Prediction: Tesla Stock Will Reach This Price in July (Hint: It's Going to Plummet)

Key Points

Tesla has already reported its vehicle delivery numbers for Q2, and they blew Wall Street's expectations out of the water.

That healthy beat on vehicle deliveries should lead to notable revenue acceleration, but its impact on profit margins remains unclear.

Tesla stock tends to exhibit extreme volatility in the weeks following its earnings reports.

- These 10 stocks could mint the next wave of millionaires ›

It's no secret that Tesla (NASDAQ: TSLA) is one of the most narrative-driven stocks in the market. The company's valuation hinges less on its revenue and profitability numbers, and more on whether investors believe it will successfully evolve into an artificial intelligence (AI) platform business with product lines spanning autonomous vehicles and humanoid robotics.

The bull case centers on Tesla scaling up its production of self-driving vehicles and proving that there is a market for its humanoid Optimus robots. These innovations aim to create entirely new revenue streams far larger than the electric vehicle (EV) and energy storage businesses that dominate its financials today.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

On the other hand, the bear case emphasizes that those same projects have experienced repeated delays and are incurring mounting capital expenditures with little in the way of near-term returns, while Tesla's core EV business has yet to demonstrate durable pricing power or margin expansion.

Tesla's second-quarter earnings report is slated for July 22, and growth investors may be wondering how the stock will react to that data readout, particularly given the polarized views about Elon Musk's ambitious vision for the company.

Image source: Getty Images.

Tesla crushed Q2 EV delivery estimates, but questions remain

Earlier this month, Tesla published its vehicle delivery figures for the second quarter. The company delivered 480,126 vehicles, comfortably ahead of the 406,024 consensus among sell-side analysts. All told, deliveries rose by 25% year over year and 34% sequentially. The company's energy storage deployments of 13.5 gigawatt-hours further underscored its momentum outside the EV business.

These figures were positive signals regarding Tesla's top-line automotive revenue. With nearly 74,000 more vehicles delivered than Wall Street expected, even conservative average selling prices should translate to a meaningful beat on automotive revenue.

However, the absence of pricing details means investors cannot yet fully judge whether accelerating revenue will translate into expanding gross margins. If a higher proportion of lower-priced vehicles were sold, or if leasing activity increased, that could have diminished the company's revenue upside.

How does Tesla stock usually react after an earnings report?

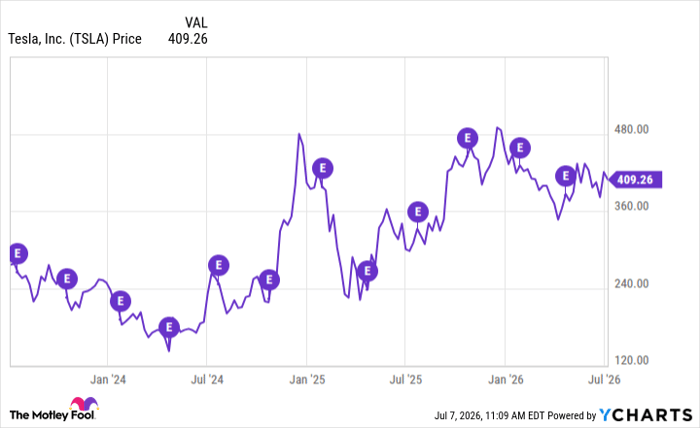

The chart below illustrates Tesla's stock price action over the last three years. Earnings releases are indicated by the purple circles with the letter "E" in the middle. The trends reveal a consistent pattern of sharp reactions from the market each time Tesla's quarterly results and guidance are digested.

TSLA data by YCharts.

Shorter-term movements immediately after the company reports have tended to be particularly pronounced. Several earnings reports across 2024 and 2025 were followed by gains of 15% to 25% over the next 30 days when Tesla's guidance was viewed favorably. At other times, particularly when the stock was already near a peak, the reports triggered pullbacks of 10% or more within the next month.

The chart makes it clear that Tesla stock rarely trades sideways after an earnings report. The market's ongoing shifts in sentiment around autonomous vehicles and AI robotics tend to amplify the impact of any surprise -- positive or negative -- in management's commentary.

Where will Tesla stock trade after the next earnings report?

Given that Q2's EV delivery beat is already public knowledge and the stock's tendency to make outsize moves, Tesla shares are likely to trade in a wide range in the days and weeks following the July 22 report.

I think a reasonable base-case forecast points to the stock fluctuating between roughly $365 and $455 over the next month. This means I think Tesla stock will decline by at least 10% by the end of July before any signs of recovery materialize.

Keep in mind that downside pressure could easily intensify if Tesla's operating expenses or capex guidance point to continued heavy investment in AI infrastructure without corresponding near-term revenue visibility. Conversely, any talk from Musk that touches on robotaxi deployments, Optimus production, or progress toward Full Self-Driving could trigger another of the familiar narrative-driven surges that have repeatedly lifted the stock by double-digit percentages.

History shows that even a single optimistic remark from Musk about autonomous driving or AI can temporarily override the impact of a mixed financial performance and send Tesla stock sharply higher. However, smart investors understand the opposite is equally true: Conservative commentary about product timelines or profit margins can lead to heavy sell-offs.

For these reasons, investors should prepare for elevated volatility rather than a single decisive directional move once Tesla's full picture emerges later this month.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $507,822!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $59,591!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $409,970!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

See the 3 stocks »

*Stock Advisor returns as of July 8, 2026.

Adam Spatacco has positions in Tesla. The Motley Fool has positions in and recommends Tesla. The Motley Fool has a disclosure policy.

Recommended Articles