Lam Research Corp Stock (LRCX) Moved Up by 3.97% on Jun 19: A Full Analysis

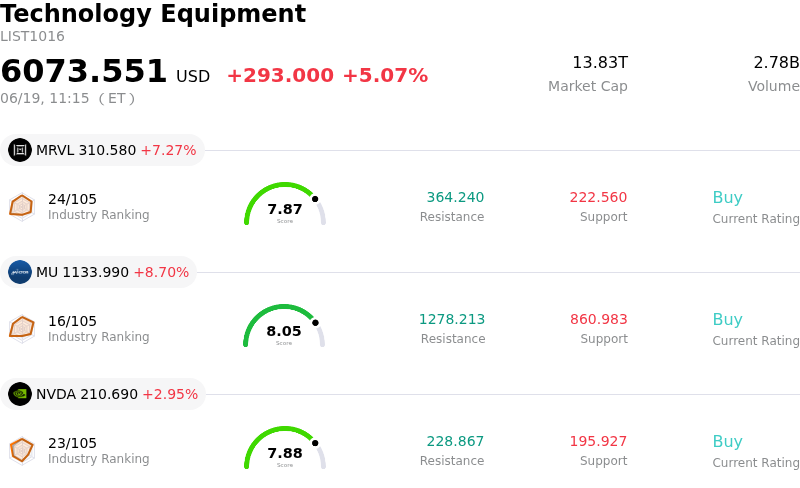

Lam Research Corp (LRCX) moved up by 3.97%. The Technology Equipment sector is up by 5.07%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

The semiconductor sector is experiencing a broad-based rally, significantly boosting equipment manufacturers like Lam Research. Market sentiment has been highly energized by recent major developments, particularly regarding U.S. domestic manufacturing partnerships. Announcements indicating that major domestic chipmakers will produce processors for leading consumer electronics giants within the United States have heightened expectations for substantial capital expenditure. This political and structural push toward localizing production lines directly translates to a robust demand outlook for wafer fabrication equipment suppliers.

Underpinning this momentum is the rapid and accelerating adoption of artificial intelligence workloads. AI-driven demand is forcing semiconductor manufacturers to transition to more complex chip architectures, including high-density 3D NAND stacks, gate-all-around technologies, and advanced packaging. Because Lam Research's specialized etching and deposition tools are critical to these advanced manufacturing processes, the company has witnessed a significant pull-forward in customer technology conversions and a much stronger demand profile than initially anticipated.

Institutional optimism has also been bolstered by a flurry of positive analyst revisions. Several prominent Wall Street firms have dramatically raised their price targets and reaffirmed bullish ratings on the stock. This wave of upgrades is driven by upgraded forecasts for global wafer fabrication equipment spending. With expectations of sustained revenue growth, healthy operating margins, and a sequential acceleration in earnings, big money flow and institutional buying have kept the stock near its historical highs.

Despite the strong upward movement and robust fundamental backdrop, some underlying risks maintain volatility in the stock. Investors remain cautious about stretched valuation metrics, as Lam Research trades at elevated trailing and forward multiples compared to historical averages. Furthermore, geographic concentration remains a persistent concern, as the company's significant revenue exposure to the Chinese market exposes it to ongoing export-control tightening and potential regulatory friction. Nevertheless, the prevailing market appetite for picks-and-shovels plays in the AI hardware super-cycle continues to overpower these valuation and geopolitical overhangs, fueling strong intraday buying activity.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 8.446, indicating a buy signal. The RSI at 68.591 suggests neutral condition and the Williams %R at 12.172 suggests overbought condition. Please monitor closely.

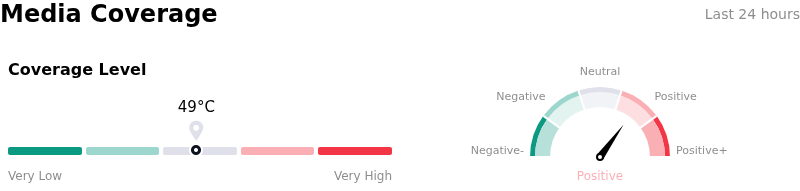

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $330.24, a high of $450.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Extreme Valuation Stretch: Following its recent rally, LRCX trades at an elevated trailing P/E exceeding 72x, far above its five-year historical median of 23x. Analysts caution that the stock is priced for perfection, requiring 26% annual revenue growth over the next five years to justify current levels, leaving it highly vulnerable to profit-taking and multiple compression.

- Decelerating System Shipment Growth: Structural concerns have emerged regarding a sharp projected deceleration in system shipment growth, which is expected to plummet to just 3% in 2026 from 82% in 2025 due to cyclical cooling in the NAND memory and China logic markets.

- High Geopolitical and Export Vulnerability: China generates approximately 34% to 35% of Lam's total revenue. This deep regional exposure leaves the company highly vulnerable to severe top-line volatility and potential market share impairment from expanding U.S. export controls and sudden revocations of shipment authorizations.

- Slowing Customer Prepayments and Insider Selling: Market anxiety has been compounded by customer down payments falling to their lowest levels in years, signaling a potential cyclical turn. This coincides with a Form 4 filing disclosing that Director Eric Brandt divested 54,500 shares totaling over $19.1 million, triggering fears of insider selling at a near-term valuation peak.

Recommended Articles