TradingKey Wall Street Weekly Report: May Nonfarm Payrolls Surge by 172,000, Far Exceeding Expectations; Us Stocks Close the Week Lower, High-Valued Tech Stocks Tumble

Previous Week’s Market Review & Analysis

Macroeconomic Landscape:

The U.S. manufacturing sector expanded for the fifth consecutive month in May, with the ISM Manufacturing PMI rising to 54.0, up from 52.7 in April, marking its highest level since May 2022. New orders increased to 56.8, from 54.1, while price pressures remained intense, with the prices index at 82.1, easing slightly from 84.6, due to higher energy and material costs linked to the Iran conflict and supply disruptions. On June 5, the U.S. Bureau of Labor Statistics reported that total nonfarm payroll employment increased by 172,000 in May, and the unemployment rate remained unchanged at 4.3 percent. Job gains were notable in leisure and hospitality, local government, and health care, while employment in financial activities declined. Average hourly earnings rose by 0.3 percent in May, bringing the year-over-year increase to 3.4 percent. Federal Reserve Governor Michael S. Barr warned in a June 2026 speech that recent bank deregulation amid a financial boom could weaken the system's resilience against future crises.

Market Performance Overview:

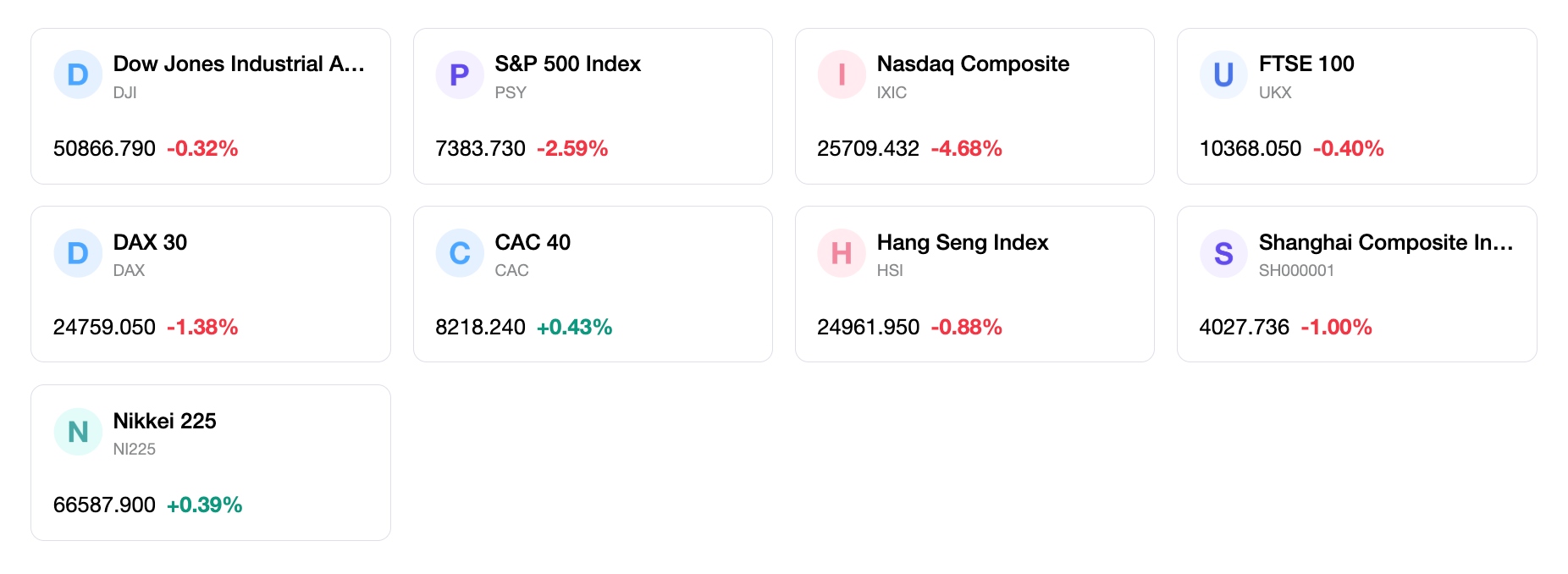

The S&P 500 closed at 7383.74, down 2.59% for the week; the Dow Jones Industrial Average closed at 50866.78, down 0.32% for the week; the Nasdaq Composite closed at 25709.432, down 4.68% for the week; and the Russell 2000 closed at 2833.502, down 2.94% for the week.

Key Events Analysis:

The release of the May jobs report on June 5 showed a stronger-than-expected increase in nonfarm payrolls, adding 172,000 jobs, exceeding the consensus forecast of 85,000. The unemployment rate held steady at 4.3%, in line with expectations. ISM Manufacturing PMI data released on June 1 indicated continued expansion in the manufacturing sector for May, albeit with persistent price pressures. Former Fed Chair Jerome Powell, in a speech on June 1, emphasized the importance of Fed independence from political pressure. Several key technology and retail companies reported earnings during the week, with some mid-cap tech companies exceeding expectations. Geopolitical developments included continued speculation and reports of potential peace deals and ceasefire extensions between the U.S. and Iran, which contributed to falling oil prices.

Flows & Sentiment:

The VIX (volatility index) was recorded at 21.51 as of June 5, which is 16.0% above its long-term average, suggesting some underlying market uncertainty. Analysts pointed out that market breadth was low, with only a few sectors dominating the overall market performance.

Overall Assessment:

The robust jobs report further affirmed the resilience of the U.S. labor market, yet also suggested a reduced likelihood of near-term interest rate cuts. Concerns about concentrated market leadership and persistent inflation pressures, as highlighted by ISM data, suggest a cautious but constructive outlook.

Next Week’s key market drivers and Investment Outlook

Upcoming Events:

The coming week will feature significant economic data releases, including the U.S. Consumer Price Index (CPI) for May on June 10, which will be a crucial indicator for inflation trends. The Producer Price Index (PPI) for May is also scheduled for June 11. Additionally, the Bank of Canada and the European Central Bank will announce their interest rate decisions.

Market Logic Projection:

Expected evolution of macro conditions and micro-fundamental factors: The market will likely closely scrutinize the upcoming inflation data for signs of moderation, which could influence Federal Reserve policy expectations. Continued strength in labor market data could further cement the Fed's data-dependent stance, suggesting no immediate urgency for rate cuts. Corporate earnings season has largely concluded, so macro data will likely dominate sentiment.

Strategy & Allocation Recommendations:

Risk-appetite guidance, sector views, and representative equity ideas: Given the ongoing strength in the technology sector and AI-related themes, maintaining exposure to quality growth stocks remains a key recommendation. Investors should consider selective opportunities in sectors showing broadening strength, but also be mindful of the narrow market leadership. A cautious approach is warranted due to potential volatility around inflation data.

Risk Alerts:

Key risks deserving attention include the persistence of elevated inflation, which could lead to a more hawkish stance from the Federal Reserve than currently priced in by markets. Geopolitical developments, particularly concerning the Middle East, continue to pose a risk to energy prices and overall market stability. The concentrated nature of recent market gains also presents a risk, as a reversal in leading sectors could impact overall index performance.

Markets Weekly

5-day index performance

Recommended Articles