ADP Report expected to show a mild rebound in employment in October

- US President Donald Trump says Iran talks to begin Monday after canceling attack

- Gold rallies to two-week high as USD softens on Iran deal hopes, receding Fed hike bets

- WTI trades with positive bias below mid-$79.00s on Iran uncertainty, supply concerns

- Bitcoin Falls Below $63,000; Can US-Iran Negotiations Reverse the Downtrend?

- WTI holds losses around $82.50 on renewed US-Iran diplomatic hopes

- Today’s Market Recap: Dow and S&P 500 Hit Fresh Record Highs, Tech Stocks Lead Gains, Palantir Surges 29%, ARM Rises Over 17%

The ADP Employment Change report is expected to show a modest improvement in private sector payrolls in October.

The ADP report will gain relevance in the absence of other labor market data releases.

The US Dollar is trading firm following the Fed’s hawkish pivot last week.

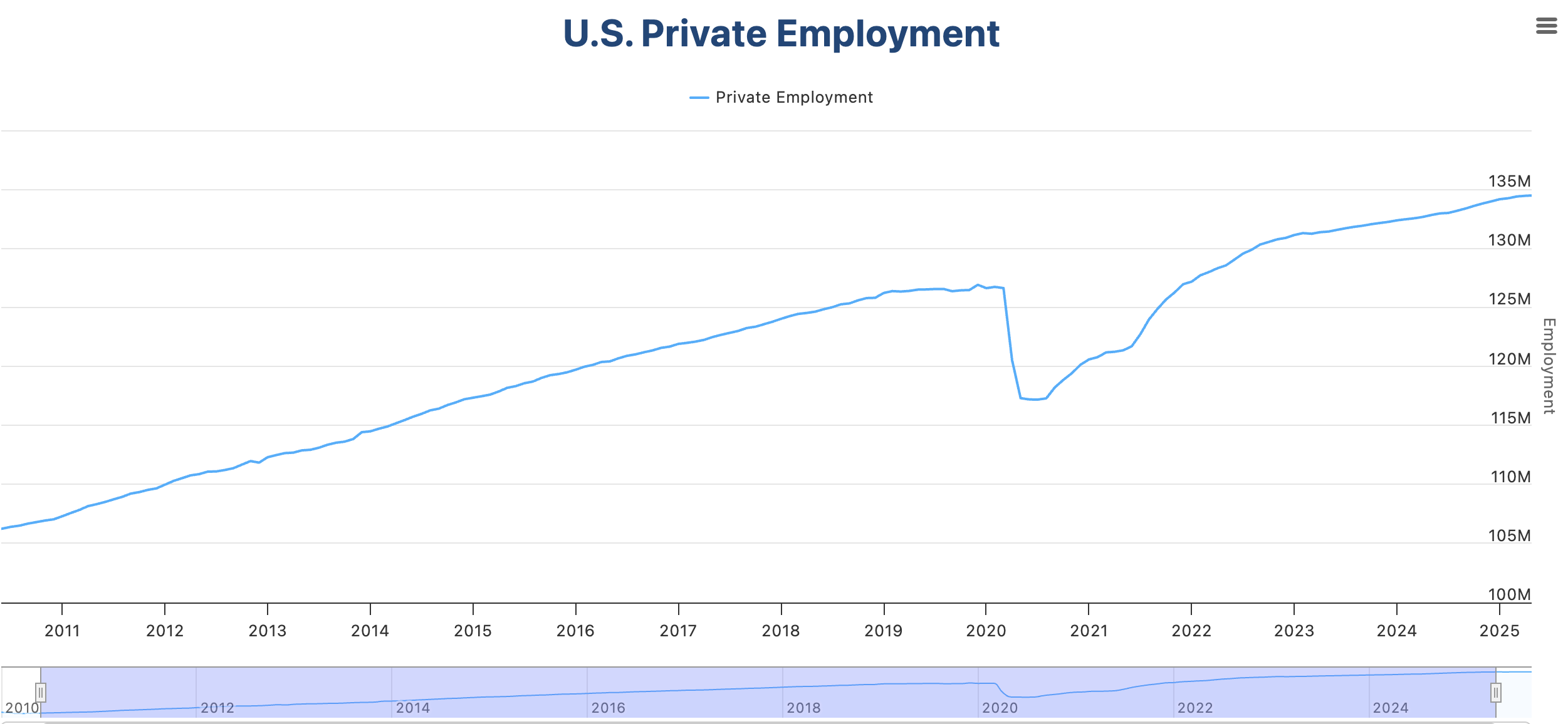

The Automatic Data Processing (ADP) Research Institute will release its monthly report on private-sector job creation for October on Wednesday. The so-called ADP Employment Change report is expected to show that the United States (US) economy created 24,000 new positions, following a 32,000 net decline in September.

These figures will attract particular interest this month, as the US Government shutdown extends for the fifth week already, and is highly likely to deprive the market and the Federal Reserve (Fed) of the closely watched JOLTS Job Openings and the key Nonfarm Payrolls (NFP) report this week.

ADP Jobs Report: Employment and the Federal Reserve

The mounting evidence of the US labour market’s deterioration has been a key factor in prompting the Federal Reserve to cut rates by 25 basis points on October 29, and remains a major concern for the dovish members of the Monetary Policy Committee (MPC), which keeps pushing for a more supportive policy.

Against this background, October’s ADP report seems unlikely to give reasons to celebrate. Private sector payrolls are expected to have bounced up, almost fully reverting September’s decline, but still showing numbers consistent with a weak labour market.

Preliminary estimates released by ADP last week revealed that net employment showed an average growth of 14,250 jobs in the four weeks ending on October 11, and the market consensus anticipates 24,000 new jobs in October. These figures would partially offset the 32,000 decline witnessed in September, yet they stand at levels well below the 150,000 average new jobs created per month over the last 15 years.

From the monetary policy perspective, the ADP is highly likely to confirm the challenging situation ahead for the Fed, which will have to fine-tune its monetary policy between a weak labor market and higher inflationary risks. This situation has created a wide divergence among policymakers, which was pointed out by Fed Chairman Jerome Powell as the main reason for cooling hopes of further monetary easing in December.

As it stands, chances of a 25 basis points rate cut in December have declined to 64% from above 90% last week. This has been one of the main drivers for the recent US Dollar (USD) recovery. In this case, a strong ADP reading might ease fears about employment and shift the focus back to inflation, endorsing Powell’s hawkish view and providing an additional impulse to the US Dollar.

Another disappointment, on the other hand, and especially if there is a further decline in net jobs, would likely boost pressure on the central bank to keep lowering borrowing costs and, in turn, send the US Dollar lower.

When will the ADP Report be released, and how could it affect the USD Index?

ADP will release the US Employment Change report on Wednesday at 13:15 GMT, and it is expected to show that the private sector added 24,000 new positions in October.

Heading into the release, the US Dollar appreciated against its main peers after the “hawkish cut” delivered by the Federal Reserve last week. The US Dollar Index (DXY) has rallied nearly 1.3% since then, reaching the 100.00 psychological level.

From a technical perspective, Guillermo Alcala, Analyst at FXStreet, highlights the resistance area above the 100.00 pshycholkigical level: “The US Dollar Index is on a bullish cycle amid dwindling hopes of Fed interest rate cuts but the Relative Strength Index (RSI) is approaching overbought levels in most timeframes as price action nears an important resistance level between 100.00 and August’s peak, at 100.25. A bearish correction from these levels should be considered.”

Downside attempts, however, are likely to remain limited, says Alcala: “A potential pullback from current levels is likely to find support at the October 9 high near 99.55 or the October 30 low, at the 98.90 area. To the upside, above 100.25, the targets are the May 29 high near 100.55, and the May 16 high, at 101.25.”

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.