SpaceX to IPO in June, How Ordinary Investors Seize the Last Opportunity?

TradingKey - SpaceX has reportedly disclosed to its underwriting team a target valuation of $1.75 trillion to $2 trillion, with market consensus forming that it will break the historical record for global IPO proceeds. Furthermore, the prospectus is expected to be publicly unveiled in late May, with final pricing slated to be completed around June 15.

For average retail investors who lack the capacity to hold SpaceX equity directly in the primary market, how to strategically position themselves before the SpaceX IPO is a major point of market focus.

Google Holdings and Indirect ETF Exposure

For investors who cannot meet the accredited investor threshold through brokerage channels or do not wish to "chase highs" on IPO day, the secondary market offers an alternative.

Google ( GOOGL )'s equity investment in SpaceX provides a relatively suitable allocation window. According to regulatory filings submitted by the State of Alaska, Google held a 6.11% stake in SpaceX as of the end of 2025. Although several financial institutions estimate that Google's current holding has been diluted to approximately 5% following SpaceX's merger with xAI in February, the corresponding potential market value still exceeds $100 billion, making it a viable secondary choice for investing in SpaceX.

For retail investors, purchasing Google in the secondary market is equivalent to an indirect, low-cost play on SpaceX, as Google's current market valuation has not yet fully reflected SpaceX's potential $100 billion unrealized gain.

Furthermore, retail investors can still indirectly hold SpaceX by allocating to ETFs that hold positions in the company.

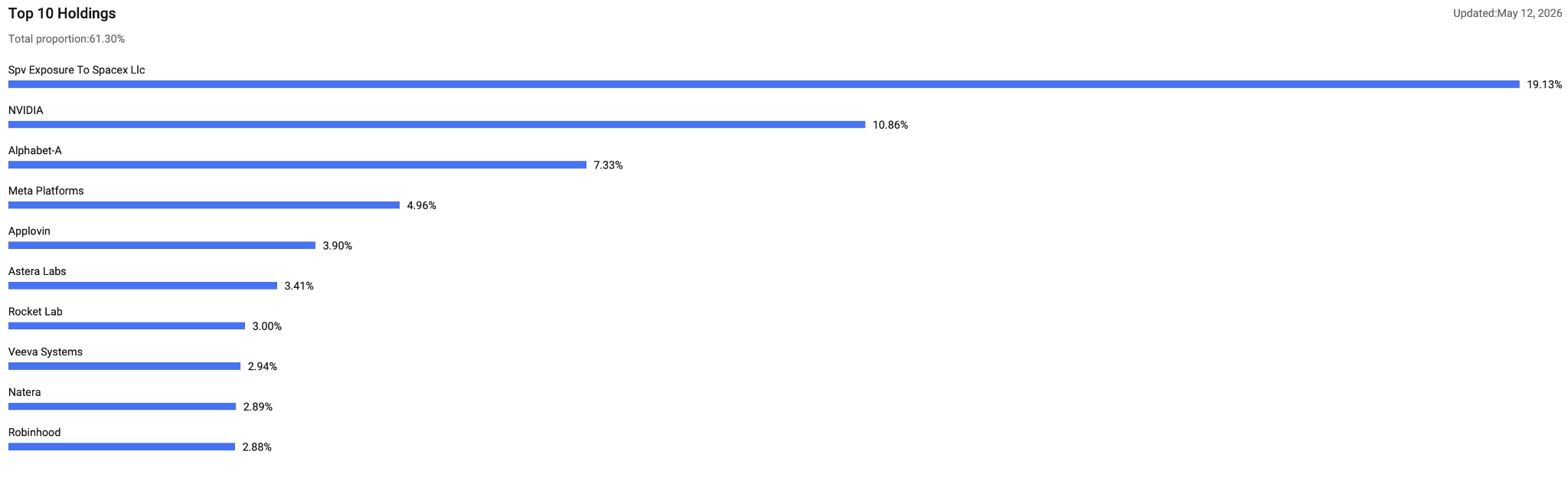

The ERShares Private-Public Crossover ETF (XOVR) has approximately 19.13% of its portfolio invested in SpaceX through a Special Purpose Vehicle (SPV) and does not impose an accredited investor threshold.

It should be noted that XOVR's SpaceX position is held indirectly through an SPV; the fund will not distribute SpaceX shares to holders upon its listing, and investors can only exit their positions by selling the ETF.

How to purchase ERShares XOVR?

XOVR is publicly traded on the Nasdaq exchange under the ticker symbol XOVR. Investors are not required to meet accredited investor thresholds and can purchase shares through any brokerage account with no minimum investment limit. The ETF has an expense ratio of 0.75%.

The ERShares Private-Public Crossover ETF (XOVR) is currently the most convenient vehicle for gaining indirect exposure to SpaceX through public markets. According to the latest data, 19.13% of the ETF's portfolio assets are invested in SpaceX through special purpose vehicles (SPVs), making SpaceX the fund's largest holding to date.

The remaining holdings are primarily technology and AI stocks, including Nvidia, Meta, and Alphabet. The ETF has nearly $500 million in assets under management.

XOVR operates by indirectly holding SpaceX through SPVs, as the fund does not hold SpaceX stock directly. For investors, this means that when purchasing XOVR, the weighting of the SpaceX position will passively increase as the liquidity of other holdings changes.

When investors sell ETF shares, the fund tends to prioritize selling liquid public stocks to meet redemptions, which passively increases the proportion of illiquid private assets like SpaceX in the portfolio. In extreme cases, this may cause a disconnect between the fund's trading price and its underlying net asset value, resulting in premiums or discounts.

How to purchase other funds and ETFs holding SpaceX?

In addition to XOVR, there are other publicly traded funds and ETFs in the market that provide indirect exposure to SpaceX.

Destiny Tech100 ETF ( DXYZ ): A closed-end fund listed on the New York Stock Exchange, specifically designed to provide public investors with access to high-growth, late-stage private technology companies.

As of the end of 2025, SpaceX accounted for 16.2% of its assets, making it one of the publicly traded closed-end funds with the largest exposure to SpaceX currently on the market. The fund has risen approximately 44% year-to-date, primarily driven by speculative fervor surrounding a potential SpaceX IPO.

Key Risks: The fund is currently trading at a premium of approximately 92% relative to its net asset value (NAV), meaning that for every $54.60 paid by investors, it corresponds to only about $19.97 in underlying assets. The high premium and a steep annual management fee of nearly 4.53% are primary risk factors, and the premium could contract rapidly once SpaceX completes its IPO.

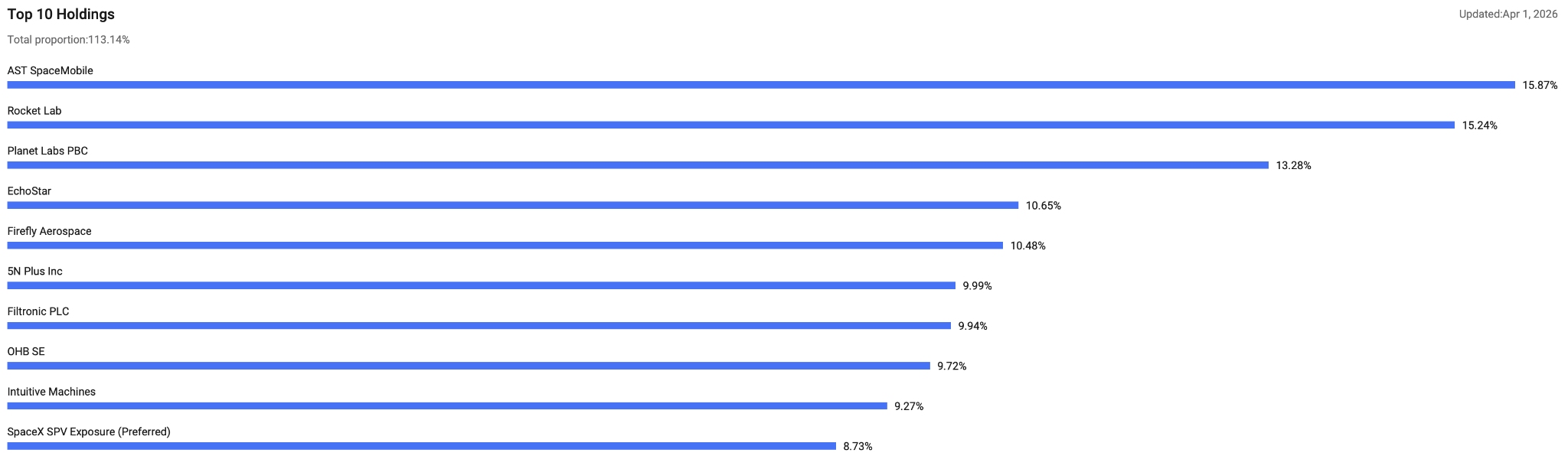

Tema Space Innovators ETF ( NASA ): A thematic ETF launched on March 30, 2026, trading on the NYSE, focusing on comprehensive investments in rockets, satellites, communications, and space infrastructure. SpaceX accounts for approximately 8.73% of its holdings, covering investment opportunities across the entire space industry value chain. NASA trades on the New York Stock Exchange and can be purchased through any brokerage account.

Key Risks: As a newly launched ETF, its assets under management are still accumulating, and attention should be paid to volatility risks.

High Risks Behind the Frenzy Premium

Investors should note that high returns are inevitably accompanied by high risks. Industry insiders have previously issued stark warnings regarding the $2 trillion valuation, stating that signals of a valuation bubble are evident.

According to institutional estimates, SpaceX's 2026 revenue is projected to be approximately $24 billion. A $2 trillion valuation implies a price-to-sales (P/S) ratio exceeding 80x, significantly higher than Saudi Aramco's IPO P/S ratio of roughly 6x. This multiple has already overextended expectations for perfect growth over the next decade.

Simultaneously, Nasdaq has pre-emptively adjusted its index inclusion rules. Effective May 1, 2026, mega-IPOs ranked in the top 40 by market cap will be eligible for fast-track inclusion into the Nasdaq 100 Index just 15 trading days after going public. SpaceX has also explicitly stated that securing early inclusion in the Nasdaq 100 is a mandatory condition for its choice of exchange.

Under these new rules, once SpaceX is included, a vast number of passive tracking funds will trigger massive mandatory buying, providing downside support for short-term valuations. However, this may also cause any quarterly results that merely meet expectations to be priced in ahead of time, leaving an extremely narrow margin for error.

Recommended Articles