Nonfarm Payrolls Thoroughly Overturn Rate Cut Dreams. Spot Gold Falls Below $4,400 Mark, Hitting New Low Since Late March.

Tradingkey - On June 5, the U.S. Bureau of Labor Statistics released May non-farm payroll data that significantly exceeded market expectations, indicating that the U.S. labor market remains resilient.

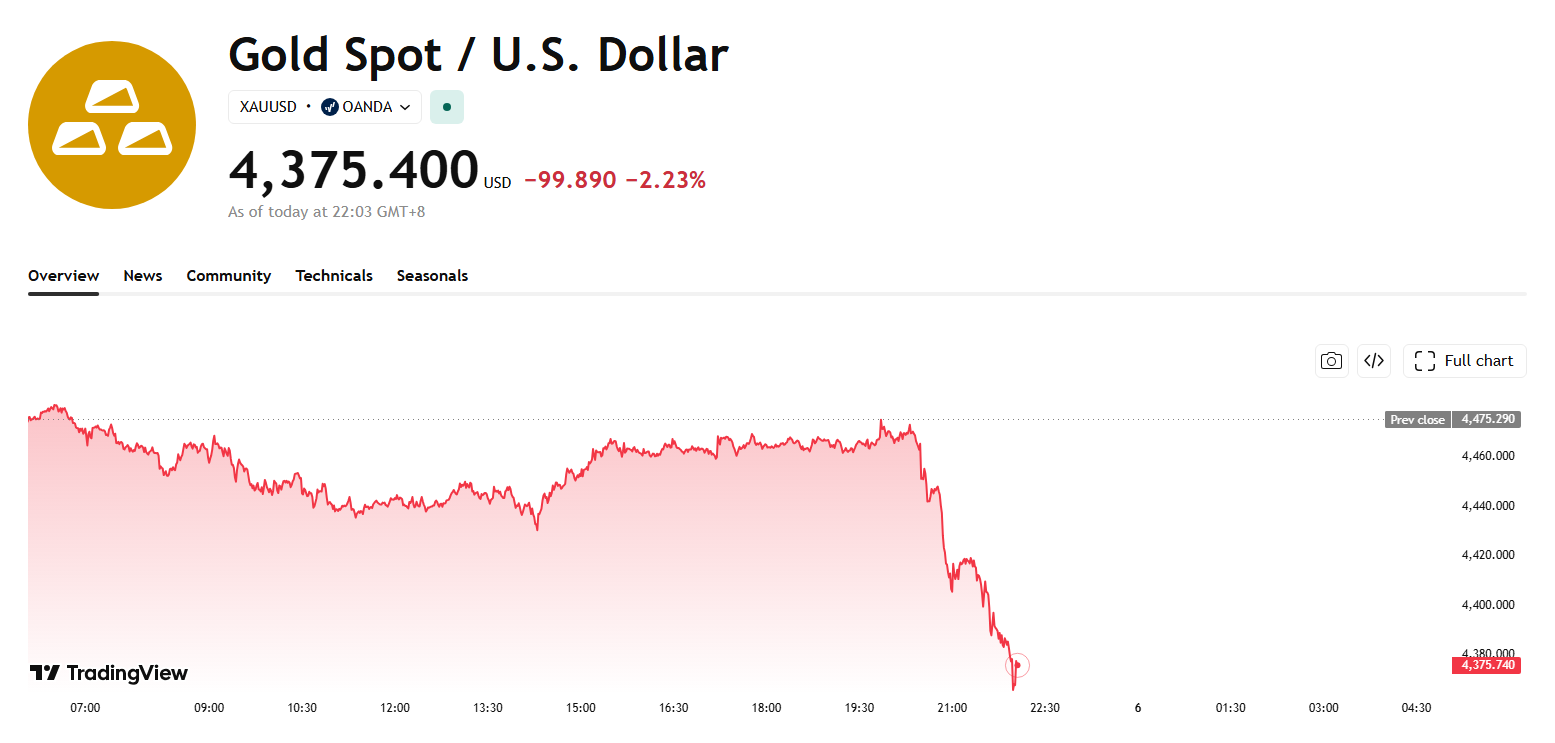

Impacted by this, spot gold ( XAUUSD) fell below the $4,400 mark. As of press time, it was down 2.23% at $4,375.4, its lowest price since March 27.

【Source: TradingView】

Data showed that May seasonally adjusted non-farm payrolls were recorded at 172,000, significantly higher than the market expectation of 85,000; the unemployment rate for May remained at 4.3% for the second consecutive month, in line with market expectations. Additionally, the combined job gains for March and April were revised upward by 93,000 from the original figures, making the past three months the strongest period for job growth in over two years.

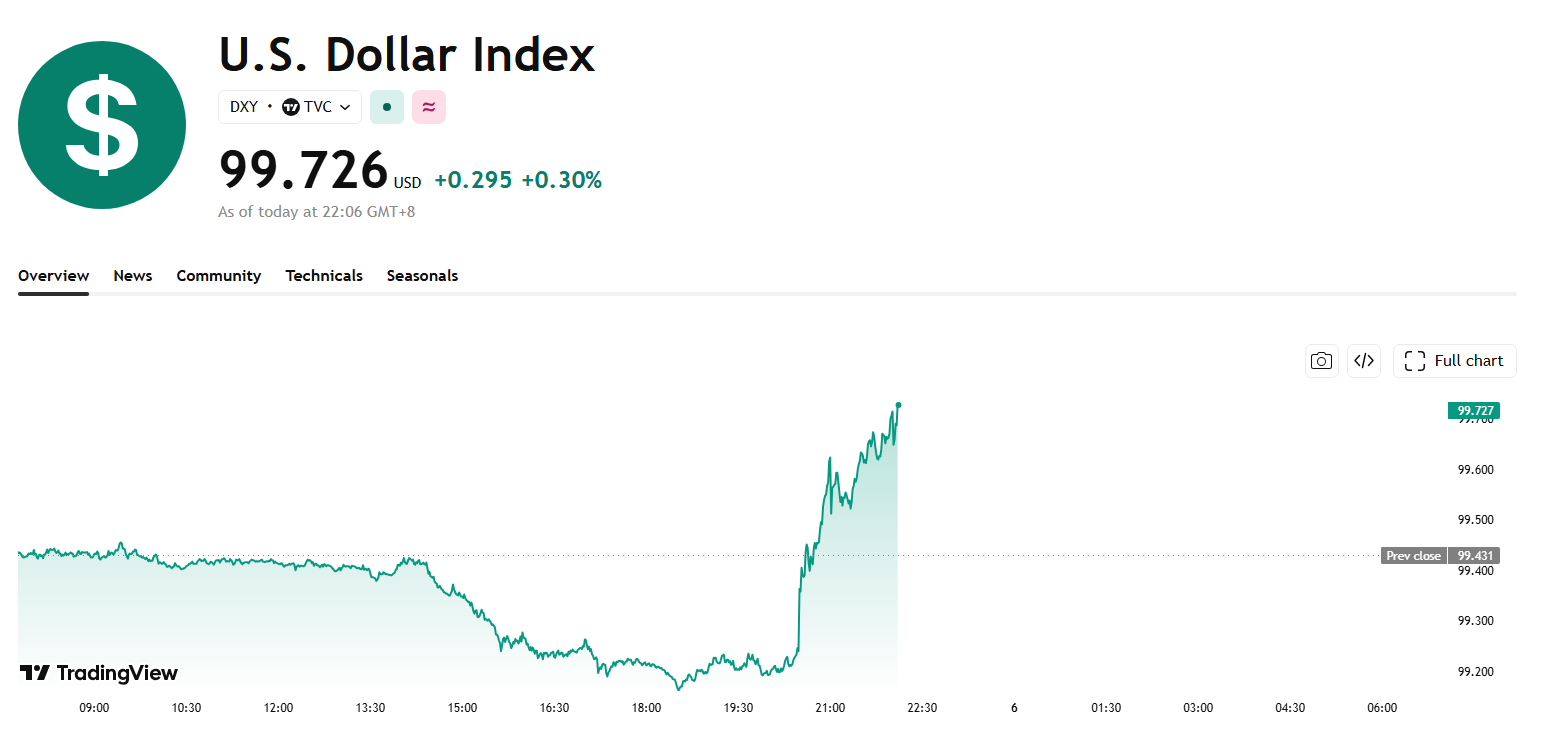

Following the release of the employment report, the U.S. Dollar Index rose sharply, trading at 99.726 as of press time, its highest level since April 9. Citi noted that the strong employment data further reinforced market expectations for Fed rate hikes, creating a favorable environment for the dollar to rise. The firm also stated that this data indicates the U.S. economy has staged an unexpected rebound despite inflation remaining above target levels.

【Source: TradingView】

In this scenario, investors' outlook on the Federal Reserve's future monetary policy has shifted significantly. The market is currently pricing in a Fed rate hike by next January, with the probability of a December hike rising to 63% from the previous 48%.

Institutional analyst Anstey stated that this non-farm report will undoubtedly dismantle any rationale for the Fed to cut interest rates in the coming months. If Warsh starts advocating for a rate cut at this month's policy meeting, he would appear out of step.

As U.S. economic data continues to demonstrate resilience, market expectations for the Fed to maintain tight policy have further intensified, leading to a simultaneous rise in the U.S. Dollar Index and Treasury yields, thereby weakening the appeal of gold as a non-yielding asset.

From a global asset allocation perspective, the gold market is currently navigating a tug-of-war between safe-haven demand and a high-interest-rate environment. On one hand, geopolitical risks and rising energy prices continue to support gold's long-term safe-haven value; on the other hand, the Fed's maintenance of tight policy has increased the opportunity cost of holding gold, exerting clear short-term pressure on prices.

However, the market is not entirely leaning bearish. Commerzbank stated that the market has shifted from rate-cut expectations before the outbreak of the war in the Middle East to fully pricing in the possibility of at least a 25-basis-point hike by the spring of 2027, thus lowering its year-end gold target from the original $5,000/oz to approximately $4,800/oz.

The institution further indicated that this target price implies there is still some upside potential for gold in the coming months because "our new baseline scenario expects a two-month transition period, followed by the reopening of the Strait of Hormuz and a retreat in Brent crude prices, which will reverse current market expectations for rate hikes."

Recommended Articles