Eurozone Q3 GDP: Sustained Recovery and Low Interest Rates to Keep Driving European Stocks Higher

TradingKey - On 14 November, Eurostat will release the revised GDP data for the Eurozone’s third quarter. The consensus expects the figures to remain consistent with the initial estimate published on 30 October, meaning the real GDP grew by 0.2% quarter-on-quarter and 1.3% year-on-year in Q3. If in line with expectations, this will reflect a modest recovery of the Eurozone economy in the third quarter. Looking ahead, the Eurozone economy is expected to sustain its recovery momentum, supported by three key drivers: policy support, improved domestic demand and industrial upgrading. The economic recovery has reduced the necessity and urgency for the European Central Bank (ECB) to continue cutting interest rates, while the low inflation level has constrained its hawkish tendencies. Overall, the benchmark interest rate is projected to remain at 2.15% in December, with a potential 25-basis-point cut in the first half of next year.

Under the impetus of economic recovery and the coordinated efforts of monetary and fiscal policies, we are optimistic about the performance of European equities over the next 12 months. Passive investors can look into European equity ETFs such as VGK and EZU. Active investors can pay attention to cyclical and liquidity-sensitive sectors and individual stocks, including Deutsche Bank (DB) and Banco Santander (SAN) in the banking sector, Siemens (SIE.DE) and Schneider Electric (SCHN.DE) in the industrial and materials sectors, as well as ASML (ASML) and SAP (SAP.DE) in the technology sector.

1. Economic Growth Rate

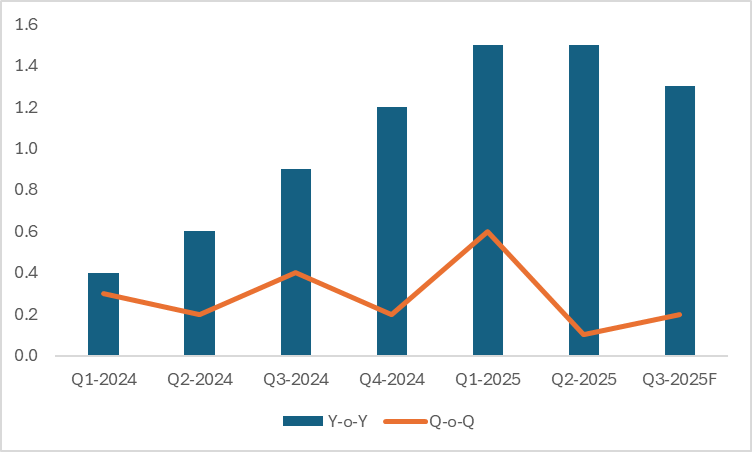

The Eurozone economy staged a modest recovery in the third quarter. The flash estimate of quarter-on-quarter (q-o-q) growth in real GDP for Q3, released on 30 October, came in at 0.2%. The revised figure, to be published on 14 November, is expected to remain unchanged, above the 0.1% q-o-q growth recorded in Q2 (Figure 1). By country, France achieved a 0.5% growth rate driven by robust increases in investment and exports. Spain and Portugal posted growth of 0.6% and 0.8% respectively. As Europe’s largest economy, Germany saw weak economic performance with zero q-o-q GDP growth in Q3, weighed down by a further decline in foreign trade exports.

From a year-on-year perspective, the Eurozone's economic growth has shown a gradual recovery trend since the start of last year. This is attributed to three key factors: first, falling energy prices have eased cost pressures, inflation has continued to cool, and household purchasing power has gradually recovered. Second, the labour market remains robust, with employment growth and rising real wages supporting private consumption, which has become the main driver of economic growth. Third, the shift toward accommodative monetary policy—including the ECB’s rate cut expectations and subsequent interest rate reductions—has relieved financing strains and boosted corporate investment as well as market confidence.

Looking ahead, the Eurozone economy is likely to maintain its recovery, supported by three core drivers: policy backing, improved domestic demand, and industrial upgrading. First, coordinated policy efforts underpin growth. The ECB’s low interest rates have gradually eased financing conditions, reviving credit provision and sustaining liquidity support for corporate investment and household consumption. Core economies like Germany have increased spending on infrastructure and national defence, with fiscal and monetary policies working in tandem to effectively mitigate the impact of trade uncertainties. Second, the domestic demand market is recovering steadily. The labour market is expected to remain robust, with falling unemployment and rising real wages significantly boosting household purchasing power. Consumer credit is staging a steady recovery, and retail demand is gradually picking up, injecting endogenous momentum into economic growth. Finally, emerging industries are leading growth. The acceleration of the digital economy and green transition, coupled with substantial investment increases in new energy, artificial intelligence and other sectors, has fostered new growth engines. Strengthened intra-regional industrial chain coordination and a stabilising manufacturing sector will further consolidate the recovery trend. However, it is noteworthy that the complex global trade environment and rising geopolitical uncertainties pose potential risks of a slowdown in the euro area’s economic growth.

Figure 1: Eurozone Real GDP (%)

Source: Refinitiv, TradingKey

2. Inflation and Monetary Policy

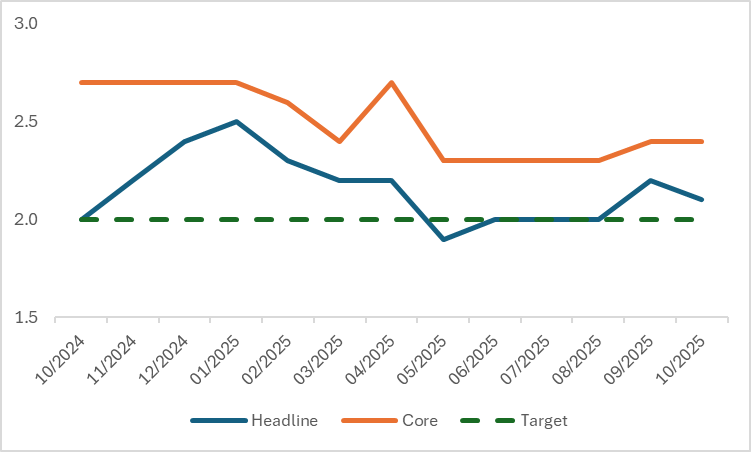

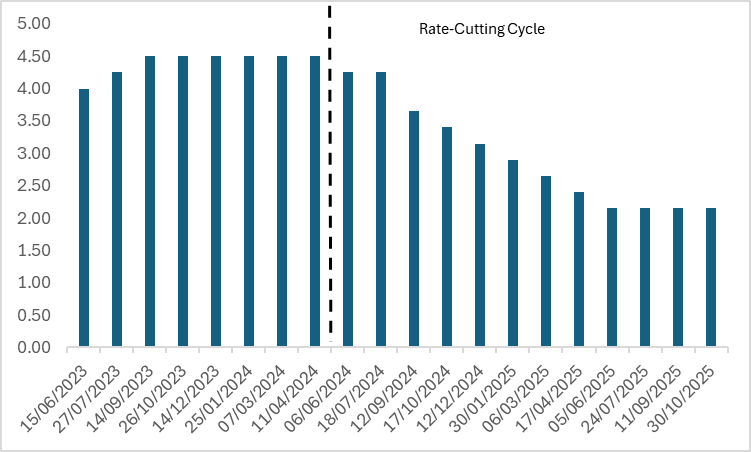

Inflation in the Eurozone has been on a gradual downward trend since the end of 2022. Over the past year, both headline CPI and core CPI have fallen to around the ECB’s 2% target (Figure 2.1). Looking ahead, against the backdrop of declining inflation stickiness, low energy prices, and the difficulty in forming a wage-inflation spiral, the probability of a sharp surge in Eurozone CPI in the coming quarters is expected to be low. Regarding monetary policy, weakened economic recovery momentum has reduced the necessity and urgency for the ECB to continue cutting interest rates, while low inflation has constrained its hawkish tendencies. Overall, after the ECB paused interest rate cuts in June this year, it is expected to keep the benchmark interest rate unchanged at 2.15% in December (Figure 2.2), with a further 25 basis points cut likely in the first half of next year.

Figure 2.1: Eurozone CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 2.2: ECB Policy Rate (%)

Source: Refinitiv, TradingKey

3. European Equities

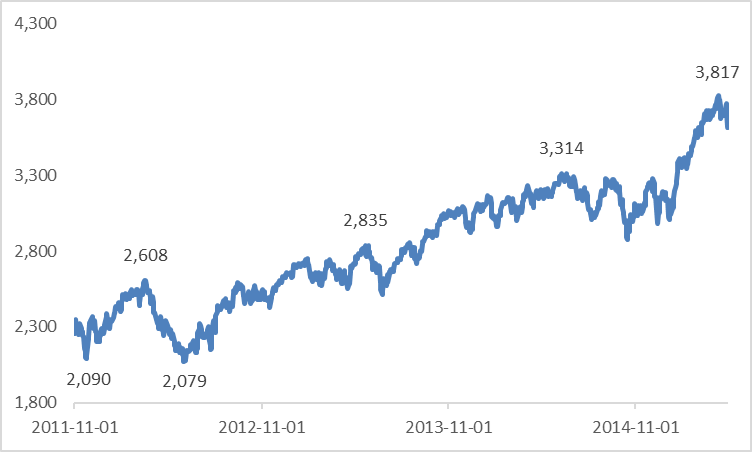

Low interest rates and accommodative monetary policies provide market liquidity, which is supportive of European equities. Historical data show that during the previous low-interest-rate cycle began in November 2011 (the early stage of the Eurozone debt crisis), European equities continued to strengthen in the following years (Figure 3). This was mainly driven by capital inflows and low financing costs that encouraged the private sector to increase equity holdings. Unlike 2011, when fiscal austerity constrained policy space, the current environment features the parallel implementation of Europe’s "rearmament" plan and Germany’s "whatever it takes" stimulus policies. Fiscal expansion is expected to underpin economic growth. Supported by economic recovery coupled with coordinated monetary and fiscal easing, we are bullish on European equities over the next 12 months. Passive investors can look into European equity ETFs such as VGK and EZU.

Amid economic recovery and a low-interest-rate environment, the most benefited sectors are concentrated in cyclical and high liquidity-sensitive areas. Active investors can pay attention to the financial sector, especially bank stocks. Widening net interest margins will drive profitability, with Deutsche Bank (DB) and Banco Santander (SAN) as core leaders in this sector. The industrial and materials sectors stand to gain from infrastructure and green investments, where Siemens (SIE.DE) and Schneider Electric (SCHN.DE) are expected to deliver outstanding performance. In the technology sector, ASML and SAP (SAP.DE), driven by demand for AI and digitalisation, are likely to perform impressively.

Figure 3: Performance of the Euro Stoxx 50 Index in a Low-Interest-Rate Environment Since the End of 2011

Source: Refinitiv, TradingKey

4. Conclusion

In summary, the Eurozone economic recovery is well underway. Furthermore, driven by the coordinated efforts of monetary and fiscal policies, we are optimistic about the performance of European equities over the next 12 months. Passive investors can look into European equity ETFs such as VGK and EZU. Active investors can pay attention to cyclical and liquidity-sensitive sectors and individual stocks, including Deutsche Bank (DB) and Banco Santander (SAN) in the banking sector, Siemens (SIE.DE) and Schneider Electric (SCHN.DE) in the industrial and materials sector, as well as ASML (ASML) and SAP (SAP.DE) in the technology sector.

Recommended Articles