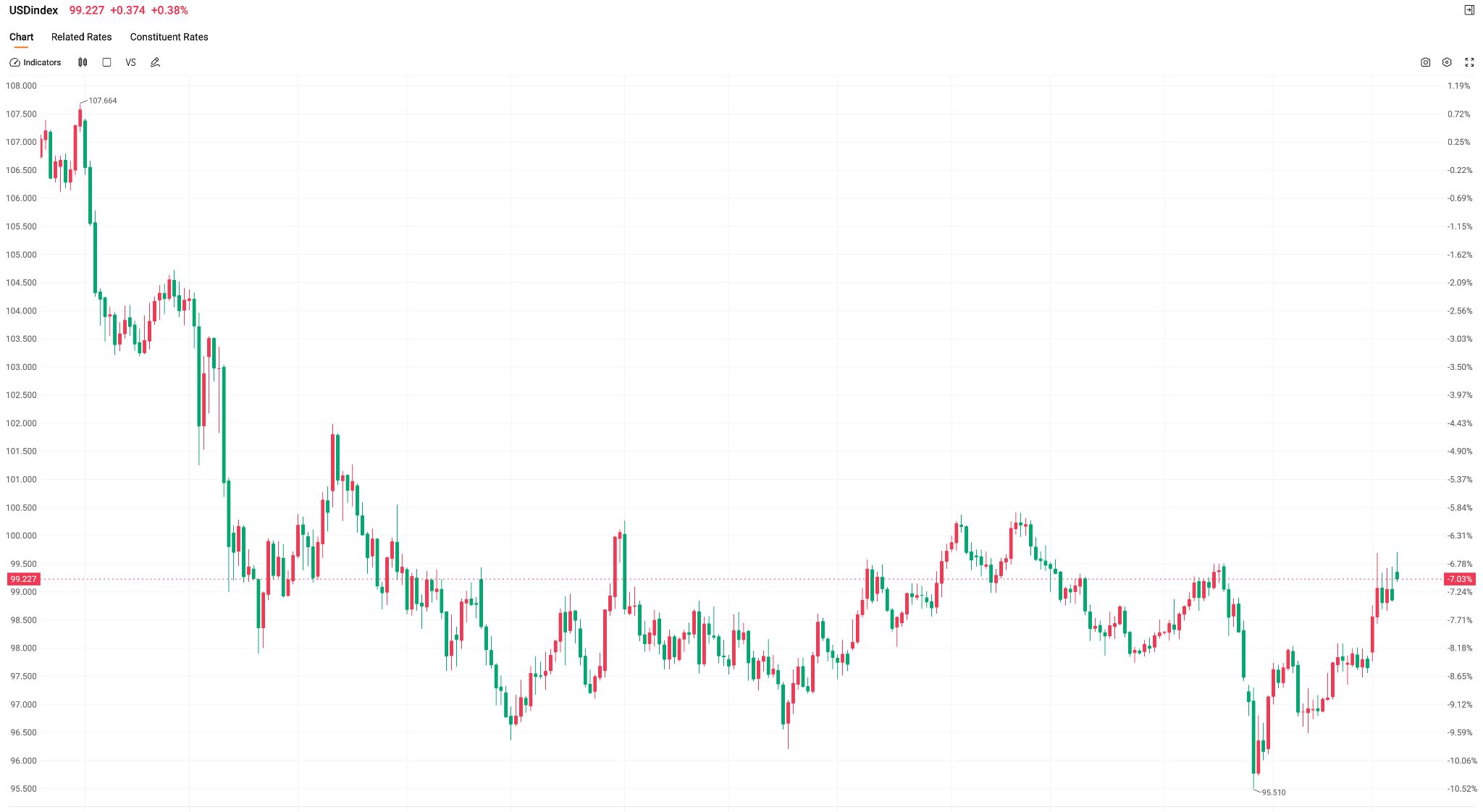

Gold Loses Favor, Is Cash the Only Safe Haven? Dollar Index Hits 100 Mark.

TradingKey - Against the backdrop of unresolved tensions in the Middle East, the U.S. Dollar Index has continued to strengthen, briefly challenging the 100 mark, while the traditional safe-haven asset— Gold (XAUUSD) seems to have lost its original safe-haven properties. Since the U.S. strike against Iran on February 28, gold opened higher with a gap but subsequently retraced continuously, erasing all gains made in the week prior to the conflict.

This performance stands in stark contrast to market expectations that rising geopolitical risks typically drive gold prices higher.

In sharp contrast to gold's trajectory, the U.S. dollar has once again become the preferred safe-haven asset for capital during this round of geopolitical conflict.

As global risk sentiment heats up, capital is flowing rapidly into U.S. dollar assets, driving the Dollar Index steadily higher and once again approaching the psychological 100 level.

Market traders generally believe that within the global financial system, the dollar remains the most liquid and largest safe-haven asset; when uncertainty rises sharply, capital tends to prioritize holding dollar cash assets to maintain liquidity.

Analysts point out that gold's recent failure to sustain a safe-haven rally is largely closely related to the U.S. interest rate environment.

Although rising geopolitical risks typically boost demand for gold, if U.S. interest rates remain high, the opportunity cost of holding gold remains elevated, which to some extent caps its upside potential.

Furthermore, a strengthening dollar also tends to exert direct downward pressure on dollar-denominated gold prices.

At the same time, the market's reassessment of global monetary policy paths is also reinforcing the dollar's appeal.

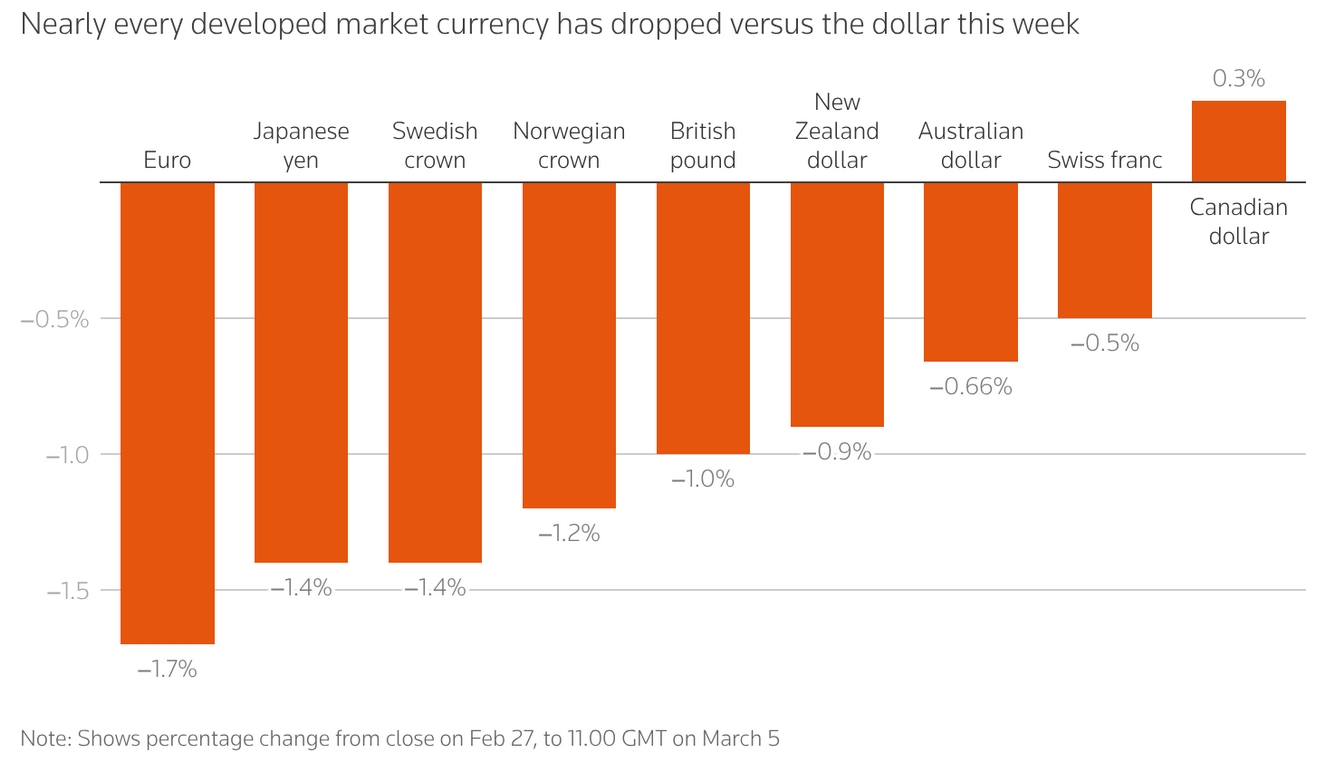

Judging by the performance of the foreign exchange market, the dollar's relative advantage is expanding further.

This widespread currency depreciation reflects a core shift in the current market—against a backdrop of rising uncertainty, global capital is flowing back into U.S. dollar assets.

Due to the dollar's central role in the global financial system, when geopolitical risks or macro uncertainties rise, investors typically prioritize increasing holdings of U.S. dollar cash or dollar-denominated assets to enhance portfolio liquidity and safety.

Concurrently, market repricing of interest rate prospects is also reinforcing this trend.

As rising energy prices could re-ignite inflationary pressures, some investors have begun to scale back expectations for the pace of rate cuts by major central banks.

If the Federal Reserve remains more cautious regarding rate cuts while other major central banks are the first to initiate easing cycles, the interest rate differential between the dollar and other currencies could still widen, thereby continuing to attract global capital inflows into the U.S. market.

Should geopolitical risks and global macro uncertainties persist, the dollar may maintain its strong position in the short term, and the "cash is king" safe-haven logic could continue to dominate the market.

Recommended Articles