USD/JPY Nears 160 Level Again. When Will Bank of Japan Intervene Again?

TradingKey - USD/JPY touched 159.65 during early Asian trading on May 28, just shy of the 160.70 low hit prior to the Japanese authorities' intervention in early May.

[USD/JPY Year-to-Date Daily Candlestick Chart, Source: TradingView]

Following the Bank of Japan's intervention which briefly pushed the pair to 155.50, approximately 80% of those gains have been surrendered in just three weeks.

What was the impact of Japan’s initial intervention?

On April 30, Japanese authorities entered the market for the first time in two years after the yen breached the 160 level. Reports indicate that the scale of this Bank of Japan intervention exceeded $90 billion, making it the most aggressive single-bout action on record.

The yen surged 3% that day, as USD/JPY plunged from above 160 to 155.57, marking its largest single-day decline since 2022. This round of intervention dealt a heavy blow to short-term speculative shorts; according to CFTC data, net short yen positions held by leveraged funds fell to 61,340 contracts in the week ending May 5, the lowest in nearly a month.

Additionally, the forced liquidation of shorts spilled over into other correlated assets, with Brent crude retreating sharply and 10-year Treasury yields trending lower. Katsunobu Kato significantly escalated verbal warnings around the time of the intervention, explicitly declaring readiness to take action against excessive foreign exchange volatility at any moment.

The primary objective of Japan’s first intervention was not to reverse the yen's depreciation trend, but rather to curb and mitigate the pace of the currency's decline, thereby securing an observation window for policy adjustments.

Why has the Bank of Japan's intervention had limited impact?

The core dilemma of intervention remains unchanged; the Bank of Japan is using liquidity to buy a window of time, but the interest rate structure has not fundamentally shifted. The yield spread between the BoJ and the Fed ensures that yen financing costs remain the lowest among major global currencies, making the carry trade returns from shorting the yen extremely attractive.

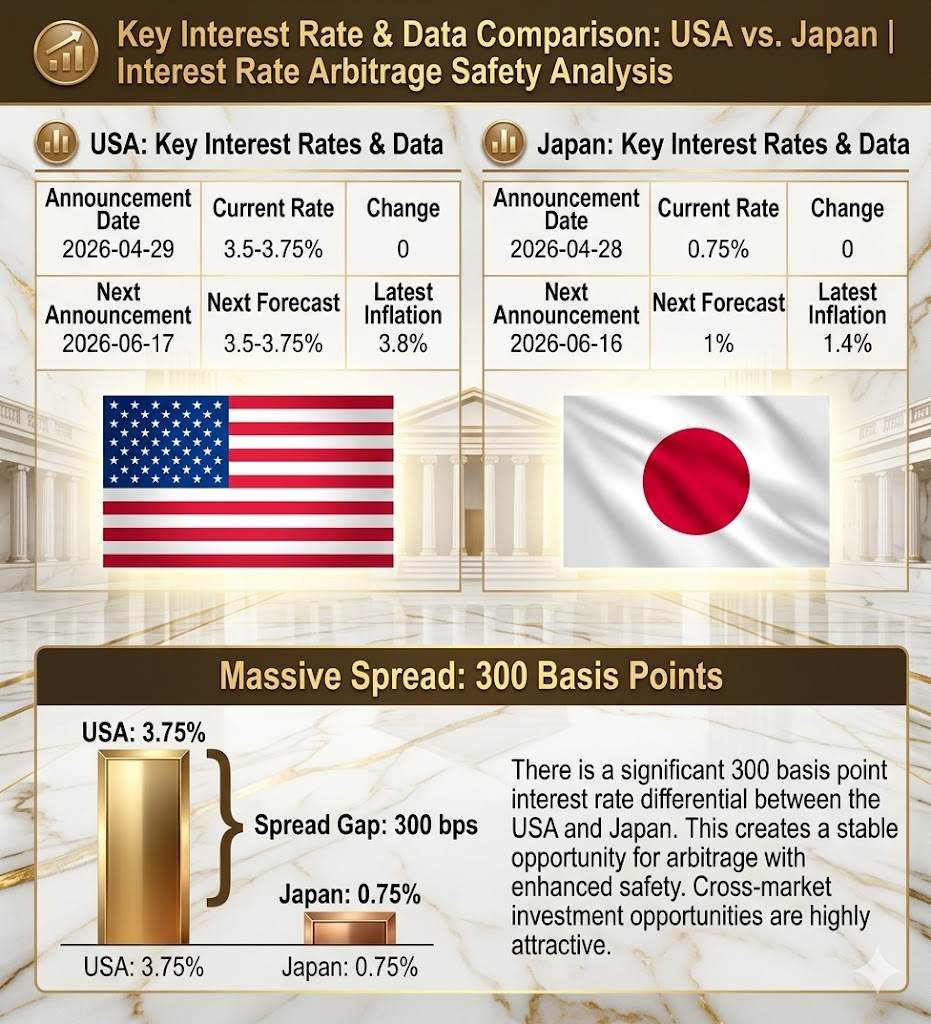

[There is a 300 basis point interest rate differential between the U.S. and Japan, Source: TradingKey]

Driven by an absolute interest rate differential of nearly 300 basis points between the U.S. and Japan, the safety cushion for carry trades is sufficiently solid. When the market realized that intervention could not change the fundamental reality of the rate gap, capital that was previously forced to close positions quickly flowed back to re-bet on yen weakness.

Meanwhile, approximately 80% of the intervention's impact was erased within just three weeks as the exchange rate rapidly returned toward the 160 level, validating this logic. For the Bank of Japan, the 160 level is a psychological line of defense and a "speed bump" while waiting for macro conditions to shift, but simply buying time cannot produce a trend reversal.

Based on the current interest rates set by the Bank of Japan and the Federal Reserve, an absolute spread of 275-300 basis points exists between the U.S. and Japan, making the safety of carry trades sufficiently robust. Upon realizing that intervention cannot change the fundamental reality of the spread, market capital has resumed betting on yen depreciation.

As long as this interest rate structure remains unchanged, any intervention can only smooth short-term exchange rate volatility and cannot reverse the long-term trend.

Rate hikes may be an inevitable choice after intervention fails.

If a consensus forms in the market that intervention is "inevitably ineffective," then the Bank of Japan's intervention will only slow the pace of the yen's depreciation, and the exchange rate will continue to see-saw before a breakout.

The only path to breaking this mechanism is for the interest rate differential to narrow.

In the current context, narrowing the interest rate differential requires at least one of two conditions: a clear rate cut by the Fed or a meaningful rate hike by the Bank of Japan.

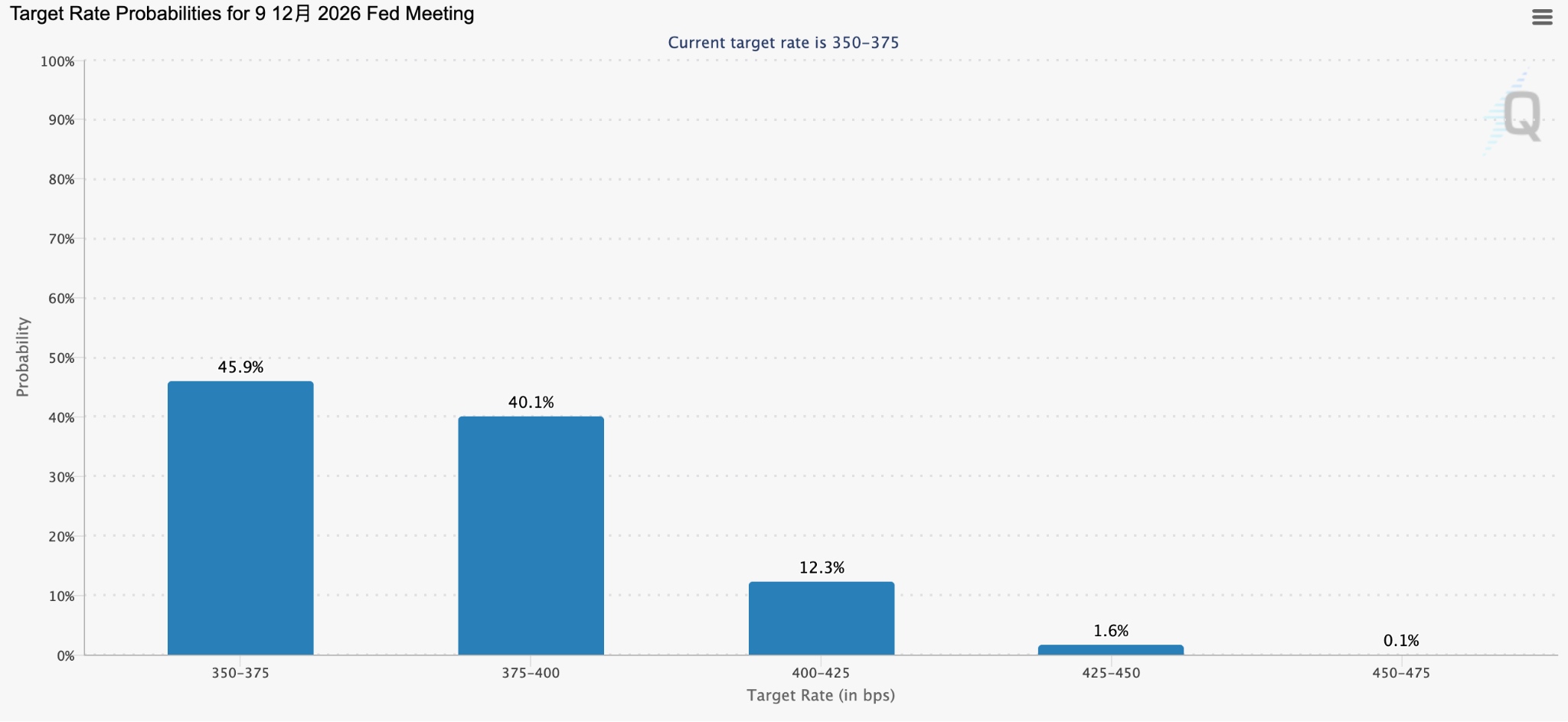

Driven by rising oil prices, the inflation issues currently facing the U.S. are prompting expectations for Fed policy to continue tightening; to date, market pricing indicates that traders at one point bet the probability of a Fed rate hike this year was higher than that of keeping rates steady.

Against this backdrop, the market will likely engage more deeply in USD/JPY carry trades, leading to expectations of further yen depreciation and forcing the Bank of Japan toward a rate-hike path.

[Fed rate hike probability for the year, Source: CME Group]

However, the Bank of Japan's decision-making framework is constrained. On one hand, April PPI surged 4.9% year-on-year, and wage growth has exceeded 5% for three consecutive years, meeting the inflationary conditions for a rate hike. On the other hand, Q1 GDP grew by only 0.5% quarter-on-quarter, with the contribution of exports far outweighing domestic demand and private consumption still shrinking. Balancing the protection of livelihoods against managing inflation has become the BoJ's greatest dilemma.

Previously, an internal divergence had emerged within the Bank of Japan over the "timing of rate hikes" rather than "whether to hike." In the April meeting, three members voted directly in favor of a rate hike, a rare internal split in the bank's history.

Second Intervention Imminent: What Signals Should Investors Watch?

Should Japanese authorities intervene for a second time, the pace, intensity, and method will depend heavily on one external variable: the degree of acquiescence from the U.S. Treasury.

The signals sent by Bessent during his previous visit to Japan were quite clear: the U.S. prefers Japan to support the yen through interest rate hikes rather than by selling U.S. Treasuries. This means that even in the event of further intervention, Japan is likely to prioritize depleting its dollar cash deposits over tapping its Treasury reserves.

Currently, market expectations for intervention are no longer anchored to specific levels, but rather to the premise that Japan will not lightly use its U.S. Treasuries. Under this assumption, 160 remains a threshold that could be breached.

Foreign exchange investors should focus on the actual signals from the Bank of Japan's June meeting—the magnitude of rate hikes, the resolve of its rhetoric, and its judgment on the sustainability of the 'wage-price spiral.' Until then, the maneuvering at the USD/JPY 160 level is essentially a test of the limits of patience between the market and the central bank.

Recommended Articles