SK Hynix Stock Price Surpasses 1.22 Million Won, Hits Record High

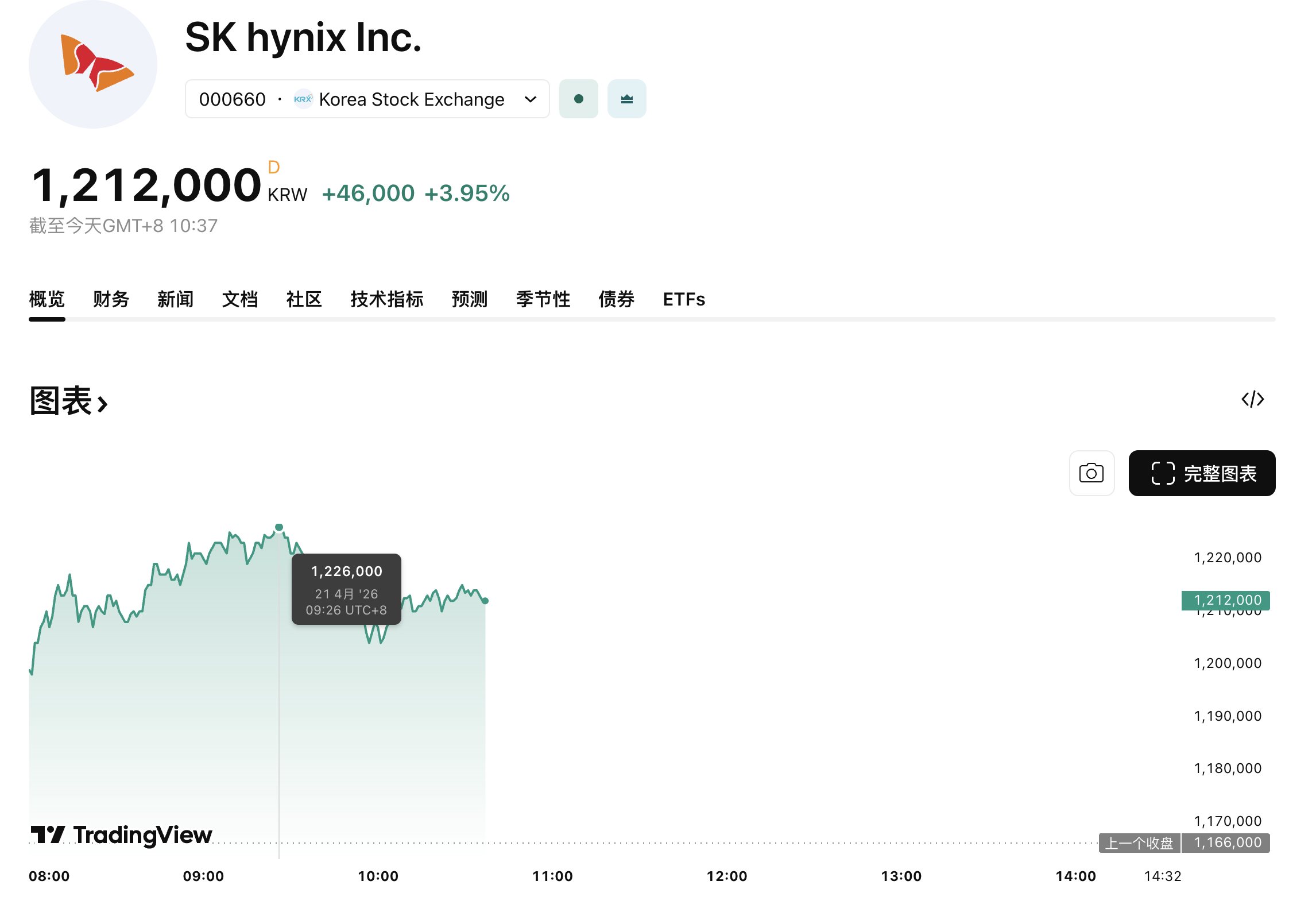

TradingKey - As of April 21, Beijing time, SK Hynix rose nearly 5% in Tuesday's intraday trading, with its share price surpassing 1.22 million won for the first time to hit a record high. The KOSPI index also reached a record high of 6,355.39 points during the session. Global memory chips are currently in a long-cycle upswing, and SK Hynix is among the primary beneficiaries.

[Source: TradingView]

The primary driver behind SK Hynix's stock price surge is the company's mass production of 192GB SOCAMM2 memory modules specifically for NVIDIA's Vera Rubin platform. By porting mobile low-power DRAM to server environments, this product not only doubles the original bandwidth but also reduces power consumption by more than 75%.

Vera Rubin is expected to begin delivery in the second half of 2026. Recent reports suggested that Vera Rubin might be delayed due to supplier capacity constraints; however, the mass production of SK Hynix's SOCAMM2 memory modules has effectively filled the capacity gap, further solidifying its key position as a core HBM supplier for NVIDIA.

A major highlight for SK Hynix is the quarterly earnings report scheduled for release on April 23. KB Securities predicts that SK Hynix's first-quarter operating profit could reach 40 trillion won, setting a new record. Market expectations for revenue stand at 50.1 trillion won, with an operating profit of 34.9 trillion won, representing year-over-year growth of 184% and 369%, respectively.

Strong earnings expectations have prompted several brokerages to raise their price targets. LS Securities maintains a "Buy" rating with a target of 1.5 million won; Citi reiterated its "Buy" rating and raised the target price to 1.7 million won; HSBC Research and Yuanta Securities both set targets of 1.8 million won with "Buy" ratings; while SK Securities issued a target price of 2 million won. Based on Tuesday's intraday price of 1.22 million won, SK Securities' forecast still implies an upside potential of over 60%.

Furthermore, geopolitical risks persist, with the outlook for US-Iran ceasefire negotiations remaining unclear. If the conflict continues to escalate, global risk assets could face a broad sell-off. The specific delivery timeline for Vera Rubin remains uncertain, and any potential delays would impact the production rhythm of SOCAMM2. As the current stock price already reflects high earnings expectations, it may face downward correction pressure if the financial report fails to meet optimistic forecasts.

Recommended Articles