Indian Rupee grinds between firm US Dollar and lower oil prices

- The Indian Rupee struggles for direction amid the firm US Dollar and lower oil prices.

- BofA sees the Fed delivering three interest rate hikes this year.

- India's HSBC PMI expands at a moderate pace in June.

The Indian Rupee (INR) opens on a flat note against the US Dollar (USD) on Tuesday. The USD/INR pair holds on to Monday’s gains around 94.70 and is expected to remain in a limited range, as a firm US Dollar due to escalated hawkish Federal Reserve (Fed) bets has capped the upside, while lower oil prices amid progress in the United States (US)-Iran peace deal will limit the downside.

During press time, the US Dollar Index (DXY), which gauges the Greenback’s value against six major currencies, trades firmly near 101.00, the highest level seen in over a year.

US Dollar continues to outperform amid hawkish Fed bets

The US Dollar continues to outperform its currency peers, as market experts appear confident that the Federal Reserve (Fed) will deliver a number of interest rate hikes this year.

Analysts at Bank of America (BofA) expect the Fed to deliver three interest rate hikes of 25 basis points (bps) in September, October, and December meetings, a sharp turnaround from the anticipation that the central bank will stand pat this year.

“The data simply don't warrant cuts this year. Core inflation is too high, and moving up. The solid April jobs report was the last straw, especially given hawkish Fedspeak," BofA said.

In the monetary policy announcement last week, the Fed left interest rates unchanged in the range of 3.50%-3.75%, as expected; however, the dot plot, which reflects where policymakers collectively see the Federal Funds Rate heading in the short-to-long term, showed that interest rates could reach 3.8% by the year-end.

Oil prices remain lower as US touts further progress in talks with Iran

In the opening trade on Tuesday, the MCX Crude Oil contract expiring on July 20 is 0.4% higher to near 7,010, but is close to its over three-month low of 6,897 posted last week. Oil prices have remained lower amid progress in technical talks between the US and Iran.

Earlier in the day, US Vice President (VP) JD Vance expressed progress in technical talks with Tehran. “Yes, there was a little bit of threatening, there was a little bit of whining, but at the end of the day, the talks continued, and we made great progress,” Vance said, CNBC reported.

On Monday, US VP Vance said that Tehran had agreed to permit International Atomic Energy Agency (IAEA) inspectors back into Iran, calling it a “major milestone for the American people and the first step in permanently denuclearizing or permanently ending a nuclear weapons program in Iran.”

Lower oil prices bode well for currencies from economies, such as India, which rely heavily on oil imports to meet their energy needs.

India's flash HSBC PMI rises but at a moderate pace

India's preliminary HSBC Purchasing Managers' Index (PMI) expands again in June; however, the pace of growth has moderated in both manufacturing and services sector activity. The Composite PMI has arrived at 57.4, lower than 59.3 in May.

"Private sector activity eased a bit in June. Growth of manufacturing output softened a tad as inventory-building lost steam after a few hectic months. New export orders remained resilient and the order-to-inventory ratio ticked up, pointing at resilient manufacturing activity down the line. Input costs across the private sector rose, but at the slowest pace in five months," Pranjul Bhandari, Chief India Economist at HSBC, said.

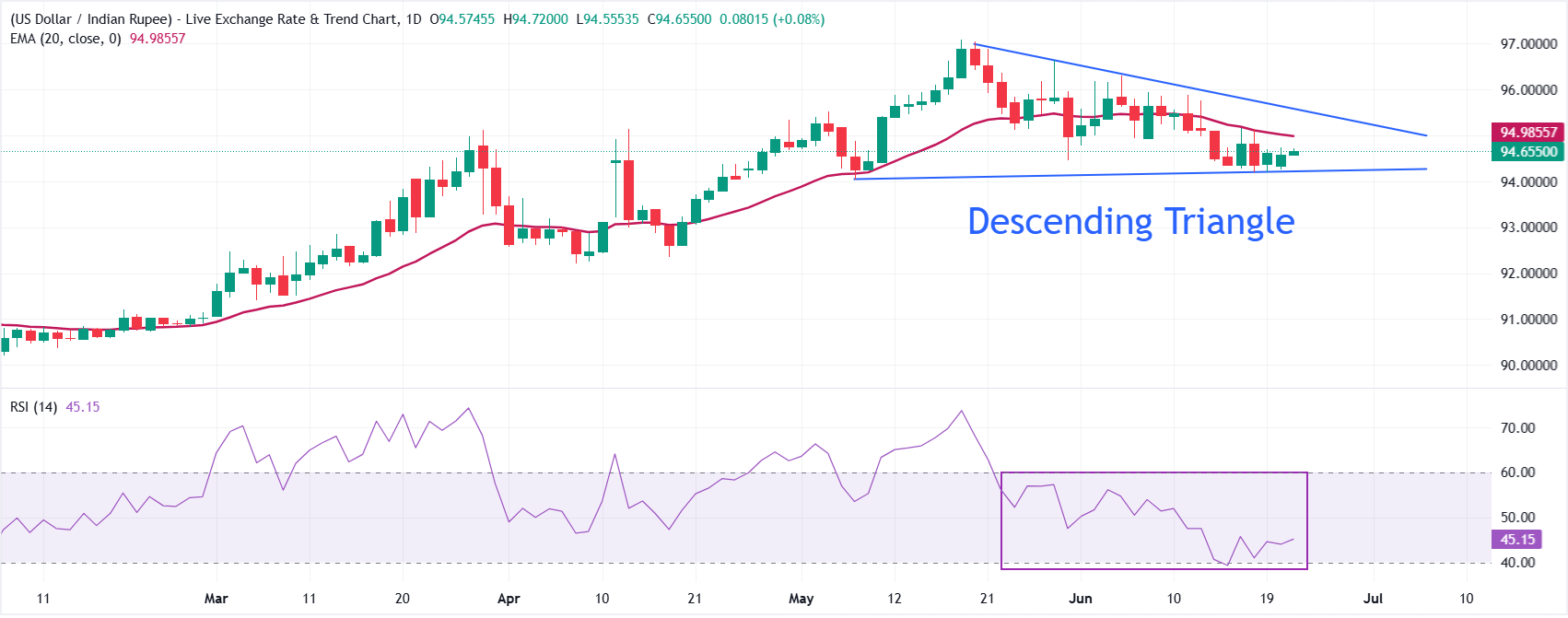

Technical Analysis: USD/INR trades inside Descending Triangle formation

USD/INR trades almost flat at around 94.65, holding a bearish near-term bias as price sits below the 20-period Exponential Moving Average (EMA) at 94.9856 and under a broader downward resistance trend line that comes in near 95.57. The loss of traction below these caps suggests rallies are likely to be faded, while the Relative Strength Index (14) hovering just under the 50 mark hints at waning upward momentum rather than outright oversold conditions.

On the topside, initial resistance is located at the 20-period EMA around 94.99, with a stronger barrier at the descending trend line near 95.57, which would need to be cleared to ease the current downside pressure. On the downside, immediate focus stays on the rising support trend line near 94.22, acting as the next key floor; a decisive break beneath this latter level would open the door to a deeper retracement within the broader uptrend structure.

(The technical analysis of this story was written with the help of an AI tool.)

Indian Rupee FAQs

The Indian Rupee (INR) is one of the most sensitive currencies to external factors. The price of Crude Oil (the country is highly dependent on imported Oil), the value of the US Dollar – most trade is conducted in USD – and the level of foreign investment, are all influential. Direct intervention by the Reserve Bank of India (RBI) in FX markets to keep the exchange rate stable, as well as the level of interest rates set by the RBI, are further major influencing factors on the Rupee.

The Reserve Bank of India (RBI) actively intervenes in forex markets to maintain a stable exchange rate, to help facilitate trade. In addition, the RBI tries to maintain the inflation rate at its 4% target by adjusting interest rates. Higher interest rates usually strengthen the Rupee. This is due to the role of the ‘carry trade’ in which investors borrow in countries with lower interest rates so as to place their money in countries’ offering relatively higher interest rates and profit from the difference.

Macroeconomic factors that influence the value of the Rupee include inflation, interest rates, the economic growth rate (GDP), the balance of trade, and inflows from foreign investment. A higher growth rate can lead to more overseas investment, pushing up demand for the Rupee. A less negative balance of trade will eventually lead to a stronger Rupee. Higher interest rates, especially real rates (interest rates less inflation) are also positive for the Rupee. A risk-on environment can lead to greater inflows of Foreign Direct and Indirect Investment (FDI and FII), which also benefit the Rupee.

Higher inflation, particularly, if it is comparatively higher than India’s peers, is generally negative for the currency as it reflects devaluation through oversupply. Inflation also increases the cost of exports, leading to more Rupees being sold to purchase foreign imports, which is Rupee-negative. At the same time, higher inflation usually leads to the Reserve Bank of India (RBI) raising interest rates and this can be positive for the Rupee, due to increased demand from international investors. The opposite effect is true of lower inflation.

Recommended Articles