Lam Research Corp Stock (LRCX) Moved Up by 3.97% on Jun 21: Drivers Behind the Movement

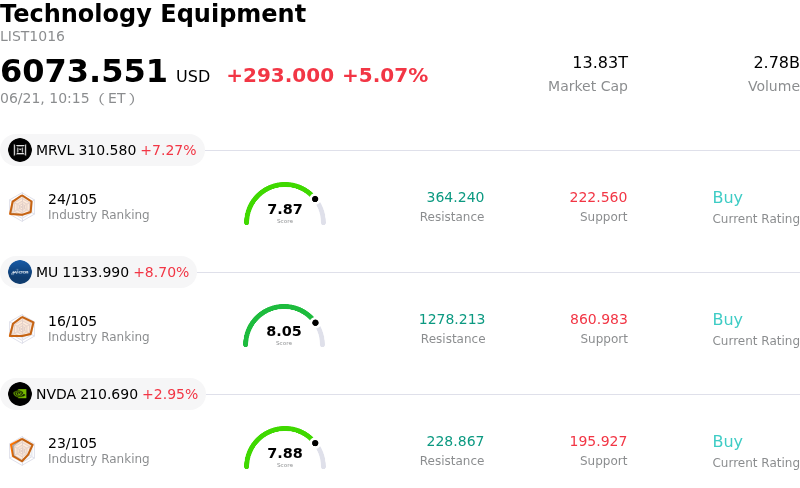

Lam Research Corp (LRCX) moved up by 3.97%. The Technology Equipment sector is up by 5.07%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research has experienced notable upward momentum driven by outstanding fundamental execution and a massive expansion in the broader semiconductor capital expenditure cycle. The company's recent quarterly earnings report surpassed Wall Street expectations on both the top and bottom lines, backed by record revenue and per-share earnings that exceeded the high end of guidance. Furthermore, management provided strong forward guidance for the upcoming quarter, indicating sequential acceleration that the market had not fully anticipated. This fundamental success is heavily tied to the relentless global artificial intelligence infrastructure buildout, which requires advanced deposition and etching tools for high-bandwidth memory and leading-edge logic processors.

A major catalyst for this positive movement is the revised outlook for the global wafer-fabrication equipment market, which the company upgraded to one hundred and forty billion dollars. This optimistic projection is aligned with recent industry-wide data highlighting triple-digit year-over-year growth in global data center component spending. Lam Research is poised to be a premier beneficiary of this trend, forecasting that its own advanced packaging revenue will grow by over fifty percent in the current calendar year. Consequently, multiple major financial institutions have aggressively raised their price targets and reiterated buy ratings, reinforcing institutional confidence in the stock as a key AI momentum winner.

The upward traction is further supported by a historic shift in semiconductor equipment industry dynamics. Rapidly expanding capacities for advanced packaging and high-bandwidth memory stacking have inverted the traditional buyer-seller relationship. For the first time in decades, pricing power is migrating from leading-edge foundries to tier-one equipment manufacturers. As the critical physical layer supporting artificial intelligence hardware becomes a major constraint, suppliers like Lam Research are commanding stronger market leverage, which has fueled aggressive buying by institutional investors.

Despite the strong upward trajectory, the stock has experienced significant intraday volatility. This volatility is primarily driven by an elevated valuation, with the price-to-earnings multiple currently trading well above historical medians, prompting a constant tug-of-war between growth momentum and multiple compression risk. Additionally, Lam Research remains highly exposed to geopolitical and regulatory developments due to its significant revenue concentration in China, which accounts for over a third of its business. These macro worries, combined with recent disclosures of high-profile insider selling and active hedging in the options market, have amplified trading swings even as the overall trend remains highly positive.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 8.446, indicating a buy signal. The RSI at 68.591 suggests neutral condition and the Williams %R at 12.172 suggests overbought condition. Please monitor closely.

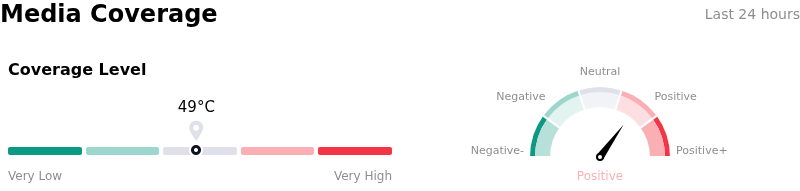

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $332.58, a high of $450.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- High Geopolitical and Export Control Exposure in China: China accounts for approximately 34% to 35% of Lam Research's total revenue, exposing the firm to severe top-line volatility and potential market share impairment as U.S. technology export controls expand and shipment authorization revocations threaten operations.

- Drastic Projected Deceleration in System Shipment Growth: Analysts maintain structural concerns regarding a projected drop in system shipment growth to just 3% in 2026 from 82% in 2025, driven by expected cyclical cooling in both the NAND memory and Chinese logic markets.

- Stretched Valuations and Multiple Compression Risk: Driven by recent AI momentum, the stock's trailing P/E ratio has surged above 72x, vastly exceeding its five-year historical median of 23x and leaving it trading about 16% above the consensus analyst price target, making it highly vulnerable to sharp profit-taking.

- Substantial Insider Selling at Valuation Peaks: Recent Form 4 SEC filings disclosed that Director Eric Brandt divested 54,500 shares in open-market transactions totaling over $19.1 million, compounding investor anxiety over potential near-term valuation peaks and insider net-selling.

Recommended Articles