U.S. March CPI Preview: Could Energy Shock Spread Broadly?

TradingKey - At 8:30 a.m. ET on Friday, the U.S. Department of Labor will release the March Consumer Price Index (CPI) report. Markets widely expect inflation to experience its sharpest monthly spike since 2022. This marks the first inflation report to fully factor in the surge in oil prices and represents a key data point in assessing whether the "energy shock" has become widespread.

Market forecasts jump in year-on-year CPI

Based on current data, market expectations are showing highly consistent directionality. The annual CPI rate for March is expected to continue expanding to 3.3%.

Headline CPI for March is projected to rise 0.9% month-over-month, with the year-over-year increase expected to climb sharply from 2.4% to 3.3%, the highest since April 2024. Core CPI, which excludes food and energy, is expected to rise 0.3% month-over-month, with the annual rate ticking up slightly from 2.5% to 2.7%.

Bank of America analysts pointed out that energy prices are expected to rise 10.6% month-over-month in March, serving as the primary driver pushing inflation higher.

The transmission path of energy prices is now clear. Since the outbreak of the Middle East conflict on February 28, WTI crude oil prices have surged from approximately $67 per barrel to nearly $100 currently.

Despite a significant pullback in oil prices following the announcement of a two-week ceasefire between the U.S. and Iran this week, the price peaks throughout March were sufficient to deliver a substantial shock to that month's CPI. TD Securities analysts stated bluntly that the recent surge in crude prices will be the main factor behind the 0.9% jump in the monthly CPI rate.

Minutes from the March FOMC meeting show that Fed officials are concerned that the conflict in the Middle East could cause energy price increases to persist for longer, making it more likely that increased costs will pass through to core inflation.

The pass-through of oil prices occurs on two levels. The direct level is reflected in rising energy prices such as gasoline pushing up headline CPI, while the indirect level involves penetration into a broader range of goods and services through transportation and raw material costs.

On the flip side of market expectations: even if March inflation jumps to 3.3% as anticipated, investors may temporarily view it as a one-time shock—provided they believe oil prices will fall significantly and a permanent ceasefire will be achieved in the Middle East. However, uncertainty regarding the sustainability of the ceasefire is making that premise increasingly fragile.

Energy Shock Spreading: Automotive, Aviation, and Food Sectors Under Pressure Across the Board

From a broader supply chain perspective, the energy shock is spreading downstream along the cost chain. Bloomberg Economics research shows that under similar oil market shocks, commodities such as jet fuel, steel, aluminum, natural gas, fertilizer, and plastics are most prone to price increases, and this cost pressure has begun to materially pass through to end-consumer sectors.

The automotive market is one of the first industries to feel the impact. Automobile manufacturing is highly dependent on steel, aluminum, and plastics, and rising raw material costs are pushing up new car pricing. The used car market has not been spared—Cox Automotive data shows that used car prices have risen to their highest level in nearly three years. The dual price hikes for new and used cars mean that the entry threshold for consumers into the automotive market is being systematically raised.

The airline industry is responding to surging fuel costs by cutting capacity and raising fees. Several airlines have begun cutting flights and increasing checked baggage fees to hedge against the sharp rise in jet fuel prices. These costs will ultimately be passed on to passengers, driving up airfares.

The lagging effect of food inflation likewise cannot be ignored. As a key input for agricultural production, rising fertilizer prices are pushing up cultivation costs. Cost pressures are transmitting along the food supply chain to the shelves, meaning grocery prices in supermarkets could continue to face upward pressure in the coming months.

Furthermore, tariff policies are simultaneously exacerbating price pressures.

JPMorgan analysts noted that regardless of where oil prices ultimately stabilize, tariffs themselves will push up CPI, with impacts covering multiple sectors including entertainment, education, household goods, communications, and personal care. LPL Financial Chief Economist Jeffrey Roach emphasized that while news of a ceasefire has caused oil prices to retreat, the price pressures brought by trade policy have not disappeared as a result.

In addition, a stagflation dilemma has emerged for the Federal Reserve; March non-farm payrolls added 178,000 jobs, far exceeding the expected 65,000, as the labor market's resilience surpassed expectations.

Minutes from the March FOMC meeting show that Fed officials have generally lowered their expectations for rate cuts. Some officials emphasized that with inflation having been above target for five consecutive years, "long-term inflation expectations could become more sensitive to rising energy prices."

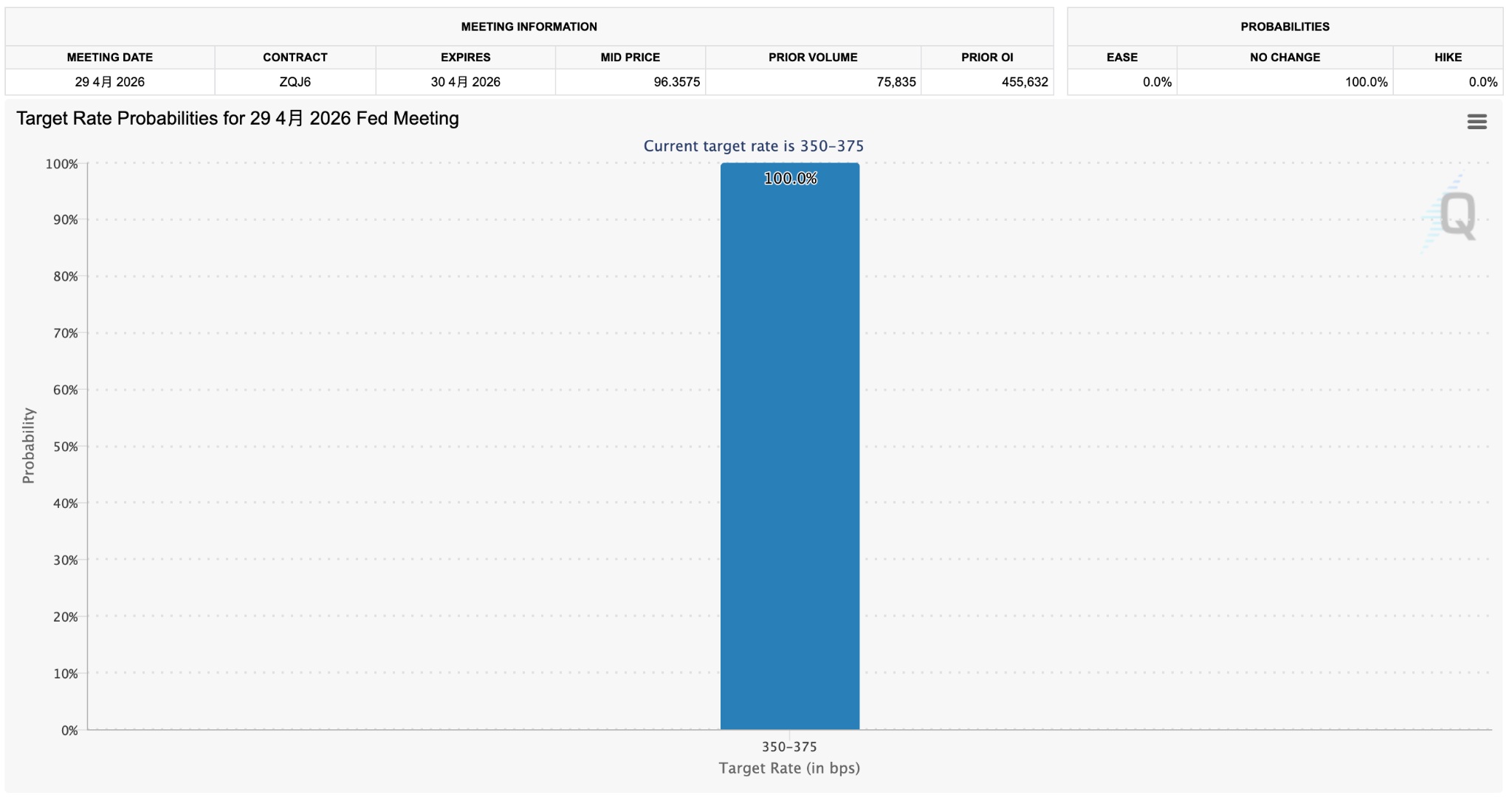

The CME FedWatch Tool shows that the market expects a 100% probability that the Federal Reserve will maintain interest rates at its late April meeting, with rate cut expectations having significantly contracted to a maximum of one for the year.

Persistently high inflation will not only suppress consumer purchasing power but also erode corporate profits and tighten financial conditions. The CEO of JPMorgan referred to inflation as the "skunk at the garden party," suggesting it could derail stock market performance in 2026.

Since the U.S.-Iran conflict persisted throughout the entire month of March, the March CPI data holds significant importance in terms of the transmission of energy prices.

If the CPI significantly exceeds expectations—meaning inflationary pressures are mounting rapidly—high-valuation technology companies led by high-growth stocks will face substantial downside risks; conversely, it could alleviate inflation anxiety, potentially leading to a rebound in rate cut expectations and thus boosting stock market performance.

Recommended Articles