Sandisk Stock Is Up More Than 3,700% From Its 52-Week Low. Is the Memory Rally Still Investable, or Is This Stock Priced for Perfection?

Key Points

Western Digital spun Sandisk off in February 2025.

Sandisk is a leader in NAND flash storage solutions for hyperscale data centers.

Its revenue and profitability are accelerating at triple-digit percentage rates, yet the company still trades at a modest valuation.

- 10 stocks we like better than Sandisk ›

Sandisk (NASDAQ: SNDK) became a stand-alone public company again in early 2025 when it was spun out from Western Digital (which had acquired it in 2016). The separation was intended to position Sandisk's management to concentrate its resources and focus on NAND flash memory and enterprise-grade solid-state drives (SSDs) at a time when hyperscalers were sharply accelerating capital spending on artificial intelligence (AI) infrastructure.

That meant that Sandisk could more easily accelerate capacity expansions and technology road maps tailored specifically to the explosive storage requirements of large language model (LLM) training and inference deployments.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

At the time of this writing, Sandisk stock trades at $1,539 -- a gain of roughly 3,748% from its 52-week low of $40 per share. The magnitude of this move inevitably prompts the question of whether the market has already priced the most optimistic upside scenario for Sandisk into its stock or whether meaningful appreciation potential remains.

Image source: The Motley Fool.

Analyzing Sandisk's business amid the AI memory supercycle

Sandisk designs, manufactures, and sells NAND flash memory chips and the SSDs built from them. These products serve as the high-speed storage layer that AI systems rely on to hold training data and real-time inference outputs. As generative AI workloads scale up, the volume of data that must be stored and accessed has grown at a much faster pace than traditional enterprise or consumer storage demand ever did.

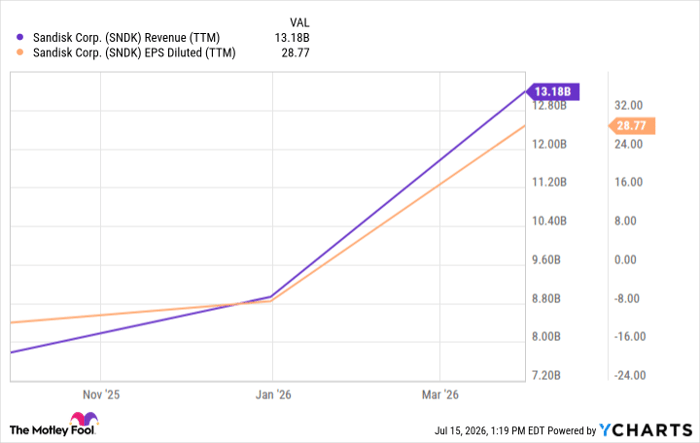

The result has been a memory supercycle in which both chip sales volumes and average selling prices are rising in tandem. Memory supplies are now far short of demand, and prices have soared. Sandisk's data center revenue and earnings per share (EPS) are growing at triple-digit percentage rates year over year, underscoring the company's operating leverage and improving gross margins as the adoption rates for AI surge toward ongoing compute capacity limits.

SNDK Revenue (TTM) data by YCharts. TTM = trailing 12 months. EPS = earnings per share.

Storage demand is becoming more secular

During Sandisk's most recent earnings call, management told investors that the company had signed a series of multiyear supply contracts worth $42 billion. These agreements lock in sales volumes and prices, and provide Sandisk with clear revenue visibility well into the latter half of the decade.

Because the contracts are tied to the multiyear build-out of AI data centers rather than to a short-term device upgrade cycle, Sandisk's order book appears stable. That's a notable contrast to the boom-and-bust pattern that has historically plagued memory and storage producers. Investors can view the current demand surge as more secular and durable than transitory.

Sandisk stock could continue soaring

So far this year, Sandisk stock has rocketed upward by 563% -- making it the top performer in the Nasdaq-100 by a mile. With that said, smart investors understand that absolute percentage gains reveal very little about a company's valuation.

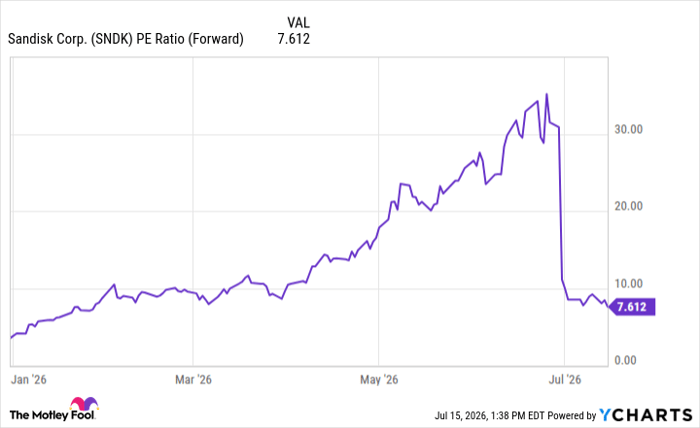

For the current fiscal year, Wall Street analysts estimate that Sandisk will report $66.51 in EPS. However, by next fiscal year, the consensus forecast points to a meaningful step change in profitability, with EPS expected to reach $208.22. On that basis, Sandisk trades at a modest forward price-to-earnings (P/E) multiple of just 7.6.

SNDK PE Ratio (Forward) data by YCharts. PE Ratio = price-to-earnings ratio.

In my view, Sandisk is set up for further valuation expansion based on a straightforward premise: AI infrastructure spending is projected to reach trillions of dollars annually over the next several years, and high-bandwidth memory (HBM) and storage form one of the indispensable pillars of that build-out. This positions Sandisk's earnings base to continue compounding through the combination of chip volume growth, pricing power, and operating leverage.

While periods of consolidation and sharp pullbacks in the stock are likely, any material decline would simply reset the entry point for a company whose AI-driven trajectory remains intact. On that basis, I see Sandisk as a compelling stock to buy and hold rather than as a name to exit in the wake of its tremendous rally.

Should you buy stock in Sandisk right now?

Before you buy stock in Sandisk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sandisk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $397,351!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,304,257!*

Now, it’s worth noting Stock Advisor’s total average return is 934% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 17, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Western Digital. The Motley Fool has a disclosure policy.

Recommended Articles