of 50%-60% over smartphone manufacturers to secure capacity. These long-term orders provide SK Hynix with stable revenue for years to come and provide the IPO with solid performance backing.

VI. Is the listing of SK Hynix bearish or bullish for Micron?

Micron has long been the only pure-play DRAM stock in the U.S. market, enjoying a "scarcity premium." The listing of SK Hynix ADRs will disrupt this landscape—U.S. investors now have a cheaper and more technologically aggressive alternative. A New York hedge fund manager remarked, "Short-term capital could flow from Micron to SK Hynix."

However, the impact may be short-term. KeyBanc analysts still raised their fiscal 2026 EPS forecast for Micron to $64.37, with a price target of $600 (representing roughly 60% upside from current levels). In the long run, the trajectories of the two companies may converge, as the HBM supply shortage benefits both.

VII. Key risks to consider before investing in SK Hynix.

SK Hynix's U.S. listing does not mean it can rest easy from now on. The memory chip industry is currently in a phase of intense competition among SK Hynix, Samsung, and Micron, and the future landscape may be reshaped by the following four factors:

- Samsung's Counterattack: Samsung has ordered approximately 20 state-of-the-art EUV lithography machines (valued at over 45 billion RMB) to expand 1c DRAM capacity; with peak chip performance, it aims to reclaim market share.

- Micron Catching Up: Micron has raised its 2026 capital expenditure to over $25 billion, expanding production at factories worldwide, and the gap in HBM4 validation is narrowing.

- Cyclical Downturn: Growth in the HBM market has slowed, and leading manufacturers have begun adjusting NAND capacity to prevent a price collapse.

- Geopolitics and Technological Iteration: Middle Eastern tensions are unsettling the market; the evolution of HBM from 3E to 4 and then to 4E represents a reshuffle with every generation, and SK Hynix may not lead forever.

VIII. How should investors view this?

SK Hynix’s pursuit of a US listing epitomizes the transformation of memory chips from "supporting characters" to "protagonists" and from cyclical commodities to strategic resources in the AI era. With an 80% yield on 1c DRAM, full production capacity, and massive orders from Nvidia in hand, the company is not just selling a narrative but relying on proven technical prowess.

Should the listing succeed, its valuation is expected to converge with Micron’s, diluting Micron’s "sole-player premium." For the first time, investors will be able to allocate to two pure-play DRAM stocks in the US market simultaneously, with the valuation gap providing room for long-short strategies.

Of course, cyclical fluctuations, technological iterations, and the fierce competition among the "Big Three" all signal risks. As Kwak Noh-jung noted: "Although the company stands at the center of the AI era, its valuation in global markets remains insufficient." A Wall Street debut in the second half of 2026 will mark a pivotal step for SK Hynix as it transitions from a "Korean champion" to a "global titan."

Recommended Articles