AMD Stock Has Doubled This Year. Is It Still a Buy?

Key Points

AMD's data center business is getting stronger.

The company's stock is now incredibly expensive.

Larger rival Nvidia may be the better choice.

- 10 stocks we like better than Advanced Micro Devices ›

Advancved Micro Devices (NASDAQ: AMD) has been one of the best-performing artificial intelligence (AI) stocks in 2026 so far. It has basically doubled in 2026, but nearly all of that run started in April. The question is whether AMD can continue this run throughout 2026 or whether there are better options available.

AMD just reported a blowout quarter, which helped boost the stock, but is it fully valued? Let's take a look.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

AMD's business isn't just AI-focused

Unlike its peer Nvidia (NASDAQ: NVDA), AMD doesn't get all of its revenue from AI-related products. It has a much more balanced business, but if growth rates continue trending in the direction they are, AMD could become a lot more AI-focused than it is now.

In Q1, its data center division saw 57% revenue growth to $5.78 billion. Its other non-AI divisions also did quite well, with Client & Gaming rising 23% year over year to $3.6 billion and Embedded increasing 6% to $873 million.

If AMD's data center division continues rising quickly, that will transform AMD into a more Nvidia-like company, eliminating the balance that some investors prefer with AMD. AMD's long-term projections indicated a compounded annual growth rate (CAGR) of 60% for its data center division.

In comparison, its other two divisions will experience a 10% CAGR over the next five years. This will leverage AMD heavily toward AI, completing the transformation into an AI-focused business. That could be a good or bad thing, depending on where you think AI demand will go.

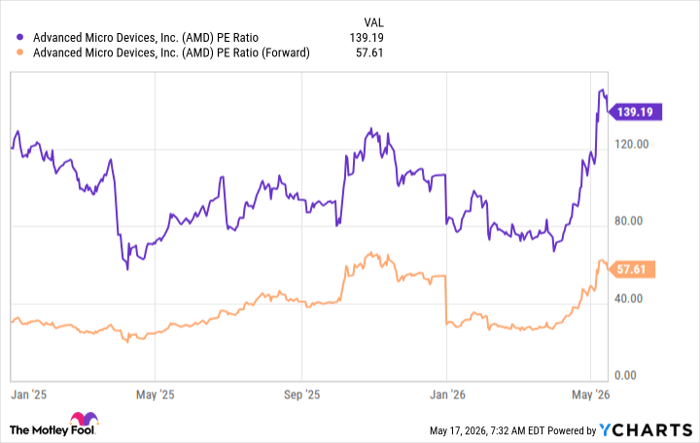

The market clearly loves the direction in which AMD's business is headed, which is why it has done so well over the past few months. However, that run-up comes at a price. AMD's stock is no longer cheap by any measure. It trades for 139 times earnings and 58 times forward earnings.

AMD PE Ratio data by YCharts

This indicates that AMD's earnings will skyrocket this year, but even after a strong year, the stock will still be very expensive. Investors need to ask themselves if this is a price worth paying, especially when Nvidia is growing at a much faster rate and trades for 27 times forward earnings.

To me, Nvidia is the far better investment, and AMD is only an alternative that some like to champion. However, AMD has been the better stock to own as of late, so the Nvidia superiority assessment hasn't panned out.

Time will tell which of these two is a better long-term investment, but I'm still taking Nvidia over AMD right now.

Should you buy stock in Advanced Micro Devices right now?

Before you buy stock in Advanced Micro Devices, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Advanced Micro Devices wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $481,750!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,352,457!*

Now, it’s worth noting Stock Advisor’s total average return is 990% — a market-crushing outperformance compared to 206% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 20, 2026.

Keithen Drury has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles