Disney: Can Recreate Netflix’s 10X Growth Miracle in a Decade?

Imagine walking through the Magic Kingdom at Disneyland, with Donald Duck’s laughter echoing in your ears and Cinderella’s Castle shining in the sunset. As you relax in a Moana-themed restaurant, eating a Mickey-shaped ice cream and streaming your favorite movie on Disney+, have you ever wondered if this empire, which draws 1.4 billion dream-chasing visitors annually and turns fantasies into reality, could once again utilize the magic of streaming and its unmatched IP dominance to replicate Netflix’s tenfold growth miracle in the next decade?

Source: TradingView

If Netflix achieved a tenfold stock price surge over a decade by continuously refining its business model and optimizing operational efficiency, then for Disney’s streaming platform, which has just reached the milestone of profitability, perhaps everything is only just beginning.

.png)

.jpg)

Source: Macrotrends, Disney

Disney Streaming: From Fairy Tale Magic to a Money-Making Empire

Since its launch in 2019, Disney+ has rapidly risen to become a new pillar of Disney’s business empire. By bundling Disney+, Hulu, and ESPN+, Disney has crafted an entertainment castle with over 200 million users, spanning all age groups.

Disney+: Disney+ is the grand hall of this castle, housing the sparkle of Cinderella’s glass slipper, Simba’s brave roar in The Lion King, Elsa’s “let it go” in Frozen, Iron Man’s thrilling flights in The Avengers, and the cultural shock of Wakanda in Black Panther. These exclusive IPs not only ignite childhood memories but also form a unique commercial moat. With 1.25 billion subscribers and still growing rapidly, Disney+ boasts a moat built on exclusive IPs that significantly enhances user retention. Beyond monthly subscription fees, Disney+ generates revenue through merchandise sales and theme park synergies. As its user base expands, its earning potential will only grow stronger.

Hulu: Hulu is like the adult-exclusive library within the castle, with 52 million users and 2024 revenue soaring to $12 billion, up 7.4%. From Daenerys’ commanding conquests in Game of Thrones to the apocalyptic human drama of The Walking Dead, and provocative films like Parasite and Joker, Hulu captivates audiences with gripping adult content. Its dual revenue model of ads and subscriptions, backed by Disney’s robust support, ensures Hulu’s profitability is solid.

ESPN+: ESPN+ is the castle’s arena, a pilgrimage site for sports fans with 25.6 million paid subscribers, up 53% year-over-year. From the electrifying moments of the NBA Finals to Tom Brady’s clutch Super Bowl passes and Conor McGregor’s brutal UFC knockouts, ESPN+ fuels fans’ passion with live events and original content. With subscription revenue (ARPU rising from $5.34 to $6.14), advertising income (ESPN’s overall ad revenue grew 17% in 2024), and emerging sports betting (ESPN Bet), its growth potential is vast.

These three platforms don’t operate in isolation; their bundled subscription strategy creates a synergy that spans children, adults, movie fans, and sports enthusiasts. In fiscal 2024, Disney’s streaming business turned profitable for the first time, marking a shift from heavy investment to sustainable growth. Leveraging its unparalleled IP assets and cross-platform synergy, Disney has built an entertainment ecosystem that’s nearly impossible to replicate. This strategy has solidified Disney’s position in the streaming wars, even beginning to encroach on competitors’ market share.

The Magic Accelerator to Catch Up with Netflix

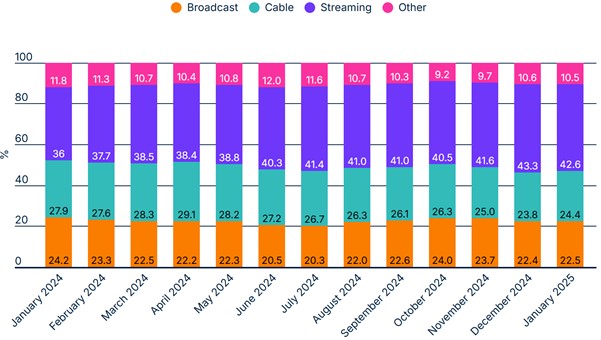

With the widespread adoption of mobile devices and faster internet speeds, users are increasingly turning to streaming services for content consumption, moving away from traditional broadcast or cable television. This behavioral shift has driven sustained growth in both the user base and viewing time of streaming services, laying a strong foundation for the future development of Disney’s streaming business.

Source: Nielsen

Under this robust long-term growth trend, whether Disney can continue to expand its operating margin is a critical focus for investors. By creating compelling exclusive content, curbing password sharing, integrating Hulu and ESPN+ services, and introducing ad-supported packages, Disney’s streaming business achieved profitability for the first time in the fourth quarter of 2024. To further enhance profitability and catch up to Netflix’s operational efficiency, investors should closely monitor progress in the following areas:

Growing Subscriber Numbers: In the future, Disney can attract more users by developing additional exclusive IP content, offering bundled packages of Disney+, Hulu, and ESPN+, and optimizing personalized recommendations and multi-device experiences, particularly in high-potential markets like Asia and Latin America.

Optimizing Pricing Strategies: Disney can refine its pricing strategies through tiered pricing, dynamic price adjustments, bundling Disney+, Hulu, and ESPN+ services, and cracking down on password sharing. These measures can significantly boost average revenue per user (ARPU), directly improving operating margins.

Expanding Advertising Revenue: The success of ad-supported packages demonstrates Disney’s ability to increase revenue without significantly raising costs. As the subscriber base grows, optimizing ad models across Disney+, Hulu, and ESPN+ and leveraging precision targeting technology will make advertising a key contributor to operating margin growth in the future.

Launching New Services: Disney is set to launch its “Flagship” direct-to-consumer (DTC) sports streaming service in Fall 2025. The platform will encompass all content from ESPN’s U.S. linear cable channels (e.g., ESPN, ESPN2, ESPNEWS), including live and on-demand programming, alongside the existing ESPN+ catalog of exclusive events and shows. Additionally, it will integrate innovative features such as ESPN Bet sports betting, event ticket sales, merchandise purchasing, aiming to deliver a comprehensive sports entertainment experience tailored for younger, digitally-savvy audiences.

Cost Management: Disney has successfully transitioned its streaming business from losses to profitability, indicating significant cost control in content production and operations. Moving forward, Disney still has substantial room to optimize content spending and operational efficiency to further boost margins.

Disney’s Streaming Magic: How High Could Its Stock Soar in Three Years?

Let’s hit the fast-forward button and envision the future of Disney’s streaming business. Disney’s streaming operations (Disney+, Hulu, ESPN+) have just turned profitable, with an operating margin of around 1% in Q4 2024, while streaming giant Netflix boasts a towering 30% margin. The gap may seem vast, but for Disney, it’s a blue ocean brimming with opportunity. Armed with an unrivaled IP treasure trove, a global user base, and a multi-pronged profitability strategy, Disney is accelerating its pursuit, potentially delivering exhilarating returns over the next three years.

Assuming Disney’s streaming business revenue climbs at a 10% compound annual growth rate, while non-streaming businesses (including theme parks, films, etc.) grow steadily at 3% for both revenue and operating income, we can outline three scenarios to showcase the potential leap in Disney’s stock price.

Scenario 1: Steady Growth

If Disney boosts its streaming business operating margin to 15% over the next three years—a reasonable and achievable target, driven by exclusive content, advertising revenue growth, and cost optimization—and pairs it with a conservative 30x price-to-earnings (PE) ratio, Disney’s stock price is projected to reach $106.

Scenario 2: Accelerated Sprint

If Disney pushes further, leveraging precise pricing adjustments, password-sharing restrictions, and new services like Venu Sports to elevate its streaming margin to 20%, and combines this with a moderate 40x PE ratio, the stock price could soar to $154.

Scenario 3: Miraculous Revival

In the most optimistic scenario, if Disney’s streaming business mirrors Netflix’s efficiency, achieving a 30% operating margin through surging global subscribers, explosive advertising revenue, and the success of new services, and earns a market-favored 50x PE ratio, Disney’s stock price could skyrocket to $221.

Recommended Articles