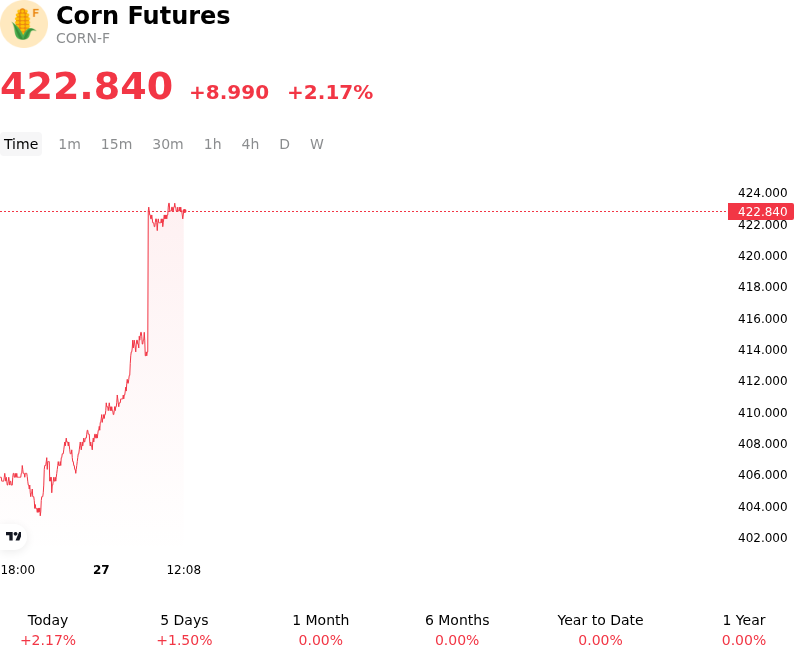

Corn Futures (CORN-F) Is up 2.17% on Jun 26: Why It Happened

Corn Futures (CORN-F) is up 2.17% at Jun 26 00:10(ET), now at $422.84, with a 7-day up of 1.50%.

What is driving Corn Futures (CORN-F)’s stock price up today?

The recent advance in corn futures is primarily driven by a dramatic shift in weather expectations and a structural repricing of supply ahead of key government reports. In the US Midwest, crop concerns are mounting as meteorological models project a major, high-pressure ridge to bring a prolonged stretch of hot and dry weather across the central Corn Belt starting over the weekend. This impending heatwave follows a mid-June period marked by severe storms, tornadoes, and excessive rainfall that left fields waterlogged and plants vulnerable to root disease. This rapid transition from excessive moisture to intense heat is stoking fears of yield degradation during critical vegetative growth stages. Simultaneously, a severe European heatwave and drought, particularly in France, have raised concerns that continental production could fall to multi-decade lows, boosting global import demand.

Supply-side anxieties are further amplified by positioning ahead of the upcoming USDA Acreage Report. Private crop surveys suggest that the actual planted area for US corn may fall significantly below the initial intentions reported in March. Rising input and fertilizer costs, coupled with late-spring planting disruptions, have incentivized a shift toward soybean cultivation. Analysts predict that these factors could remove substantial volume from the projected domestic supply, shifting the market balance from a comfortably supplied outlook to a much tighter scenario if yields are compromised.

This tightening supply narrative triggered a sharp technical reversal in the futures market. Having recently touched multi-month lows, the price action initiated a key reversal session, prompting heavy short-covering. Institutional speculative accounts and commodity funds, which had amassed sizeable net-short positions in grain markets, rushed to cover their exposure before the fast-approaching month-end and quarter-end deadlines.

Support is also stemming from robust demand signals and positive macroeconomic spillovers. Weekly export data continues to reflect strong international appetite, led by steady buying from Mexico and Japan, alongside market chatter that Chinese buyers are actively inquiring for late-summer shipments of US grains. On the macroeconomic front, a recovery in the energy complex has provided a constructive backdrop. As crude oil and gasoline futures rebounded from recent lows, they bolstered the pricing environment for ethanol, for which corn is the primary feedstock. This stabilization in energy-linked demand, combined with near-term weather risks, has successfully re-established a production risk premium in the market.

More details about Corn Futures (CORN-F)

Recent Events and Risks:

- Favorable Crop Progress and High Soil Moisture: The USDA's Crop Progress report showed 68% of the U.S. corn crop rated in "good-to-excellent" condition, with crop development outpacing historical averages as silking reached 5% (above the 3% five-year average). This steady development and favorable Midwest moisture levels have minimized weather risk premiums, exerting downward pressure on Chicago Board of Trade (CBOT) futures.

- Crude Oil and Biofuel Price Deterioration: Easing Middle East tensions and diplomatic progress between the U.S. and Iran have triggered a sharp decline in crude oil and gasoline prices, forcing RBOB gasoline and wholesale Chicago ethanol swap prices lower. Because corn is the primary feedstock for U.S. ethanol production, this decline in biofuel margins directly impacts domestic corn demand, dragging CBOT corn down near multi-month lows.

- Upward Revisions to European Crop Yields: In its June report, the European Union's crop monitoring agency (MARS) raised its projected 2026 EU-27 corn yield forecast to 7.38 tonnes per hectare from 7.30 tonnes per hectare. This upward revision highlights expectations of larger global grain supplies, compounding the bearish outlook in international markets.

- Strong U.S. Dollar and Technical Liquidations Ahead of USDA Reports: The U.S. dollar index hovering near a 13-month high has eroded the export competitiveness of U.S. grains on the global stage. Furthermore, commodity funds have engaged in speculative selling and technical position liquidations as traders brace for the highly anticipated USDA Quarterly Grain Stocks and Planted Acreage reports on June 30.

Recommended Articles