[IN-DEPTH ANALYSIS] Australia: Under the Influence of Domestic and International Factors, AUD/USD Remains Bullish in the Short Term

Executive Summary

Following the AUD/USD exchange rate increase in April and May this year, we believe there remains upside potential for the currency pair in the short term (0-3 months). This outlook is supported by three key factors: First, Australia’s economic growth rebound, combined with a slower pace of interest rate cuts by the Reserve Bank of Australia, is expected to bolster the Australian dollar. Second, short-term improvements in tariff frictions are likely to support economic growth in the Asia-Pacific region, benefiting Australia’s commodity export sector and strengthening the AUD. Third, growing concerns over a sustained decline in the U.S. dollar index are prompting Australian institutional investors, particularly pension funds, to increase currency hedging, further supporting AUD appreciation. In the short term, we anticipate that Trump’s negotiations with multiple countries may ease global trade tensions. However, we believe high tariffs and erratic diplomatic strategies will remain hallmarks of Trump’s presidency, making lasting trade resolutions unlikely. In the medium term (3-12 months), escalating global trade conflicts are expected to weaken the U.S. economy, with ripple effects worldwide. During this period, the U.S. dollar is likely to appreciate as a safe-haven currency, leading to a probable peak and subsequent decline in AUD/USD.

Source: TradingKey

* Investors can directly or indirectly invest in the foreign exchange market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Recent AUD/USD Trends

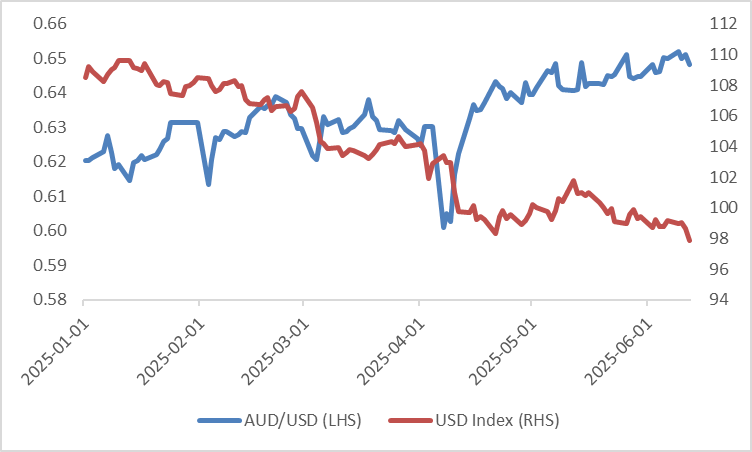

After bottoming out at 0.601 on 7 April this year, the AUD/USD exchange rate began to recover. The drivers behind the increase in April and May differed. In April, the sharp appreciation of AUD/USD was primarily driven by external factors rather than domestic ones. The introduction of additional tariffs, concerns over the Federal Reserve’s independence, and U.S. Treasury turmoil triggered a sell-off in the U.S. dollar, boosting the Australian dollar (Figure 1). Following April’s significant gains, May’s steady upward trend was supported by a combination of domestic and international factors. On 8 May, a U.S.-U.K. trade agreement and, on 12 May, easing U.S.-China trade tensions improved market risk appetite. These developments, coupled with robust Australian labour market data released on 15 May and unexpectedly strong inflation figures on 28 May, provided further support for the AUD.

Figure 1: AUD/USD and USD Index

Source: Refinitiv, TradingKey

2. Short-Term (0-3 Months) AUD/USD Outlook

Looking ahead, we believe AUD/USD has further upside potential in the short term (0-3 months). This view is supported by three key factors:

First, Australia’s economic growth recovery, combined with a slower pace of interest rate cuts by the Reserve Bank of Australia (RBA), is expected to drive AUD/USD higher. Strong employment growth has significantly boosted disposable income, fuelling a gradual recovery in domestic demand, including private consumption. Additionally, the economic rebound, alongside the start of the rate-cutting cycle, has led to signs of rising inflation, particularly in Core CPI. Looking forward, with stronger growth and elevated inflation, the RBA is likely to slow its pace of rate cuts, supporting the Australian dollar’s exchange rate.

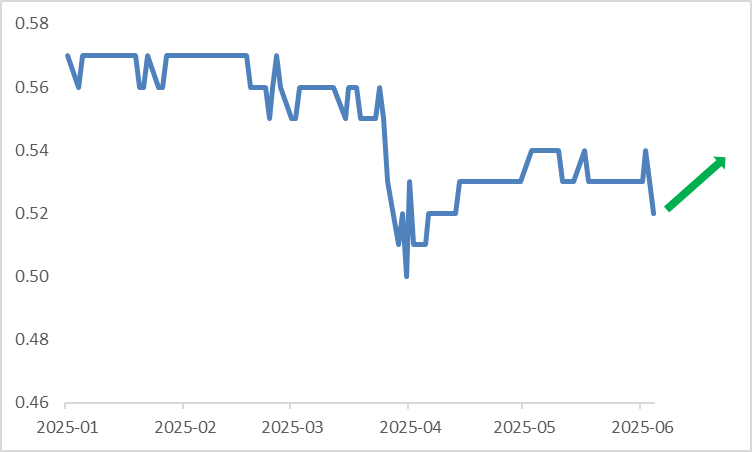

Second, easing U.S.-China trade tensions and the increasing likelihood of trade agreements between the U.S. and other Asian nations are expected to support economic growth in the Asia-Pacific region. As a commodity-exporting nation with Asia as its primary export market, Australia stands to benefit from regional economic stability, which is positive for the AUD exchange rate. On a global scale, if the U.S. secures trade agreements with more partners, global trade tensions may further subside. This could lead to a decline in the Swiss Franc (CHF), a traditional safe-haven currency that has previously benefited from U.S. policy uncertainty and related risk aversion. Consequently, in the short term, we are particularly bullish on AUD/CHF (Figure 2.1).

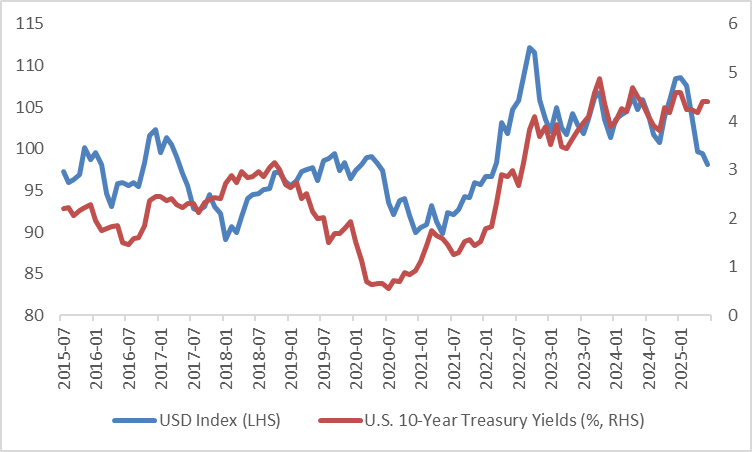

Third, Australian institutional investors, particularly pension funds, hold significant allocations in U.S. equities and bonds. For Australian fund managers with AUD as their base currency, a depreciating U.S. dollar reduces returns on U.S. investments. Consequently, currency hedging is critical for investors heavily exposed to USD-denominated assets. Given the long-term positive correlation between the U.S. dollar and U.S. Treasury yields (Figure 2.2), a weaker dollar tends to lower yields, increasing bond prices. In other words, U.S. Treasuries offer some inherent currency hedging benefits. In contrast, the correlation between the USD and U.S. equities is weaker, meaning a declining USD index significantly impacts the returns of AUD-based investors in U.S. stocks. As we anticipate continued USD weakness in the short term, more Australian investors are likely to adopt currency hedging strategies, further supporting AUD/USD appreciation.

Figure 2.1: AUD/CHF

Source: Refinitiv, TradingKey

Figure 2.2: USD Index and U.S. 10-Year Treasury Yields

Source: Refinitiv, TradingKey

3. Medium-Term (3-12 Months) AUD/USD Outlook

In the short term, we expect Trump to engage in negotiations with more countries, potentially easing global trade tensions. However, we believe high tariffs and erratic diplomatic strategies will remain defining features of Trump’s presidency, making sustained trade resolutions unlikely. In the medium term (3-12 months), escalating global trade conflicts are likely to weaken the U.S. economy, with ripple effects worldwide. During this period, the U.S. dollar is expected to appreciate as a safe-haven currency, leading to a probable peak and subsequent decline in AUD/USD.

* For further details supporting our foreign exchange market views, please refer to the macroeconomic section below.

4. Macroeconomics

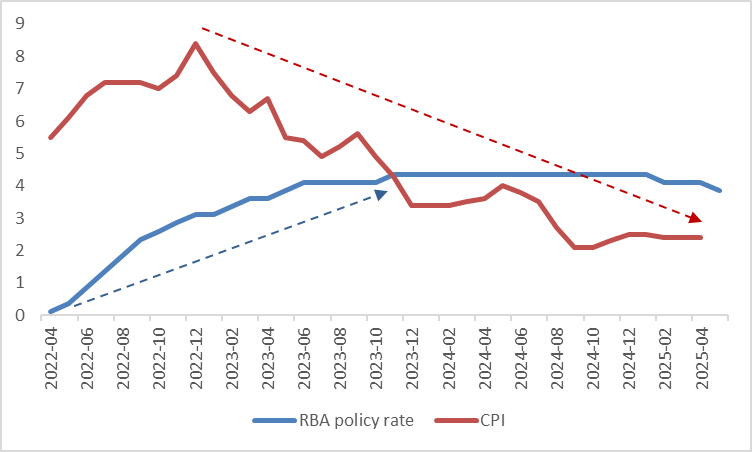

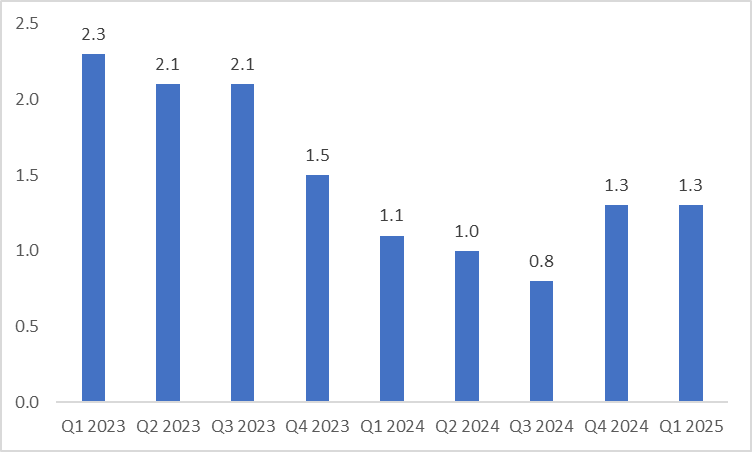

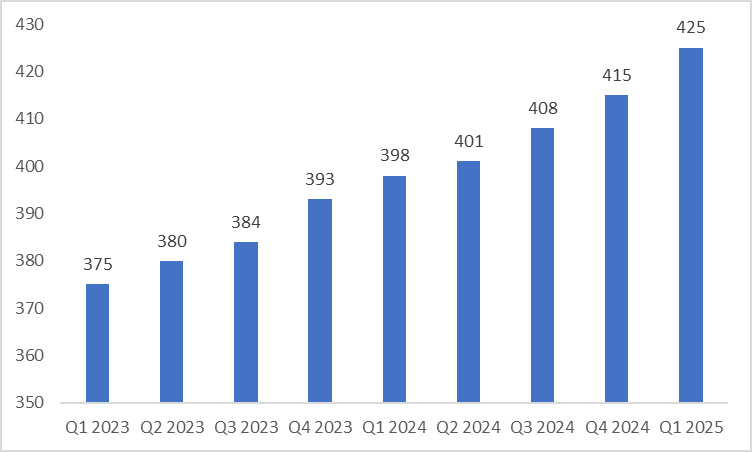

Between May 2022 and November 2023, the RBA successfully navigated its rate-hiking cycle, effectively curbing inflation while avoiding an economic crisis and maintaining low unemployment levels (Figure 4.1). Although Australia’s economic growth slowed significantly in the first three quarters of 2024, data since late last year indicates a recovery (Figure 4.2). This rebound is primarily driven by robust employment growth and declining inflation, which have boosted real disposable income (Figure 4.3), supporting a gradual revival in private consumption. Rising incomes are evident not only in increased spending but also in savings, with the household savings rate rising from 3.9% at the end of last year to 5.2%, closer to pre-pandemic levels. This higher savings rate lays a solid foundation for sustained consumption growth and economic stability in the medium to long term.

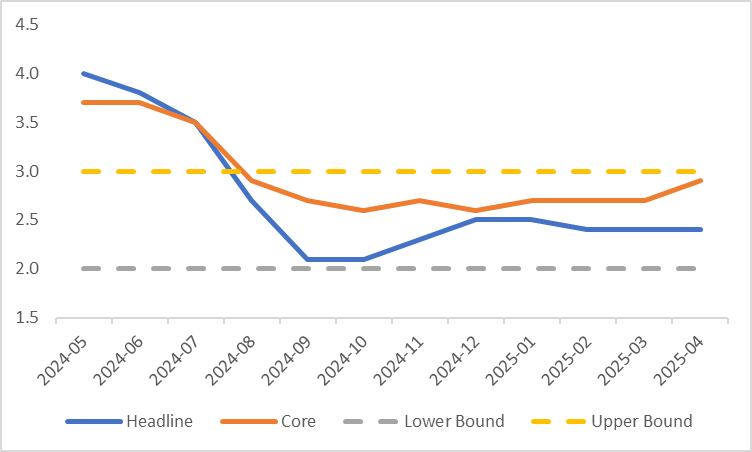

Over the past year, with the RBA maintaining its policy rate at a high of 4.35%, Australian inflation has steadily declined. However, since the start of this year, as the RBA initiated its rate-cutting cycle, the downward trend in CPI has stalled. Notably, Core CPI, which the RBA closely monitors, showed an upward trend in the latest April data (Figure 4.4). Looking ahead, with sustained economic recovery and rising domestic demand, the risk of reflation in Australia is expected to become increasingly pronounced. Despite the RBA’s dovish stance at its May meeting, we believe that, against the backdrop of rising inflation and economic recovery, the RBA will slow its pace of rate cuts, likely implementing only 1-2 additional cuts by the end of this year.

Figure 4.1: RBA Policy Rate and CPI (%)

Source: Refinitiv, TradingKey

Figure 4.2: Australia GDP (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 4.3: Australia Disposable Personal Income (AUD Billion)

Source: Refinitiv, TradingKey

Figure 4.4: Australia CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Recommended Articles