3 Reasons to Buy MercadoLibre Stock on the Dip

Key Points

MercadoLibre is investing in its future.

The company's moat can help it tap into long-term opportunities.

The stock is fairly valued after the recent drop.

- 10 stocks we like better than MercadoLibre ›

MercadoLibre (NASDAQ: MELI) has been a terrible stock to own over the past 12 months. The company's shares are down 38% over this period. The e-commerce specialist's recent first-quarter update, released on May 7, further extended the significant market losses it had already experienced. However, despite MercadoLibre's challenges, there are good reasons to invest in the company and hold onto its shares for a while. Here are three of them.

1. Necessary investments for the future

In the first quarter, MercadoLibre's revenue grew by a healthy 49% year over year to $8.8 billion. That was a fairly strong top-line performance for the company. However, MercadoLibre's margins and profits declined meaningfully. The company's operating margins dropped by 6% year over year to 6.9%, while its net earnings per share came in at $8.23, down from the $9.74 reported in the year-ago period.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

Declining profits and worsening margins were key reasons MercadoLibre's shares dropped after it announced its first-quarter results. However, MercadoLibre not doing so well on the bottom line isn't surprising given recent developments. The e-commerce leader has been facing stiff competition in its home market in Latin America. It has chosen to address this by sacrificing short-term margins and profits to extend initiatives that may pay off handsomely in the long run. One thing the company has done is lower the threshold for free shipping in Brazil, an initiative that, MercadoLibre argues, is already showing results in the form of stronger gross merchandise volume growth.

Free shipping is an important offer that can help boost sales volume and customer spend on e-commerce platforms. Yes, it may lead to lower margins in the near term, but it could also attract more customers and eventually help the company build a stronger ecosystem, eventually making up for the lower near-term profits and margins. It could also help MercadoLibre scale its fast-growing, higher-margin advertising business, since the deeper its ecosystem, the more attractive it becomes to companies looking to place ads in front of potential customers.

That's why this initiative may be worth it. MercadoLibre is pursuing other attractive opportunities in its fintech segment, including expanding its credit card offerings. Many of the people in the markets it serves are underbanked, underscoring another major growth opportunity. This initiative also means higher loan reserves (which contributed massively to margin compression in the period) and, potentially, various credit perks and incentives, all of which can affect profits in the short run. But in the long run, it could all pay off.

2. There is a large addressable market

Another important point to note is that MercadoLibre is looking at a large and growing e-commerce and fintech opportunity. Online retail has been expanding at a good clip in many regions in recent years, but according to some data, Latin America, where MercadoLibre is dominant, has been one of the fastest-growing markets. And even though the company will face competition, it has built a wide moat that could help it maintain its lead over the next decade.

MercadoLibre benefits from deep network effects within its core e-commerce platform. As customers and businesses increasingly join its ecosystem, it becomes even more valuable to those on the outside looking in. MercadoLibre's business also imposes high switching costs for merchants who build online storefronts with the company and use many of its services, including payment, analytics, inventory management, and more.

Lastly, MercadoLibre has built a large infrastructure that enables it to operate across many South American countries, some of which are somewhat politically unstable. This isn't an easy thing to replicate. Of course, none of that means the company's competition can't make some headway. But MercadoLibre's competitive edge, coupled with its investments in the future, can help it capitalize on the attractive growth runway in its core markets.

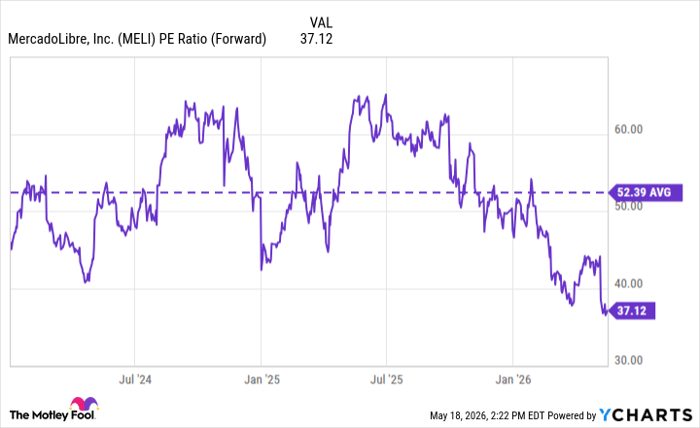

3. The price is right

With MercadoLibre's recent setbacks, the company's shares look about as attractive as they have in years.

MELI PE Ratio (Forward) data by YCharts

Some may argue that the company is still expensive. The average forward price-to-earnings ratio for consumer discretionary stocks is 26.5 as of this writing. However, MercadoLibre is still posting excellent sales growth, while its margins and earnings compression are a result of initiatives that could improve its financial results in the future. My view is that MercadoLibre is fairly valued at current levels and could deliver strong long-term returns to investors who initiate positions today.

Should you buy stock in MercadoLibre right now?

Before you buy stock in MercadoLibre, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and MercadoLibre wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $483,476!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,362,941!*

Now, it’s worth noting Stock Advisor’s total average return is 998% — a market-crushing outperformance compared to 207% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 19, 2026.

Prosper Junior Bakiny has positions in MercadoLibre. The Motley Fool has positions in and recommends MercadoLibre. The Motley Fool has a disclosure policy.

Recommended Articles