Federal Reserve set to hold interest rates in Warsh's debut as chair

- The US Federal Reserve is expected to leave the policy rate unchanged for the fourth consecutive meeting in June.

- The revised Summary of Economic Projections will provide key clues on potential rate hikes.

- All eyes will be on the new Fed Chair Kevin Warsh’s comments.

The United States (US) Federal Reserve (Fed) announces its interest rate decision on Wednesday, another pivotal meeting for markets to gauge the stance of policymakers and new Chair Kevin Warsh as energy prices retreat after the United States and Iran reached a framework deal to reopen the Strait of Hormuz.

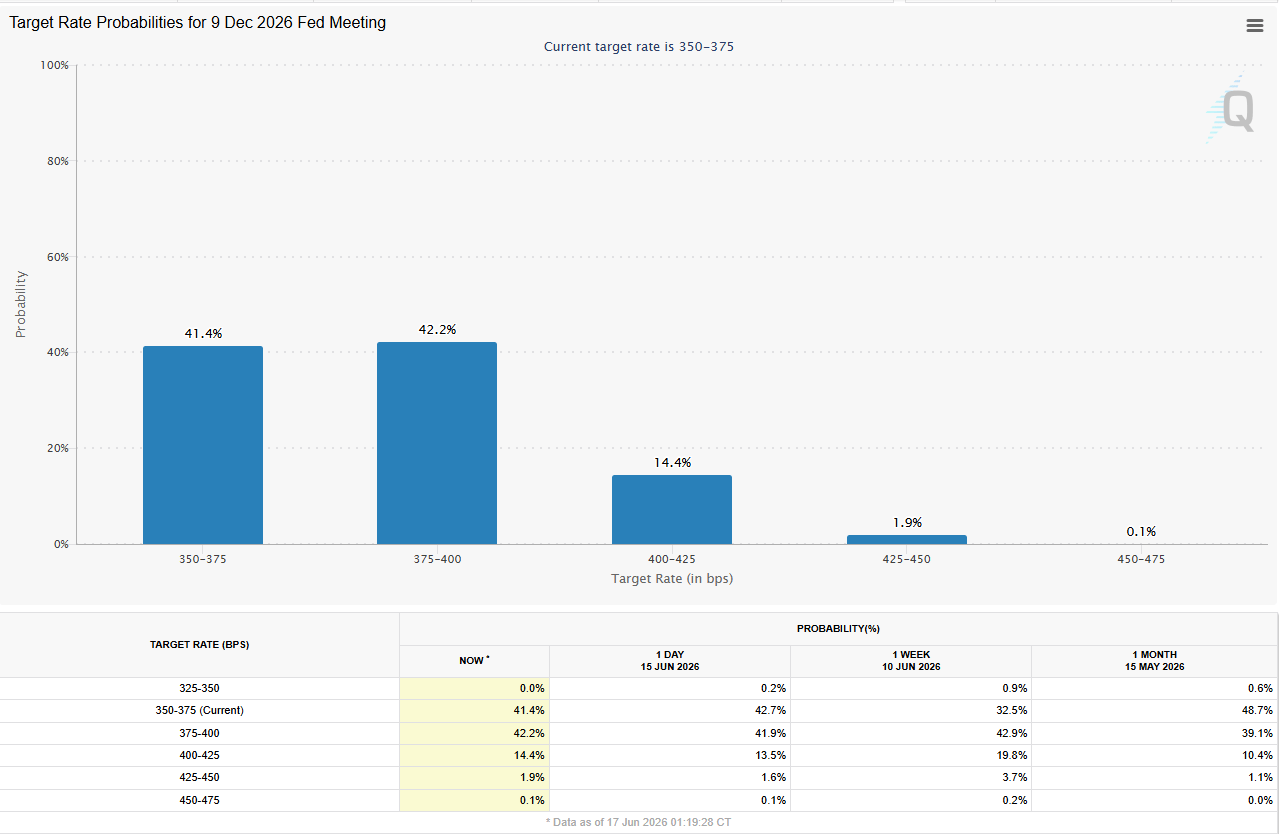

Markets widely expect the Federal Open Market Committee (FOMC) to keep interest rates unchanged in the range of 3.5%-3.75% for the fourth consecutive meeting in June.

As this decision is fully priced in, the revised Summary of Economic Projections (SEP) and Fed Chair Warsh’s comments in his first post-meeting press conference will grab all the attention as they could offer key clues on the policy outlook and thus drive the US Dollar’s (USD) performance.

Despite the recent decline in crude Oil prices, markets still see a relatively strong probability of the Fed tightening the policy later in the year. According to the CME FedWatch Tool, investors are currently pricing in about a 58% probability that the Fed will raise the interest rate by 25 basis points (bps) at least once by end-2026.

After fluctuating at around $65 per barrel before the US and Israel launched a joint attack on Iran on February 28, the West Texas Intermediate (WTI) rose to its highest level since June 2022 above $110 by mid-March. Since the first temporary ceasefire agreement between the US and Iran was announced in early April, Oil prices corrected lower but remained elevated relative to pre-war levels. With the latest deal finally paving the way for the reopening the Strait of Hormuz, WTI declined further and broke below $80.

Policymakers will take this development into account when penciling down their macroeconomic projections and interest rate expectations.

Previewing the Federal Open Market Committee (FOMC) meeting, “the policy rate will remain unchanged with likely hawkish changes in communications,” said TD Securities analysts.

“The easing bias will be dropped with hawkish adjustments to the SEP and dot plot. The uncertainty lies in new Fed Chair Warsh's press conference. A strong pushback from Warsh is unlikely as that would damage his credibility and effectiveness towards his long-term, reform-minded agenda,” they added.

When will the Fed announce its interest rate decision and how could it affect EUR/USD?

The Fed is scheduled to announce its interest rate decision and publish the monetary policy statement, alongside the SEP at 18:00 GMT. This will be followed by Fed Chair Kevin Warsh’s press conference starting at 18:30 GMT.

The latest SEP published in March showed that policymakers’ median projection pointed to a 25 basis points (bps) cut this year, unchanged from the SEP published in December 2025. It won’t be a surprise if there are hawkish revisions in the SEP given the changes in the macroeconomic backdrop.

Nevertheless, the market positioning suggests that the USD has room on the upside if the document shows that a majority of policymakers project at least one rate hike by the end of the year. In this scenario, market participants could continue to price in a rate hike and fuel another leg higher in US Treasury bond yields and the USD, causing EUR/USD to stretch lower.

Conversely, the USD could come under pressure if the SEP shows that a majority of policymakers expect to keep the policy rate unchanged for the rest of the year. Although this would still be a hawkish revision when compared to the March SEP, it would still be a less hawkish outlook than what markets are currently expecting. In this case, EUR/USD could gather recovery momentum.

Comments from Warsh in the post-meeting press conference could also drive the USD’s valuation. If Warsh pushes back market expectations for a rate hike and adopts an optimistic tone about the inflation outlook, now that Oil prices are coming back down, the USD could struggle to find demand. In the less likely scenario, Warsh could acknowledge strong labor market data and refrain from delivering a dovish message.

ING strategists Francesco Pesole, Chris Turner and Frantisek Taborsky note that the US Dollar (USD) is supported by strong US data and Fed expectations despite sharply lower Oil prices.

"The Dollar can stay resilient, but needs a nod from policymakers (especially from new Chair Kevin Warsh) that rate hikes are a real possibility,” they add. “This keeps questions around the durability of the oil sell-off open, and FX markets are, for now, reluctant to fully price in that optimism.”

In summary, the USD’s valuation, and EUR/USD’s performance, will depend on how convinced Fed policymakers are of a quick return to disinflation. Unless there is a clear message, either within the SEP or from Chair Warsh, that policy-tightening is no longer the preferred path forward, any weakening in the USD could remain short-lived.

Eren Sengezer, European Session Lead Analyst at FXStreet, provides a short-term technical outlook for EUR/USD:

“The technical outlook is yet to point to a bullish reversal. On the daily chart, the Relative Strength Index (RSI) recovered but is yet to make a decisive breakthrough 50. Additionally, EUR/USD remains well below the 100-day and 200-day Simple Moving Averages (SMAs).”

“On the upside, a key resistance area seems to have formed at 1.1655-1.1675, where the Fibonacci 38.2% retracement of the February-April downtrend, the 100-day SMA and the 200-day SMA converge. In case EUR/USD manages to clear this area, it could face an interim resistance at 1.1730 (Fibonacci 50% retracement) ahead of 1.1800 (Fibonacci 61.8% retracement).”

“Looking south, the first support level could be spotted at 1.1560 (Fibonacci 23.6% retracement) before 1.1500 (static level, round level) and 1.1410 (March 13 low).”

Warsh, at the helm of a hawkish-leaning Fed

New Fed Chair Warsh inherits a committee that consists of mostly hawkish voting and non-voting members. Dallas Fed President Lorie Logan, Cleveland Fed President Beth Hammack and Minneapolis Fed President Neel Kashkari stand out as the most hawkish voters, according to the FXStreet Speechtracker scores.

In a speech on May 27, Kashkari scored 7.4/10 on the FXS Speechtracker, modestly above the 7/10 historical average and thus slightly more hawkish relative to the established baseline. The speech leaned clearly toward vigilance on inflation as he stressed that the risk to the US inflation now outweighs the risk of labour-market deterioration. Kashkari also noted that most post-April data point to higher inflationary risks and that a Middle East war shock could keep global price pressures elevated.

Fed’s Logan delivered a distinctly more hawkish tone on June 3, with an FXS Speechtracker score of 8.2/10. The remark that “inflation is trending toward the mid-2s, not all the way to 2%” and that trimmed-mean inflation is “not currently a reliable signal,” alongside comments that financial conditions are accommodative, the labor market is stable, and corporate earnings are “going gangbusters,” underscored concern that inflation is taking too long to return to target. By stressing that monetary policy is not restraining the economy and expressing increasing concern that higher interest rates could be necessary later this year, the speech pushed the policy narrative further into hawkish territory.

If Warsh intends to convince policymakers of the need for policy-easing, he will have an uphill battle. Some of the more neutral members, such as New York Fed President John Williams and Fed Governor Jerome Powell, could be inclined toward holding settings steady but they are unlikely to support rate cuts until there is convincing evidence that inflation is moving back toward the target, or there is a persistent and clear deterioration in labor market conditions.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions. The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

Recommended Articles