The Stock Market Is Underestimating the Massive Growth Potential of This Artificial Intelligence (AI) Giant That Could Easily Become a $1 Trillion Company

Key Points

Shares of Oracle fell after the company released its latest quarterly report, but investors seem to be missing the bigger picture.

Oracle is filling an important gap in the AI infrastructure ecosystem by building more data centers.

The company's growth rate is poised to jump significantly over the next three years, which could help it easily reach a $1 trillion market cap.

- 10 stocks we like better than Oracle ›

Oracle (NYSE: ORCL) is one of the most important artificial intelligence (AI) infrastructure companies in the world, building data centers for major hyperscalers, AI companies, and many others.

The booming demand for AI solutions and services has driven a surge in the need for dedicated AI data centers. Goldman Sachs, for instance, predicts that demand for agentic AI solutions will drive a 24x increase in token consumption. An AI token is the unit of data that AI models process during the training and inference phases.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Not surprisingly, the massive jump in AI token consumption will create a need for more AI infrastructure. Oracle is filling this gap by aggressively adding new data center capacity. However, the company's shares have underperformed over the past year, dropping by more than 10%, compared with the 37% jump in the tech-laden Nasdaq Composite index.

Its latest quarterly report didn't improve investor sentiment either, as Oracle stock fell by over 8% despite delivering crushing Wall Street estimates. It seems the market isn't giving Oracle enough credit for its healthy growth and bright prospects, especially given its growth potential that could easily help it become a $1 trillion company.

Let's see why it would be a good idea to buy this AI stock while it is beaten down.

Image source: The Motley Fool.

Oracle's aggressive capital spending has spooked investors, but they are missing the bigger picture

Building AI data centers is a capital-intensive undertaking. Not surprisingly, Oracle's capital spending more than doubled in the recently concluded fiscal 2026 (which ended on May 31) to $48 billion from $21.2 billion in the preceding year. The reported capital spending totaled almost $56 billion last year, including $8 billion in customer prepayments.

The company anticipates capital spending of $70 billion this year, with another $20 billion to $25 billion to be financed by customer prepayments. So, Oracle's reported capex could land between $90 billion and $95 billion in fiscal 2027. That will be a significant jump over last year. Oracle plans to finance its share of capex by raising $40 billion through debt and equity. It had announced a $20 billion fundraise earlier this year through a share sale, meaning it will raise an equivalent amount through debt and equity financing.

This explains why Oracle fell despite reporting a 21% increase in revenue last quarter to $19.2 billion and a 24% year-over-year jump in earnings per share to $2.11. Analysts would have settled for $1.97 in earnings per share on revenue of $19.09 billion. However, a closer look at Oracle's backlog explains why the company needs to aggressively ramp up spending.

Oracle's remaining performance obligation (RPO), which refers to the total value of contracts yet to be fulfilled at the end of a quarter, increased to a whopping $638 billion in fiscal Q4. That was way higher than the RPO of $138 billion at the end of fiscal 2025. Importantly, the new data center capacity that Oracle is building will allow it to accelerate the conversion of its RPO into revenue.

The company noted on its latest earnings call that it expects to convert 12% of its RPO into revenue in the next 12 months, with another 34% expected to be realized between 13 and 36 months. So, Oracle is on track to convert 46% of its backlog, or $293 billion, into revenue over the next three years. Of that, almost $77 billion is projected to be converted into revenue within the next year.

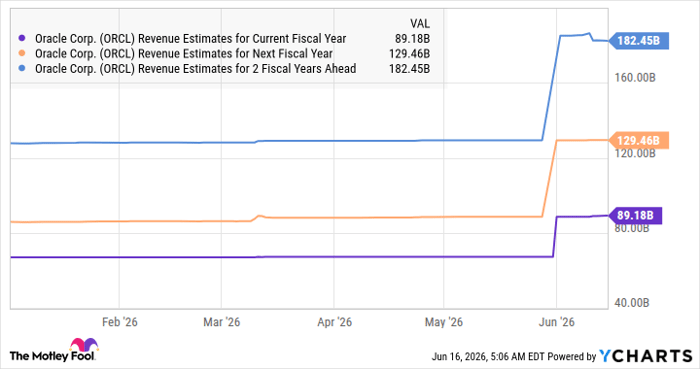

This clearly points toward a significant acceleration in Oracle's growth. The company reported $67.4 billion in revenue in fiscal 2026, up 17% from the prior year. The fiscal 2027 revenue estimate of $90 billion points to a 33% jump in its top line. The growth rate will pick up in subsequent years as RPO conversion into revenue accelerates, which is precisely what analysts anticipate.

Data by YCharts

Of course, the aggressive data center build-out will negatively impact its margins in the near term. Oracle CFO Hilary Maxson noted on the earnings call:

Our fiscal year 2027 gross margin will step down due to timing for the ramp up of our data center projects into their full revenue contribution plus impacts from mix. While these investments are creating pressure on near-term gross margins in our infrastructure business, we expect margin performance in infrastructure to improve rapidly as we reach full contractual revenue levels at our data centers.

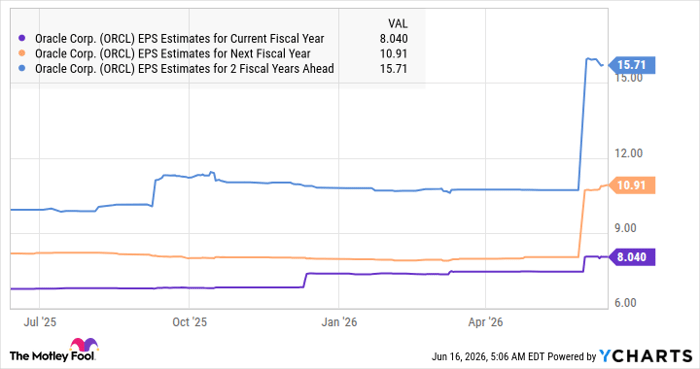

This explains why Oracle expects its fiscal 2027 earnings per share to increase by 18% to $8.05. However, as Oracle fulfills more of its contractual obligations, its earnings growth should also accelerate.

Data by YCharts

A trillion-dollar company hiding in plain sight

The chart above indicates that Oracle's earnings could jump to $15.71 per share after three years, accelerating significantly from the growth anticipated in the current and next fiscal years. The tech-laden Nasdaq-100 index has a forward price-to-earnings ratio of 26.6. Oracle, for comparison, trades at 24 times forward earnings.

Assuming Oracle trades at 26 times earnings after three years (almost in line with the Nasdaq-100) and its earnings per share indeed reach $15.71, its stock price could increase to $408. That's 111% higher than Oracle's current stock price. The company has a market cap of $554 billion as of this writing, which means Oracle stock could jump significantly from current levels and become a trillion-dollar company in the next three years.

Should you buy stock in Oracle right now?

Before you buy stock in Oracle, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Oracle wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $440,440!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,303,950!*

Now, it’s worth noting Stock Advisor’s total average return is 959% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 16, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group and Oracle. The Motley Fool has a disclosure policy.

Recommended Articles