Last Year, New Fed Chair Kevin Warsh Believed Artificial Intelligence Would Pave the Way for Interest Rate Cuts. Now, It's Doing the Exact Opposite.

Key Points

Kevin Warsh begins his tenure as chair of the Federal Reserve's Board of Governors with questions about the broader economy and potential agency reforms.

While Warsh has argued for interest rate cuts based on AI productivity gains, AI has arguably been pushing yields higher lately.

The Iran war has certainly contributed to higher yields, but it's not the only factor, according to one macroeconomic strategist.

- These 10 stocks could mint the next wave of millionaires ›

In a Wall Street Journal op-ed last November scrutinizing the Federal Reserve, Kevin Warsh said artificial intelligence (AI) would be a "significant disinflationary force." Many experts took this to mean that Warsh was suggesting the benefits of AI could pave a path for the Fed to further cut interest rates.

A lot has happened since then -- including Warsh's installation as the Fed's new chairman. But right now, AI is having the opposite effect and is likely contributing to elevated inflation.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

In fact, it could be the very thing that forces the Fed to raise interest rates later this year.

Official White House photo by Daniel Torok.

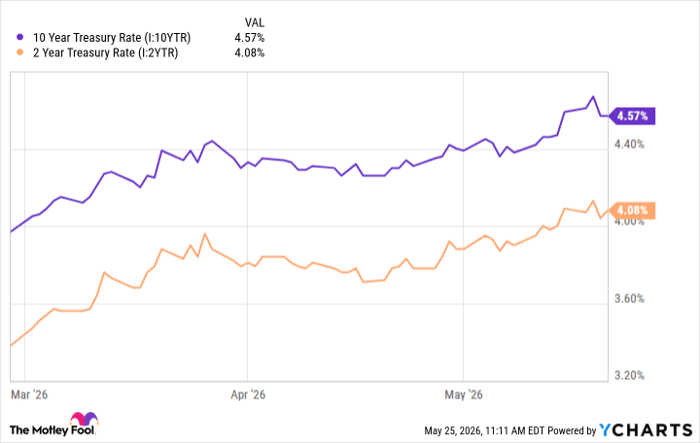

Significant AI capex may be driving yields higher

Many have assumed that the Iran war has led to the recent significant rise in bond yields.

10 Year Treasury Rate data by YCharts.

There's no doubt that it could be a significant contributor. Conflict in the Middle East has driven oil and gas prices higher. While energy is stripped out of core inflation, it tends to have a trickle-down effect on all aspects of the economy. Although many strategists and investors are banking on a clearer agreement between the U.S. and Iran, it still seems too soon to suggest that such an agreement, if made, will definitely hold up. Furthermore, oil and gas prices are unlikely to return to pre-war levels.

But even if the agreement does hold, some experts still don't think the war is having the largest effect on inflation and bond yields right now.

Brian McCarthy, a managing principal at the macroeconomic strategy firm Macrolens, actually attributes this recent climb in bond yields to AI capital expenditures (capex), which have soared this year.

In 2025, the "Magnificent Seven" spent an estimated $400 billion on capex, largely for AI infrastructure, such as data centers, chips, and servers. Most of this is driven by the hyperscalers, huge cloud companies like Amazon and Microsoft whose infrastructure needs require more and more investment.

The "Magnificent Seven" entered the year guiding for a 70% increase in AI capex, which would bring 2026 levels to $680 billion. But following first-quarter earnings reports, that guidance was apparently too light. The group largely raised guidance and now expects an estimated $725 billion in capex this year.

It's a staggering amount, and who knows how many times the hyperscalers will raise guidance this year.

It's also the main driver of bond yields right now, according to McCarthy, who said the rise in yields isn't due to inflation. Bond yields have risen close to 50 basis points (half a percentage point) since the Iran war started (as of May 26), but had been up as much as 60 bps.

However, McCarthy said the break-even inflation rate is up only 15 bps in this period, while the rest is attributable to the real inflation rate. The break-even rate is based on the market's inflation expectations, while the real rate is more closely tied to the market's growth expectations. McCarthy said:

[I]t's not exclusively or even predominantly the Iran war and the oil price spike that's driving this move. I believe it's the big upward revisions we've had to AI capex. We're now looking at the increment of 2025 to 2026 in AI capex going from $380 billion to maybe $800 [billion]. That $400 billion and change is 1.3% of GDP, and that goes right to GDP growth. So this is a very strong driver of GDP momentum at this point.

Warsh is interested in looking at inflation through a new lens

Interestingly, economic trends that are often viewed as positive can be viewed negatively in certain scenarios.

For instance, in recent years, strong job reports and historically low unemployment were often viewed negatively by investors because they drove inflation, thereby preventing the Fed from cutting rates. That seems to be what's happening here, as typically, economic growth is viewed positively.

As of this writing, investors betting on changes to the benchmark federal funds rate see the Fed holding rates steady for the rest of the year, then hiking in January 2027. Keep in mind that economic conditions, or at least the view of them, can change quickly, and these probabilities change all the time.

Warsh has also talked about looking at inflation through a different lens. He wants to focus not on one-time changes driven by geopolitics, beef prices, or other "tail risk," but on the change once all the "one-offs" are removed, and on their effect on the economy.

It's hard to know exactly what this means for Warsh's first few months, and whether he'll use this new lens to suggest that inflation is less of a problem than some believe.

However, the market also seems to be testing Warsh as he begins his tenure. If the 10-year U.S. Treasury yield keeps rising toward 5%, it will be harder for Warsh not to contemplate a rate hike, which could anger President Donald Trump.

Given what McCarthy said and the difference between break-even and real inflation, AI could prove to be the culprit.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 984%* — a market-crushing outperformance compared to 210% for the S&P 500.

They just revealed what they believe are the 10 best stocks for investors to buy right now, available when you join Stock Advisor.

See the stocks »

*Stock Advisor returns as of May 28, 2026.

The Motley Fool has a disclosure policy.

Recommended Articles