2 Reasons to Buy Netflix Stock on the Dip

Key Points

Netflix can still expand into other lucrative areas of the streaming industry.

The company's shares are trading at (very) reasonable levels.

- 10 stocks we like better than Netflix ›

Netflix (NASDAQ: NFLX) can't catch a break. The streaming leader was already having a tough year, but its second-quarter update, which it released on July 16, sent its share price even lower. The stock is now down 24% this year and 42% over the past 12 months. Netflix's second-quarter results were not terrible, not by a long shot. The company's revenue increased by 13.4% year over year to $12.6 billion, while its earnings per share climbed 11% to $0.80.

However, Netflix's third-quarter guidance of $12.9 billion, which would represent a 11.7% year-over-year increase, fell short of Wall Street's projections. That said, even with the headwinds it is facing, Netflix looks like an attractive stock to buy on the dip. Let's consider two reasons why.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Image source: Getty Images.

1. Potential growth opportunities

Netflix remains one of the top players in the streaming market. However, the company has not yet established itself in several industry niches, including sports streaming. In its second-quarter letter to shareholders, Netflix noted a negative impact on its business during the first half of the year due to the Winter Olympics and the FIFA World Cup, which it does not own the rights to. Many investors see this as a bearish sign. I disagree. The fact that these events are harming Netflix's business highlights that, provided the company can make significant headway in sports streaming, it could meaningfully grow engagement and paid subscriptions. And the company has already started making progress toward that goal.

In recent years, Netflix has livestreamed football games and boxing fights. That may just have been the beginning. The company is reportedly planning to bid for the rights to the 2030 and 2034 FIFA World Cups. It likely will seek out other opportunities as well, and given that it has a much stronger brand name than most streaming specialists, it could be just as successful as them -- if not more so -- once it establishes a strong library of content in this space. And that's just one of many opportunities it could pursue.

2. The price is right

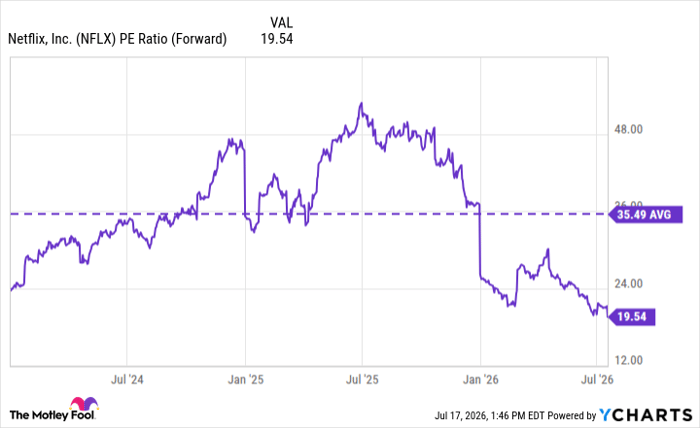

Given Netflix's post-earnings dip, the company is now trading at attractive levels. The stock is cheaper than it has been over the past two years, at least going by its forward price-to-earnings (P/E) ratio.

NFLX PE Ratio (Forward) data by YCharts

The average forward P/E for information technology stocks is 21.6. Some may argue that Netflix is cheap because growth is slowing down and its prospects aren't as attractive as they once were. But every time the streaming giant has found itself in a similar situation, it has turned things around. My view is that Netflix will do the same thing this time, given the large, untapped opportunity in streaming and advertising.

Should you buy stock in Netflix right now?

Before you buy stock in Netflix, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Netflix wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $371,842!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,244,783!*

Now, it’s worth noting Stock Advisor’s total average return is 900% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 19, 2026.

Prosper Junior Bakiny has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Netflix. The Motley Fool has a disclosure policy.

Recommended Articles