CoreWeave Q3 2025 Earnings Analysis: Short-Term Hypergrowth vs. Long-Term Leverage Risks—Trading Opportunity or Trap?

- Gold Prices Under Pressure After Hitting $4,600, UBS: Safe-Haven Logic Unchanged But Only Delayed.

- US-Iran Rift Persists, Will Gold Rise or Fall Next?

- Gold rallies on hopes for US-Iran talks and falling US Treasury yields

- Gold Price Forecast: XAU/USD opens lower around $4,450 on fears of widening Iran conflicts

- USD/JPY Hits 160.00 Mark, Will Japanese Government Intervene? Will the Currency’s Rally Be Contained?

- Seesaw Effect Continues. US Pre-Market Three Major Index Futures Weaken, Oil Prices Rise, Bitcoin Drops Below 68,000 Mark

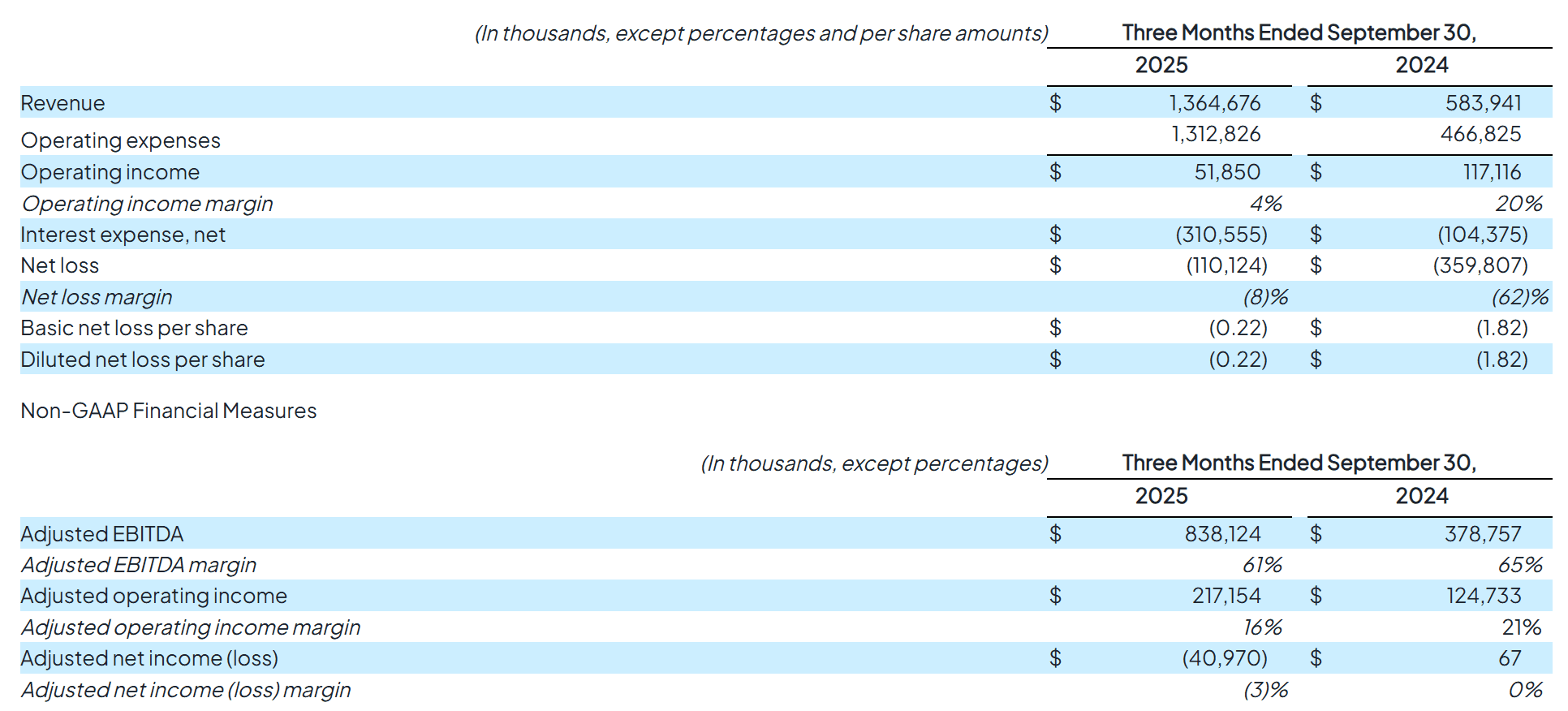

CoreWeave’s Q3 earnings report paints a dramatic tug-of-war picture. Fueled by sustained robust demand for AI training and inference, revenue hit a record $1.36 billion, surpassing expectations of $1.29 billion; net loss narrowed to $110 million, far better than the analyst consensus of ~$300 million. Boosted by the news, the stock surged as much as 6% in after-hours trading. However, this positive sentiment quickly reversed. As earnings details emerged, the share price flipped to a sharp decline, dropping over 7% at one point. This reversal exposes the core contradiction in CoreWeave’s growth narrative: Is this a buying opportunity right now, or a potential trap?

CoreWeave’s Business Model

The AI infrastructure market is on the cusp of hypergrowth, and CoreWeave is a prime beneficiary. Its business model is straightforward: procure the latest and scarcest GPU chips (e.g., GB200/GB300 series) from its deeply tied partner NVIDIA, install them in data center servers, and rent out the compute power under long-term commitment contracts to hyperscale clients like Microsoft and OpenAI, locking in stable revenue for years ahead. These contracts not only generate 15%-25% upfront payments for immediate cash flow, but their high-credit receivables can also serve as collateral for new rounds of debt financing, fueling GPU purchases and scale expansion in a self-reinforcing capital-business loop.

What sets CoreWeave apart is its optimization of servers for AI workloads, enabling hyperscale enterprises to access required compute capacity instantly without waiting for new infrastructure builds.

CoreWeave’s Competitive Advantages and Moat

50%+ GPU Utilization: Extreme Efficiency Optimized for AI

Unlike traditional hyperscalers reliant on centralized general-purpose clouds, CoreWeave positions itself as a specialized AI infrastructure provider. Its model encompasses custom hardware orchestration, vertically integrated data center ownership, and a sophisticated software stack. As a result, CoreWeave achieves GPU utilization rates exceeding 50%, far above the 15%-25% of legacy providers. This translates to delivering more effective compute for the same hardware investment or lower costs for equivalent output.

NVIDIA “Iron Triangle”: Triple Bind as Shareholder, Supplier, and Customer

CoreWeave’s other core edge lies in its deep entanglement with key AI ecosystem players, forming a formidable moat through shareholder, supplier, and customer relationships. NVIDIA is not only the primary GPU supplier but also holds ~7% equity stake and leases compute from CoreWeave via reverse agreements. This tie-in ensures CoreWeave gains access to NVIDIA’s latest GPUs 5-8 months ahead of competitors, seizing technological and market first-mover advantages.

Furthermore, CoreWeave has forged strategic partnerships with top AI firms. OpenAI is both a shareholder and its largest compute partner, with a multi-billion-dollar long-term deal. Microsoft, contributing over 60% of 2024 revenue as the top client, locks in resources via extended contracts. This model aligns CoreWeave’s growth tightly with AI leaders, preemptively securing core demand.

Interpreting CoreWeave’s Latest Performance Metrics

Revenue: 134% Surge Followed by Unexpected Guidance Cut

Q3 revenue soared 134% YoY to $1.365 billion, but the company slashed its full-year 2025 guidance from a high of $5.35 billion to a range of $5.05-$5.15 billion. The downgrade stems directly from “third-party data center developer delays,” pushing Q4 planned capacity and revenue recognition into future periods. This underscores that CoreWeave is not a pure software platform but a capital-intensive infrastructure player constrained by physical construction, power supply, and supply chain bottlenecks.

Profitability: Operating Margin Crashes to 4%, Interest Devours Earnings

Despite explosive revenue growth, total operating expenses skyrocketed from $467 million YoY to $1.313 billion, causing operating income to plummet 55% to $51.85 million and the operating margin to collapse to just 4%. This disconnect highlights diminishing marginal returns from scale. The company likely pays premium prices for scarce GPUs and power capacity, eroding pricing power.

Net interest expense nearly tripled from $104 million YoY to $310 million, reflecting the heavy debt burden from aggressive capex plans. Although net loss narrowed on the surface, operating profit was entirely consumed by interest, revealing a perilous capital cycle: massive debt is needed to fund capex for order fulfillment, yet interest eats into profitability. Even adjusted EBITDA and operating margins lagged last year’s levels, indicating a genuine decline in core operational strength.

Balance Sheet and Capital Expenditures

As of Q3-end, the company held $3 billion in cash and equivalents, providing ammunition for near-term expansion. Construction in progress rose $2.8 billion QoQ to $6.9 billion, representing committed but uncommissioned infrastructure. Q3 capex totaled $1.9 billion, which management admitted was “below expectations”—directly tied to third-party data center delays. This further confirms revenue recognition hinges on physical progress, currently bottlenecked.

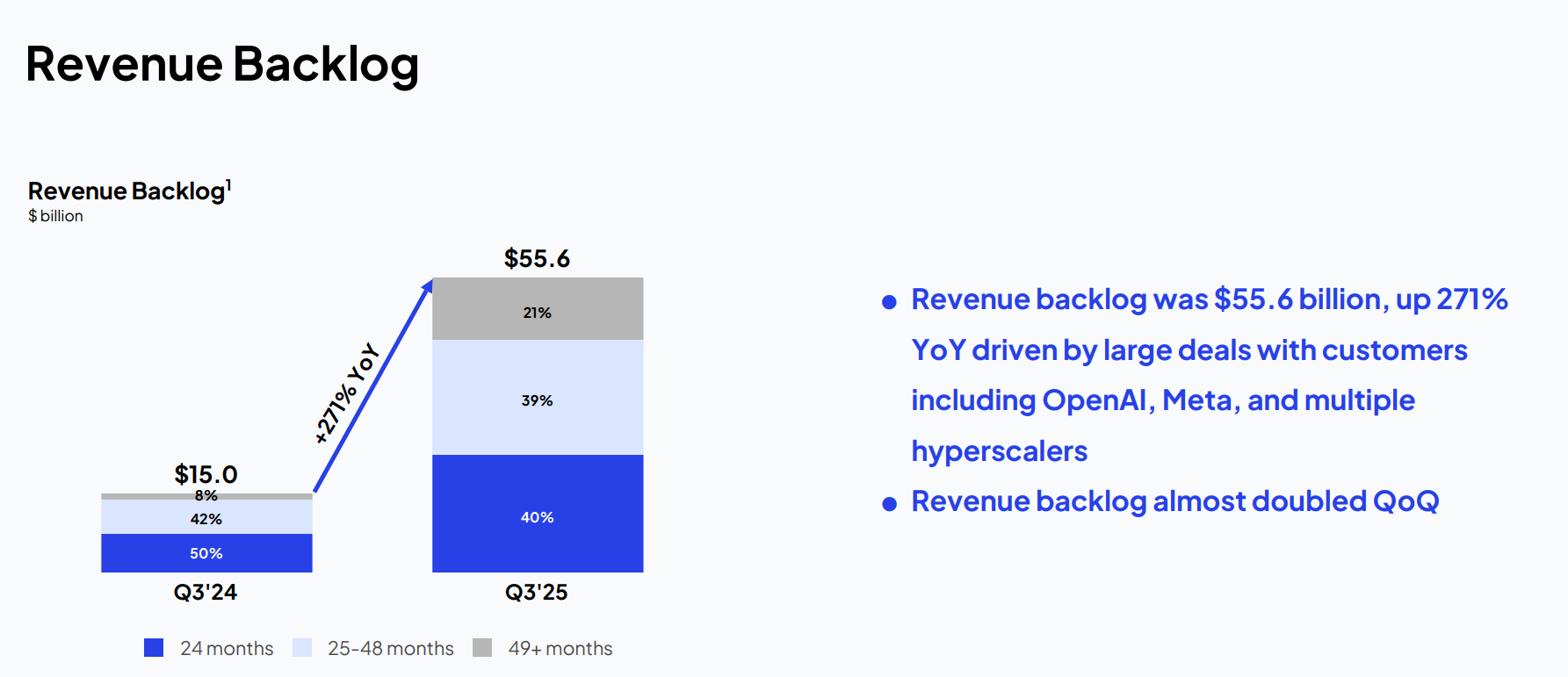

Order Backlog

Q3 revenue backlog surged from $30.1 billion at Q2-end to $55.6 billion, adding over $25 billion in a single quarter. These orders primarily come from AI industry leaders, serving as strong market validation while highlighting client concentration. For instance, the OpenAI partnership totals up to $22.4 billion, and a six-year Meta deal reaches $14.2 billion.

CoreWeave’s Potential Risks

Accounting Classifications and Structural Profitability Risks

In gross margin and cost breakdowns, the company excludes depreciation of key assets like servers and GPUs from cost of revenue, shifting it to the “technology and infrastructure” category, yielding a superficial 74% gross margin. This may be an accounting optimization that obscures true unit economics, making it hard for investors to gauge sustainable GPU leasing profitability.

Structurally, CoreWeave isn’t inherently more efficient or higher-priced than rivals like Oracle; extending GPU depreciation to 6 years eases short-term pressure but decouples from 1-2 year tech iteration cycles. If AI chip prices fall or model efficiencies reduce demand, accelerated future depreciation could compress margins or flip to losses.

Financial Risks from High Leverage

CoreWeave’s expansion relies heavily on leverage. It collaterizes GPU assets and high-value contracts to borrow from institutions. As of the latest quarter, total debt stood at $14 billion, with over 50% tied to GPUs. Should AI hype cool or tech iterations devalue assets, collateral revaluation could trigger margin calls. High interest and maturing debt could rapidly drain cash, sparking a liquidity crisis.

Customer Concentration Risk

CoreWeave’s success is deeply tied to NVIDIA’s dominance and AI fervor; its priority GPU access is essentially external dependency. If NVIDIA’s position weakens, the high-valuation, high-debt model becomes unsustainable. Moreover, current clients face GPU shortages, forcing reliance on CoreWeave for backup or peak needs. Once these giants perfect in-house supply chains, CoreWeave’s unique value proposition erodes.

Summary

In the short term, CoreWeave retains strong delivery momentum. Q3 revenue and backlog both exceeded expectations, demonstrating speed and execution advantages amid AI supply-demand mismatches. Contract extensions with hyperscalers enhance revenue visibility, reflecting deployment prowess and technical barriers for high-performance GPU clusters. With robust demand and competitors’ capacities not yet fully online, near-term growth certainty remains high—though this window of advantage is not eternally secure.

Over the long haul, investors should exercise caution. First, heavy reliance on a few core clients risks substantial revenue and profit hits if they self-build or switch providers. Second, total dependence on NVIDIA for supply leaves no control over pricing or availability, vulnerable in tight cycles. Third, the balance sheet is strained; high leverage and massive capex yield persistently negative free cash flow. Once the industry reaches supply-demand equilibrium or AI sentiment cools, the stock faces material downside. Thus, CoreWeave’s current investment appeal suits short-term trading plays rather than long-term value allocation.

Read more

* The content presented above, whether from a third party or not, is considered as general advice only. This article should not be construed as containing investment advice, investment recommendations, an offer of or solicitation for any transactions in financial instruments.