Today’s Market Recap: Chip Stocks Retreat Collectively, Meta Rises Against the Trend, Non-Farm Payrolls Become the Next Key Catalyst

Track Market Trends

TradingKey - On July 1, Eastern Time, U.S. stocks closed fluctuating lower on the first trading day of the second half of the year. Although some megacap tech stocks such as Meta ( META) showed strength, a collective pullback in chip stocks dragged down the Nasdaq and the S&P 500. Investors digested U.S. manufacturing and employment-related data while continuing to monitor the upcoming June non-farm payrolls report due this week, as well as the impact of U.S.-Iran negotiations on energy markets and inflation expectations.

As of the close, the Dow Jones Industrial Average fell 0.03% to 52,310.22 points; the S&P 500 Index fell 0.22% to 7,483.23 points; and the Nasdaq Composite Index fell 0.66% to 26,040.03 points.

In terms of sectors and individual stocks, the semiconductor sector was the main drag of the day. The Philadelphia Semiconductor Index closed down about 6.3%, with Nvidia ( NVDA) down 1.25%, AMD ( AMD) down 6.89%, Micron Technology ( MU) down 10.57%, and Intel ( INTC) down 9.03%. Following a substantial rally in AI chip stocks earlier this year, rising market concerns over high valuations, capital expenditure return cycles, and some profit-taking pushed the chip supply chain into a noticeable correction. Performance among megacap tech stocks diverged, with Meta surging approximately 8.83%.

In commodity markets, crude oil prices continued to slide. Brent crude spot closed down 3.02% at $71.2/barrel; WTI ( USOIL) crude spot closed down 2.77% at $68.08/barrel, both hitting near four-month lows. U.S. President Trump stated that negotiations in Qatar were progressing well, easing market concerns over Middle East supply disruptions and continuing to unwind the geopolitical risk premium previously priced into oil.

For precious metals, gold staged a notable rebound. Spot gold ( XAUUSD) jumped over 2% intraday, reclaiming the $4,000 threshold. Soft U.S. employment-related data, combined with remarks from Federal Reserve Chairman Warsh that inflation risks have moderated, led to some easing in the market's pricing of the policy path. However, against the backdrop of the US dollar and Treasury yields remaining relatively high, whether gold's short-term rebound can be sustained still depends on this week's non-farm payrolls data and subsequent comments from Fed officials.

Market News

An important change has occurred in the Federal Reserve's policy communication framework. At the European Central Bank's Sintra Forum in Portugal, Federal Reserve Chairman Warsh stated that the Fed will try to avoid using forward guidance to steer market expectations of the interest rate path in advance, and that future policy meetings will be discussed more on the basis of real-time economic data. He emphasized that, besides reaffirming the 2% inflation target, the Fed will not easily hint at its next policy direction and plans to strengthen the use of real-time and high-quality economic data over the next 9 to 12 months.

US manufacturing data cooled slightly, but remained in expansionary territory. The US ISM Manufacturing PMI for June fell to 53.3 from 54.0 in May, ending its previous upward trend, but remained above the boom-or-bust line for the sixth consecutive month. The new orders and export sub-indices ticked down, indicating that front-loading demand previously driven by Middle East tensions and supply chain concerns is cooling. However, AI investment continued to support electronics, semiconductors, and related manufacturing industries, suggesting that US manufacturing has not experienced a significant stall.

US private sector employment growth slowed as the market awaited the non-farm payrolls report. ADP data showed that private sector employment increased by 98,000 in June, a slowdown from the previous growth rate. Meanwhile, corporate layoffs declined significantly compared to May, indicating that the overall labor market remains stable, but the momentum for new job creation is weakening at the margin. With the June non-farm payrolls report about to be released, this set of data intensified market focus on whether the US labor market is cooling.

Meta is reportedly planning to sell surplus AI computing power, becoming the focus of US corporate news of the day. Meta is reportedly developing a cloud business and plans to sell some of its idle AI computing capacity to external parties. If implemented, this plan would bring Meta directly into the enterprise AI computing services market, putting it in competition with cloud service providers such as Amazon ( AMZN ), Microsoft ( MSFT ), Google ( GOOGL ), and CoreWeave ( CRWV ). The market believes this could help ease investor concerns over Meta's high AI capital expenditures and potentially open up a new source of revenue beyond its advertising business.

The US and Iran held talks in Doha. The United States and Iran concluded a round of indirect talks, with discussions focusing on shipping regulations in the Strait of Hormuz and the unfreezing of Iranian assets, though significant differences remain between the two sides regarding a long-term peace agreement. Iran still wants external recognition of its jurisdiction over the Strait of Hormuz and plans to charge transit fees on vessels in the future, while the US is attempting to block such arrangements. Although the talks sent some signals of de-escalation, uncertainty remains regarding regional security and the outlook for energy transit.

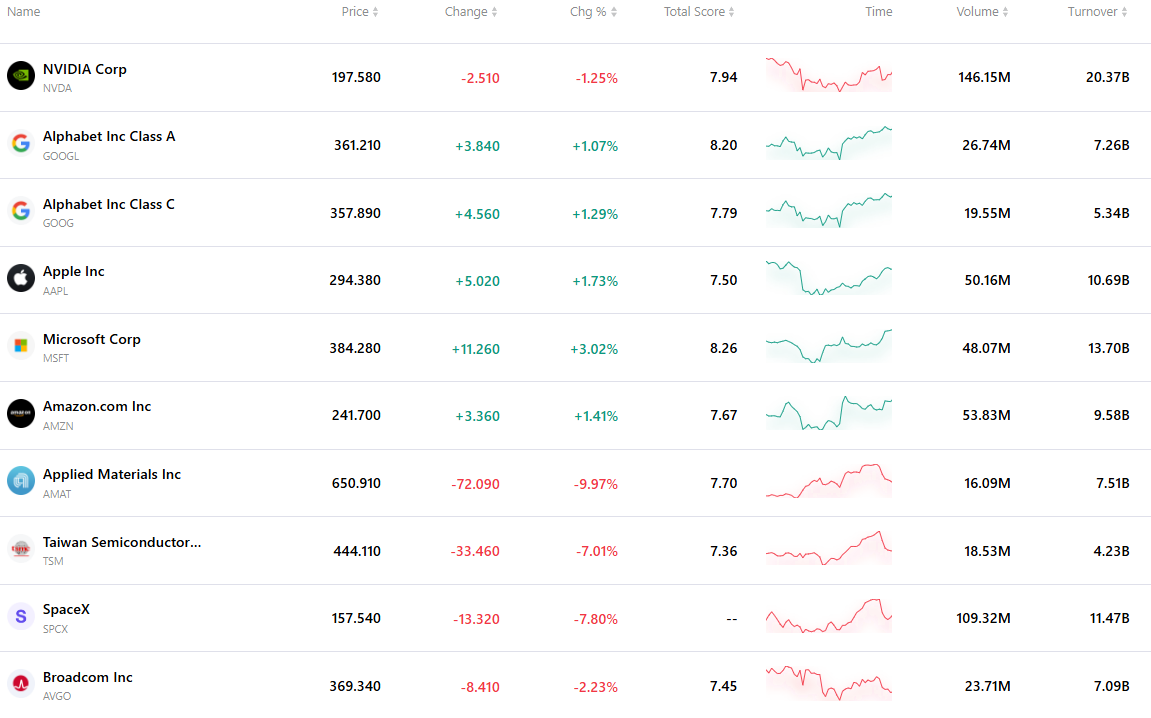

Top 10 Most Active Stocks

The table below lists the ten most actively traded stocks in the latest market. Supported by massive trading volumes and excellent liquidity, these assets have become key benchmarks for tracking global market dynamics.

Recommended Articles