3 Reasons to Buy Novo Nordisk Stock

Key Points

Novo Nordisk has several pipeline candidates that will help improve its position in its core market.

The company's margins are excellent compared to its peers.

Novo Nordisk prioritizes returning capital to shareholders.

- 10 stocks we like better than Novo Nordisk ›

Novo Nordisk (NYSE: NVO) has faced significant challenges over the past couple of years. The company lost its lead in the weight-loss market to its biggest rival, Eli Lilly (NYSE: LLY), its financial results have been mediocre at best, and it has faced clinical setbacks for otherwise promising pipeline candidates. Given all that, it's not surprising that Novo Nordisk's shares have declined by more than 60% over the past 24 months. However, investing in Novo Nordisk while the stock is down may be a great idea, given solid reasons to expect a rebound. Here are three arguments in favor of a bull case for Novo Nordisk.

Image source: The Motley Fool.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

1. An attractive pipeline

One major obstacle Novo Nordisk faced concerned its next-gen anti-obesity medicine, CagriSema. Though it looked like a smashing clinical success and posted solid weight-loss efficacy numbers in phase 3 studies, it fell short of the 25% mean weight loss management had hoped for. On top of that, it failed to demonstrate non-inferiority to Eli Lilly's Zepbound in a head-to-head study. CagriSema will almost certainly earn approval, but it won't allow Novo Nordisk to take the lead back from Eli Lilly.

Other candidates in Novo Nordisk's pipeline might get it closer to that goal. One of them is Amycretin, which is a medicine that mimics two gut hormones: GLP-1 and amylin. The dual pathway approach has proven highly effective, as Zepbound has demonstrated. Further, whereas CagriSema combines two separate drugs, making it more complex to fine-tune for efficacy and manufacturing, Amycretin is a single molecule that activates two pathways that can induce weight loss through appetite control.

Amycretin could be more effective and easier to manufacture at scale than CagriSema for those reasons. Amycretin is undergoing phase 3 studies in subcutaneous and oral formulations. Strong results could send Novo Nordisk's shares soaring. Then there is UBT251, a medicine that mimics the actions of three gut hormones, which Novo Nordisk licensed from a China-based company. This medicine has already posted strong phase 2 results in weight loss and diabetes, albeit those were from studies conducted in China.

Still, UBT251 looks promising, and, together with Amycretin and several other candidates in Novo Nordisk's pipeline, could eventually help the company regain some share in the GLP-1 market.

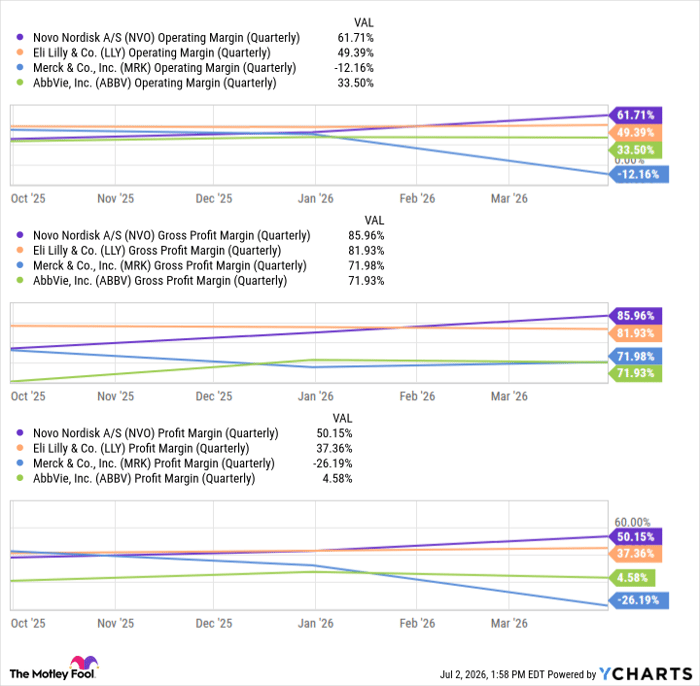

2. Excellent margins

Novo Nordisk boasts some of the strongest margins among its similarly sized peers.

NVO Operating Margin (Quarterly) data by YCharts

The company has achieved industry-leading margins thanks to several factors. Here are two of them. First, the company's strong position in the diabetes and weight-loss market grants it pricing power. Second, the Denmark-based pharmaceutical leader sells medicines that patients stay on for years, especially those with diabetes. Diabetics can take drugs like Ozempic indefinitely, since it is a lifelong disease. This means stable, recurring, predictable, almost subscription-like revenue. Even as Novo Nordisk has lost some ground to Eli Lilly, it continues posting strong margins. And as the company launches new products in its core therapeutic areas, we could see Novo Nordisk improving on that front.

3. Returning capital to shareholders

Novo Nordisk is an attractive stock to consider for income seekers. The company currently offers a forward yield of 3.6%, which is well above the S&P 500's average of 1.1%. Further, the company's annual dividend has increased consistently, rising almost 145% over the past decade. Even with the struggles it has encountered lately, the company's dividend looks safe. And on top of that, Novo Nordisk has a solid share repurchase plan in place. In other words, the company prioritizes returning capital to shareholders, which is another good reason to consider the stock.

Buy and forget

Novo Nordisk may still face some headwinds as more drugmakers seek to enter the GLP-1 market. The company could also encounter more clinical setbacks. But overall, Novo Nordisk's prospects look strong. There is always the possibility that investigational medicines will fail in the clinic; that's why the leading drugmakers have deep pipelines -- and Novo Nordisk has plenty of diabetes and weight-loss candidates beyond those we have discussed. And additional competition won't sink the company's business. It has not dominated the diabetes market for about a century by accident. Besides, the GLP-1 space is projected to grow rapidly and will accommodate multiple winners. For all those reasons (and more), it's worth it to buy shares of Novo Nordisk and hold onto them for a while.

Should you buy stock in Novo Nordisk right now?

Before you buy stock in Novo Nordisk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Novo Nordisk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $409,970!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,200,223!*

Now, it’s worth noting Stock Advisor’s total average return is 916% — a market-crushing outperformance compared to 210% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of July 7, 2026.

Prosper Junior Bakiny has positions in Eli Lilly and Novo Nordisk. The Motley Fool has positions in and recommends AbbVie, Eli Lilly, Merck, and Novo Nordisk. The Motley Fool has a disclosure policy.

Recommended Articles