Firm data isn't hot enough for the US Dollar

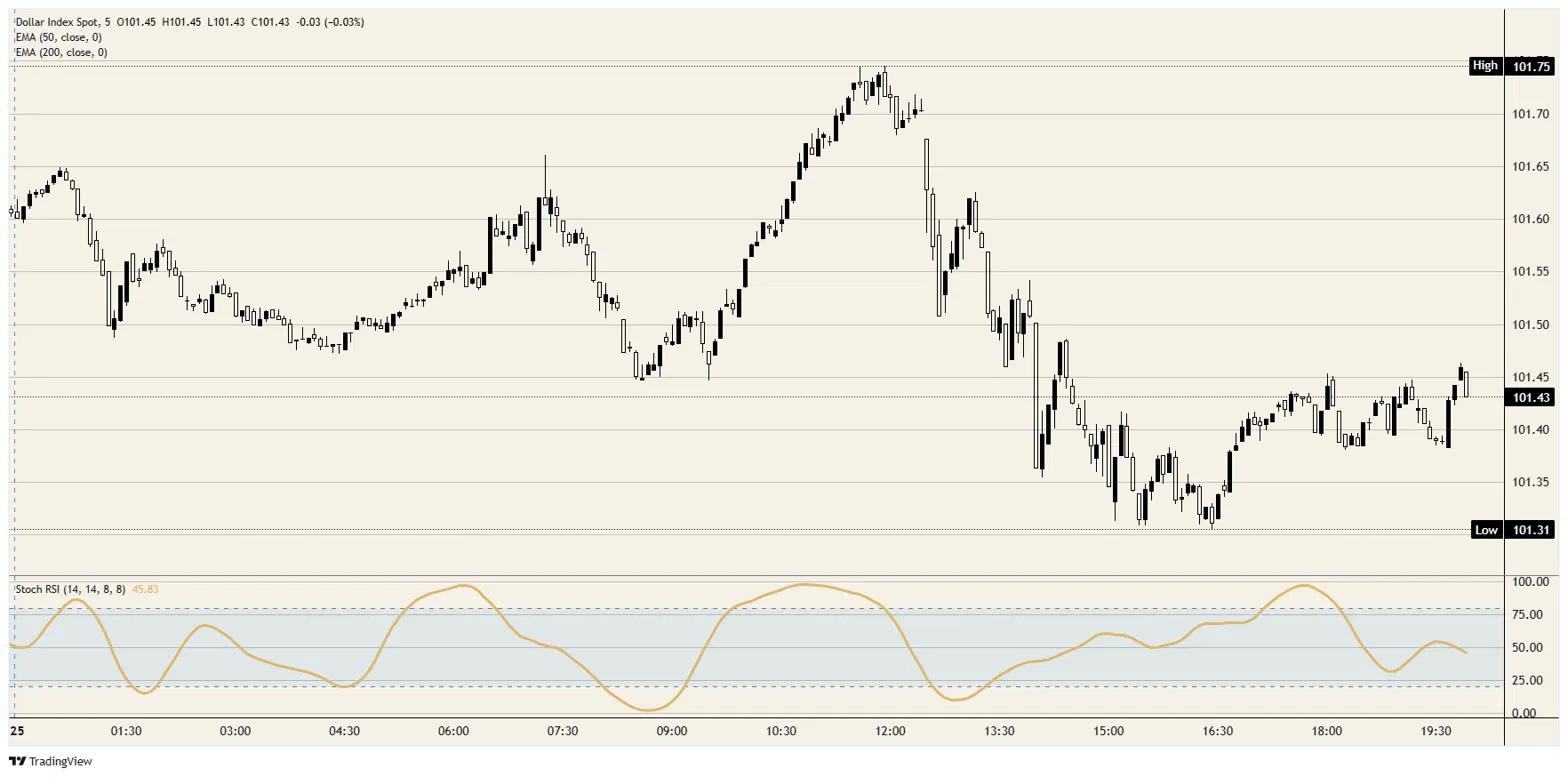

- DXY eased on the day, stalling just below the highs after a powerful multi-month climb.

- US growth, spending and jobless claims all came in firm on Thursday.

- Yet core PCE landed only in line, trimming Fed hike bets and leaving the Dollar without fresh fuel.

The US Dollar Index (DXY) had every excuse to extend on Thursday and declined instead. A firm batch of US data crossed the wires, yet the Dollar eased off the top of its multi-month rally, slipping back toward 101.45 after probing close to 101.75 earlier in the session. The numbers were supposedly tailor-made for Dollar bulls; the tape's refusal to extend on them is the more interesting signal.

Good numbers, just not the right kind

On paper, the releases ticked the boxes a Dollar bull would want. First-quarter Gross Domestic Product (GDP) was revised up to 2.1% annualized, comfortably above the 1.6% consensus, while personal spending and personal income both rose 0.7% and beat. Core capital goods orders jumped 1.6%, and weekly jobless claims fell to 215K, undershooting the 225K estimate. By almost any measure the US economy is still running warm.

The catch sat in the inflation data. Core Personal Consumption Expenditures (PCE), the inflation gauge the Federal Reserve (Fed) watches most closely, printed in line at 0.3% MoM and 3.4% YoY, sticky but no hotter than feared. Markets had been bracing for an upside surprise that would force the Fed's hand harder; an in-line read removed that tail, and traders quietly trimmed the odds of a September hike.

Already priced for hawkish

None of this changes the bigger picture, which is a Fed still leaning hard against inflation. Last week's hold left the policy rate at 3.75% alongside a hawkish set of projections, and the market continues to price at least one more hike before year-end. That stance has powered the Dollar's run and pushed DXY to the top of its range.

The problem for bulls is that a fully-priced story needs fresh, hotter input to keep advancing, and Thursday delivered firm rather than scorching. Crude Oil has also slid back toward pre-conflict levels as the US-Iran peace framework holds, easing the inflation impulse at the margin, so the Dollar simply ran out of reasons to push higher on the day.

Stretched but still pointing up

Structurally, the uptrend on the chart is still firmly intact. DXY sits well above its 50-period and 200-period Exponential Moving Averages (EMA), both clustered in the high-99s, and the daily Stochastic Relative Strength Index (Stoch RSI) near 70 shows momentum elevated but not yet exhausted. Thursday's dip held above the prior session's base around 101.30.

What the chart cannot disguise is fatigue at the highs. An index that fades on a firm data dump is telling you the easy money up here has been made, even if it has not yet handed the trend back to sellers. For now this reads as a pause inside a bull move, not a reversal.

Levels to watch

Resistance: The 101.75 to 101.80 zone caps the range and marks the line bulls must reclaim and hold; a clean break opens room toward 102.00 and beyond.

Support: Initial support sits near 101.30, the prior session's floor, with the round 101.00 handle below it. A deeper unwind would put the high-99s, where the moving averages sit, back in play.

Bias: Higher, but selectively. The trend still favours the Dollar and at least one hike remains priced, so dips toward 101.00 are a better bet than chasing the highs. Friday's University of Michigan (UoM) sentiment survey and inflation expectations are the next, lower-tier catalyst, and a soft inflation-expectations print would chip further at the hike narrative.

Dollar Index 5-minute chart

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Recommended Articles