At Over $1 Trillion Market Cap, Is Micron Still Worth Buying?

HBM4 Continues To Drive Growth At 32% In Revenue

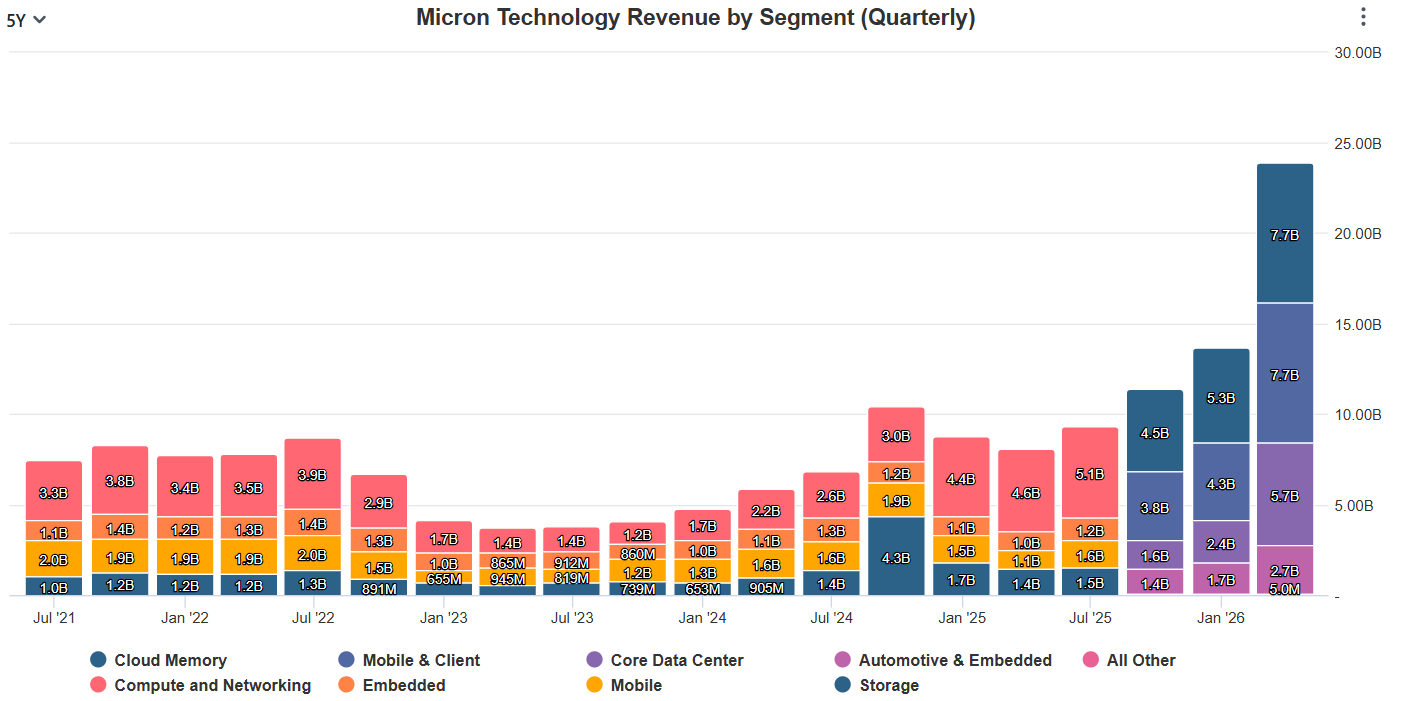

TradingKey - Micron Technology (NASDAQ: MU) market cap reached $1 trillion, followed by a price surge of 19%. Even more interesting, the stock price has gained by over 283.43% in the last 6 months, and this optimism intrigues my mind into finding out whether MU remains a bullish stock. From my analysis, HBM, which is a major revenue driver, faces an underserved advanced memory market which secures the demand up to 2027. Take, for example, the fiscal Q2’2026. In this release, the company’s cloud memory, where HBMs are classified, recorded an all-time high revenue of $7.75 billion, up from $5.28 billion in Q1’2026. If I also look forward, there is a high chance of sustaining this growth, pushing the price upwards, driven by management outlook. The management projects revenue of $33.5 billion in fiscal Q3’26, representing a possible 40.4% QoQ increase. Assuming the cloud memory segment maintains a 32% of the projected revenue as seen in this past quarter, it means MU’s cloud segment is likely to record a revenue of $10.72 billion in fiscal Q3’26, up from $7.7 billion in Q2’26. Based on my analysis, the image below shows the revenue trend in the last six months, delivered the 283.43% price gain. This is the period MU recorded impressive revenues. In my opinion, HBMs rapid market acceptance is currently in an early stage, and it positions the company for a real AI memory business. So, let me delve deeper to unravel why I believe MU warrants a “Buy” driven HBM chips.

Source: EEWORLD

Source: EEWORLD

Numbers Don’t Lie; $100 Billion TAM By 2028 Changes Everything

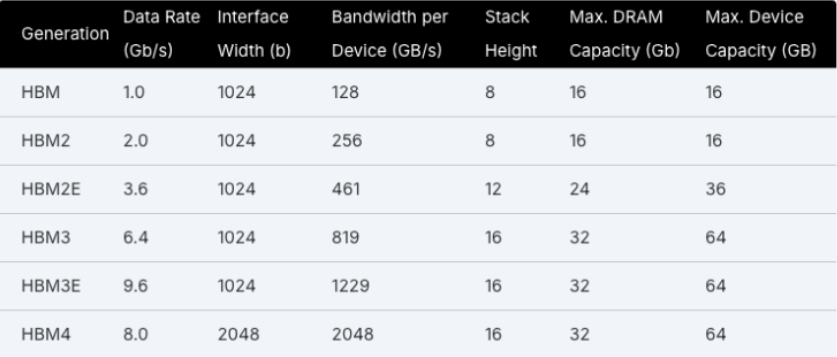

To bring out the number’s perspective much better, HBM product progress has been impressive. The first HBM had a data rate of 1.0 GB/s and a bandwidth per device of 128 GB/s. Now MU has HBM4 with a data rate of 8.0 Gb/s and a bandwidth of 2048 GB/s. This huge development comes with advanced and shortened data transmission paths that enable reduced power consumption. At this time, when the AI is at its inflection point, high-performance computing and data-intensive applications are needed. This is why you will see in my explanations below that MU’s HBMs have attracted a high demand.

Source: EEWORLD

Source: EEWORLD

In hindsight, MU’s approximation of the HBM Total Addressable Market (TAM) CAGR is around 40% from 2026 to 2028. This is primarily driven by this huge customer acceptance, which might bring in a revenue of around $100 billion in 2028 from $35 billion in 2025.

Here, you note that the latest MU’s HBM4 is already receiving huge market acceptance, given that all volume and price agreements for the 2026 HBM supply have already been completed. This includes the latest HBM4 in mass production, resulting in an outlook that shows the upside momentum is here to last. We are in the second quarter of the year 2026, and all MU’s HBM agreements involving supply have been completed, and this hints to me that the company has ample time to prepare for the rapidly growing AI market that needs these high-speed memory chips.

Recall, I previously mentioned that the current HBM4 has a maximum drum capacity of 32 GB. Looking ahead, MU has a new memory chip under development, HBM4E 16-high, and is expected to provide a maximum DRAM capacity of 48GB. Even before exhausting the market for the HBM4, the HBM4E is expected to ramp in 2027, which suggests that there is a possibility of a sustained upside momentum.

Volume HBM4 Shipments Also Prove Its Worth

Here, let’s take a scenario where a business is actively in research and development with no results to show. I believe this is not the type of business you would invest in if you are a risk- averse investor. This is not the case with MU because its HBM4 volume shipments kicked off in its first quarter of 2026 and are designed for NVIDIA Vera Rubin. For those who do not know, Vera Rubin is currently the most powerful AI platform globally, a chip that has greatly contributed to NVIDIA attaining a $5 trillion market cap. The most exciting fact is that this AI platform depends on Micron’s HBM4 memory, making MU an unavoidable beneficiary in NVIDIA’s market leadership. In fact, HBM4 is in production ramp to meet TAM, and this might result in catalyzing yield maturity faster compared to its previous HBM3E. In my view, this is not something to overlook, given the revenue volume it brings to the company, above 32%.

What Is Q2’2026 Earnings Growth Really Telling Us?

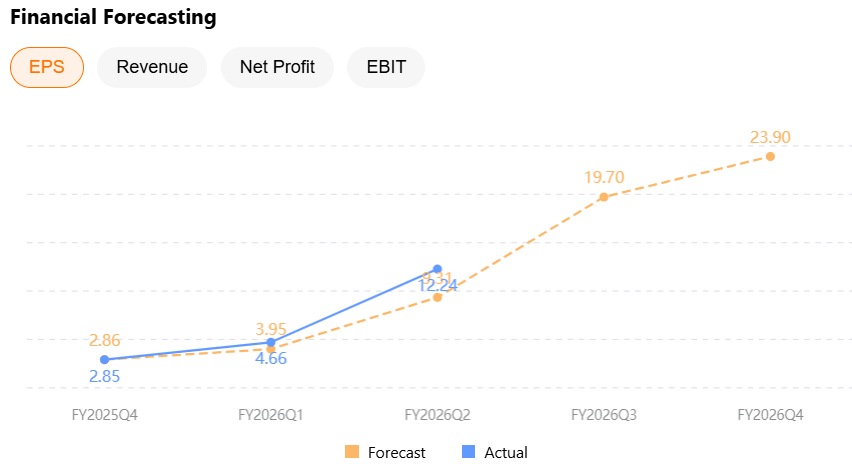

I previously highlighted Q2’26 revenues, and therefore, I believe that to this point, it is easier to relate Micro’s earnings improvement to the revenues. Q2’26 is a proof of this with EPS coming in at $12.24, beating analysts’ estimates from $9.31. Following my optimism above, driven by the HBM4, I believe the company has the capacity to beat the Q3’26 earnings estimate of $19.70.

Why Is It Worth Buying At $980

Looking at the historical record of consistent earnings beats, I will assume MU is likely to sustain this trend given the high demand for its HBMs. I will then apply the Price-to-Earnings (P/E) multiple to estimate the approximate upside potential by the end of 2026. Currently, the company’s P/E ratio trails at 46.5x, and to me, this is a fair market valuation consistent with the earnings growth. I am optimistic that MU is likely to maintain this consistency due to the demand for its HBM4, resulting in achieving an EPS of $23.90 in Q4’26. These two data points give a possible price target of $1,111.35 by Q4’26, which represents a potential price upside of 13.22%.

Detail | Value |

Trailing P/E ratio | 46.5x |

Esimated EPS by the end of (FY2026) | $23.90 |

Estimated price target (As of August 2026) | $1,111.35 |

Current Price (June 2026) | $981 |

Estimated Percentage Upside Potential | 13.3% |

2027 Upside Potential | |

Forward P/E | 10.0x |

Esimated forward EPS | $113.81 |

Possible price target (August 2027) | $1,138.1 |

Potential Percentage Price Target | 16.1% |

Even from a comparative perspective to its peers, Western Digital Corporation (NASDAQ: WDC) and Seagate Technology Holdings Plc (NASDAQ: STX), using the P/E multiple, it indicates that MU is undervalued. At the current MU’s P/E of 41.56x against the rallying STX P/E of 78.99x, and WDC at 30.30x. While STX leads in terms of P/E, its estimated Q1’27 forward earnings are estimated to reach $3.01, down from $5.01, while MU’s Q4’26 earnings are estimated to reach $23.90. It indicates that MU is fairly priced and that STX is currently overpriced. WDC’s P/E estimate of $3.68 in Q1’27, up from $3.28, reflects that together with MU, they are growth stocks, currently fairly priced.

Is Geopolitical Exposure the Hidden Threat?

Well, my answer is yes. While there is a conducive political environment currently, the management notes in the guidance above that it does not factor in possible trade or geopolitical developments that might affect the earnings estimates. For instance, in Q2’26, the impressive DRAM sales of $18.8 billion at 207% YoY growth may be achieved if global access remains uninterrupted to global AI customers, such as Chinese Hyperscalers, which face a ban.

While this is a risk, I do not think it is a major concern to worry about too much because Micron has diversified its geographical manufacturing from Idaho, New York, Singapore, Taiwan, India, to Japan. So far, Micron has five-year strategic customer Agreement (SCA) volume commitments with non-China AI customers. Even though China faces sudden restrictions, the contracted backlog already offers earnings growth potential.

Takeaway

I am reiterating my bullish stance on MU given that its HBMs remain solid in driving revenues and earnings. From the comparative P/E multiple analysis, MU is fairly priced at the current price, which is why I believe it warrants a bullish rating.

Recommended Articles