PepsiCo Stock Rebounds From 52-Week Lows; Can Q2 Earnings Fuel a Bigger Rally?

TradingKey - PepsiCo (NASDAQ: PEP) shares are trading around $143, up roughly 2% on the day, but the stock still has plenty of ground to recover. Even after today's bounce, it's sitting about 11% below its all-time high above $159 reached earlier this year and only 6% above its 52-week low of $132.96.

The drop finally makes one of the market's most recognized Dividend Kings more appealing to long-term investors. The real issue now is whether this recovery will be the initial phase of a longer recovery or just a pause prior to another downward turn.

Q1 Earnings Revealed a Real Volume Turnaround

The first-quarter '26 results (on April 16) continue to be the cornerstone of the investment thesis. Revenue increased 8.5% YoY to $19.44 billion and core EPS of $1.61 exceeded expectations by almost 4%. On a GAAP basis, earnings rose 27% to $1.70 per share.

But the biggest lesson was not revenue or earnings – it was growth in volume.

PepsiCo Foods North America reported a 2% volume increase and a 4% unit growth, bringing them closer to adding around 300 million additional consumption occasions, compared to the previous year. One of the best indicators that the company is doing the right things in terms of focusing on smaller packages and value add products is the fact that it is drawing back price-conscious consumers that were previously trading down. The next quarterly reporting period will be the proving ground to see if that momentum can be maintained or it's just a one-quarter bounce.

A 4% Dividend Hike Signals Management's Confidence

Management also provided another boost to income investors' confidence.

PepsiCo raised its annual dividend by 4%, effective with the June 2026 payment, while reaffirming full-year guidance for 2% to 4% organic revenue growth. Management also is forecasting better performance in the second half of the year within that range.

It is the 53rd consecutive annual dividend increase for PepsiCo, and brings the dividend yield to about 4.19%. If you are a long-term investor, then that's an important sign. Companies generally don't commit to higher dividend payments unless they're confident in future cash flows.

UBS Cuts Its Target but Keeps a Buy Rating

UBS lowered its price target on PepsiCo to $172 from $186, but maintained its Buy rating.

The firm noted that PepsiCo has been the third-worst-performing stock across its entire coverage universe since April 16, falling nearly 14% over that period. UBS also acknowledged that Frito-Lay North America's return to historical growth rates may take longer than previously expected.

Despite that, the bank feels PepsiCo has a viable path ahead for both organic revenue growth and earnings growth, which many packaged food competitors do not have. That's an important distinction, as the weakness in the share price has been more severe than the deterioration in the underlying business.

Barclays and Other Analysts Turn More Cautious

Not everyone on Wall Street is as optimistic.

Barclays lowered its price target from $158 to $144, but preserved its Equalweight rating, noting uncertainty about whether the PepsiCo Foods North America turnaround will persist. The firm now anticipates revenue growth of 2.6% in 2026, close to the bottom of its guidance, and an EPS of $8.54, which represents about 4.9% earnings growth.

Companies have also lowered their expectations. Bernstein lowered its target to $142, TD Cowen cut its forecast to $150 on weaker U.S. retail trends, and Piper Sandler reduced its target to $178, pointing to rising input costs and slowing snack distribution momentum.

PepsiCo Stock Price Chart - Source: Tradingview

What's consistent in these revisions is not a bearish tone, but a more measured approach, indicating analysts remain bullish, but with a lower recovery rate than before.

Executive Equity Grants Add Routine Insider Activity

PepsiCo also disclosed a recent Form 4 filing showing that International Beverages CEO Eugene Willemsen received new performance-based and time-based restricted stock units as part of his regular compensation package.

The awards were given as a compensation as opposed to bought through open market and vested from 2027 to 2029. In other words, investors shouldn't interpret the filing as a bullish insider buying signal. Nevertheless, the equity stakes link management's long-term compensation to the company's future prospects, giving executives the same kind of incentive that shareholders are hoping for in terms of improving company performance.

Analyst Targets and What to Watch Next

After the most recent revisions, the mean price target is now between about $142 and $178, with UBS on the high end, and Barclays and Bernstein on the low end. Even after those reductions, most targets still imply upside from the current share price around $141.

Image Source: TipRanks

The next big catalyst is PepsiCo's second-quarter earnings report on July 9. Wall Street is currently expecting EPS of $2.21 on approximately $23.99 billion in revenue. A positive report coupled with confirmation that PepsiCo Foods North America volume growth is not slowing down in the seasonally robust summer months could boost the stock back into the $150s.

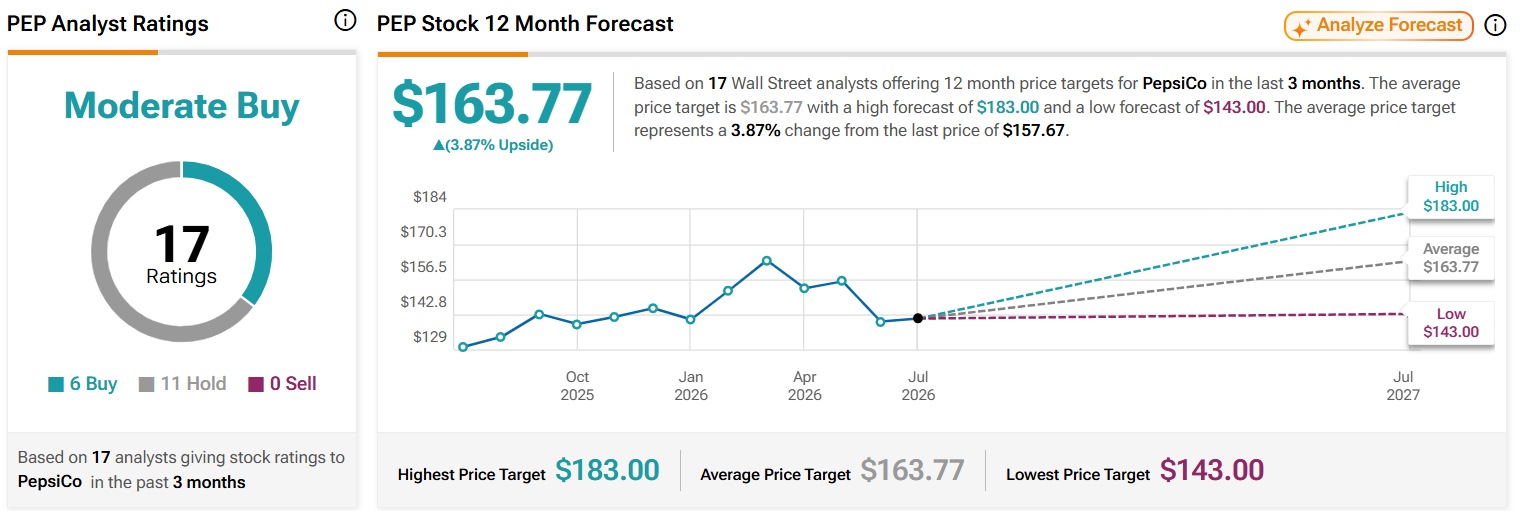

PepsiCo PEP Analyst Ratings and 12-Month Forecast: Moderate Buy Consensus at $163.77 Target

PepsiCo has earned a Moderate Buy from 17 Wall Street analyst ratings issued in the past 3 months including six buys and 11 holds. The average 12-month target price is $163.77 for 3.87% upside with a high target of $183.00 and a low of $143.00.

Overall, the analysts have fairly stable expectations for the consumer staples stock and the chart signals mixed results. The price targets align with the $163.77 average at the top of the channel and 0.5 Fib extension. The low target of $143.00 is consistent with the prior double bottoms and the 200 EMA.

The high target of $183.00 is consistent with major Fib extensions and the channel targets. Relative strength index levels are consistent with neutral readings for the price action and the overall trends remain consistent with the previous highs and lows.

Institutional volume is consistent with the prior support areas and the overall technical pattern structure aligns with the $146-$148 trend line defense, with room to extend to $163-$183 area as targets align with analyst levels. Fundamentals for defensive names have been strong and may continue to be the case. Long $157.67 above $163.80 stop below $143.00 targeting $183.00.

Recommended Articles