SpaceX Reverses to Rally After Slumping 16%. Oppenheimer Sees 58% Upside for Company's Stock

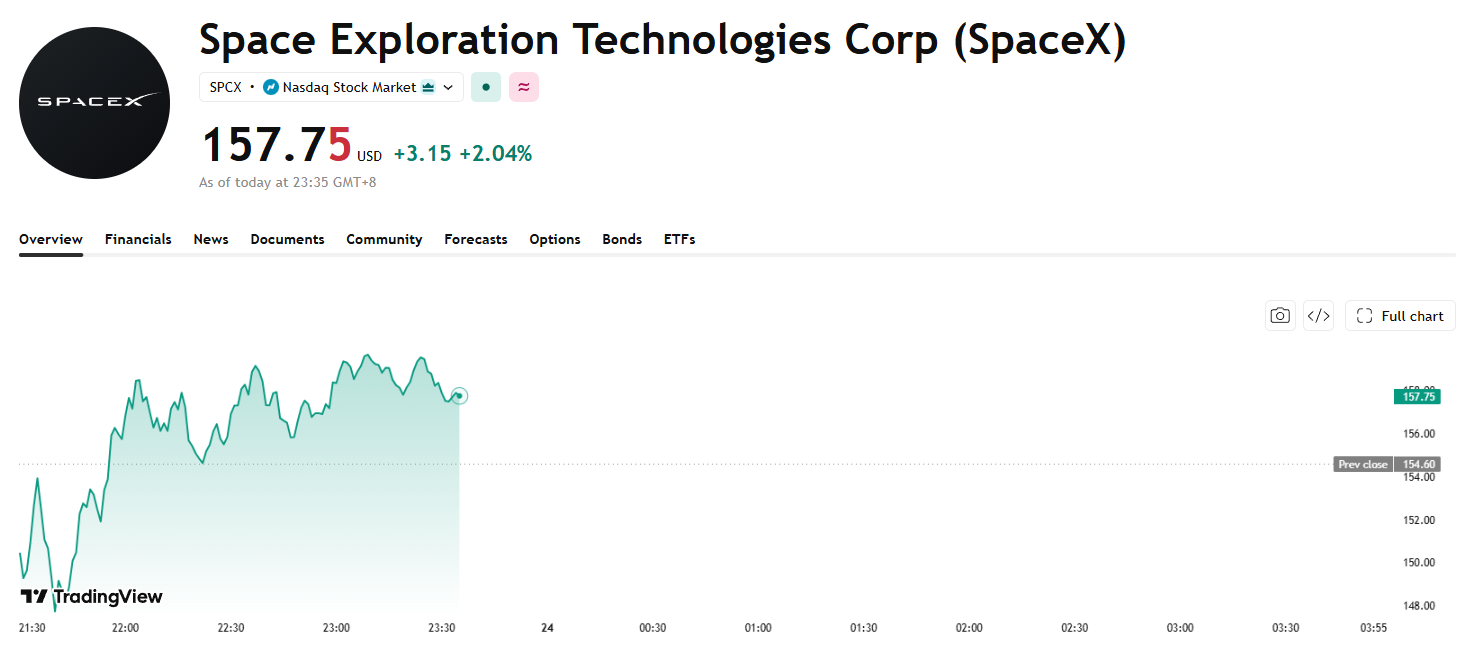

TradingKey - SpaceX (SPCX) plunged 16.43% in a single day yesterday following its bond issuance, and briefly dipped below its IPO price of $150 during pre-market trading today. However, amid a broad sell-off in tech stocks, SpaceX bucked the trend to rise over 3%, and as of writing, it remains up 2.04% at $157.75.

After experiencing a short-term plunge triggered by rumors of the bond issuance, SpaceX's stock price has staged a recovery, which in essence reflects the market's perception of this financing shifting from "liquidity panic" back to rational pricing.

[Source: TradingView]

The primary purpose of this $20 billion bond issuance is to refinance bridge loans maturing in 2027, which represents a routine capital structure optimization for high-credit corporations rather than a sign of cash flow stress. Combined with the company's post-IPO cash reserves of over $100 billion, the previous panic narrative of SpaceX being "extremely cash-strapped" has been progressively debunked, providing the underlying support for the stock price recovery.

It is worth noting that the shift in valuation logic brought about by the bond issuance has not disappeared. Prior to the listing, the market focused more on the long-term upside of the space and AI narrative, but the bond issuance has pulled investors' attention back from grand visions to operational realities, prompting a re-evaluation of how the pace of the company's massive capital expenditure aligns with its cash-generation capability.

Simply put, although Starlink is a mature cash-flow engine, the technological iterations of Starship, the global expansion of the satellite network, and the deep deployment of AI infrastructure are all in high-investment phases, leaving the path to long-term profitability still uncertain.

The sustainability of the subsequent stock price recovery depends on the following two factors.

First is the final pricing in the credit market. If the bond issuance spread remains manageable and subscription demand is robust, it would signal that the debt market recognizes the company's long-term solvency, which would simultaneously ease debt-related anxiety on the equity side.

Second is tangible progress on the business front. If the high-frequency reuse of Starship is achieved and Starlink's profit release accelerates, proving that its self-generated cash flow is sufficient to cover heavy capital expenditures, the debt will transition from a valuation drag back into a growth tool, driving the company's valuation back onto an upward trajectory.

Oppenheimer Asset Management raised its SpaceX price target from $190 to $250 in its latest research report, representing 58% upside from the current stock price.

The firm believes that with the enhanced revenue visibility brought by the acquisition of Cursor, SpaceX's AI business growth prospects have improved significantly, and the company may continue to leverage acquisitions in the future to build up key capabilities in large language models, data centers, power, and spectrum.

Recommended Articles