【US Pre-Market】Memory Chip Sector Stages Collective Rebound, DRAM ETF Rises Nearly 7% With SK Hynix ADR Impending

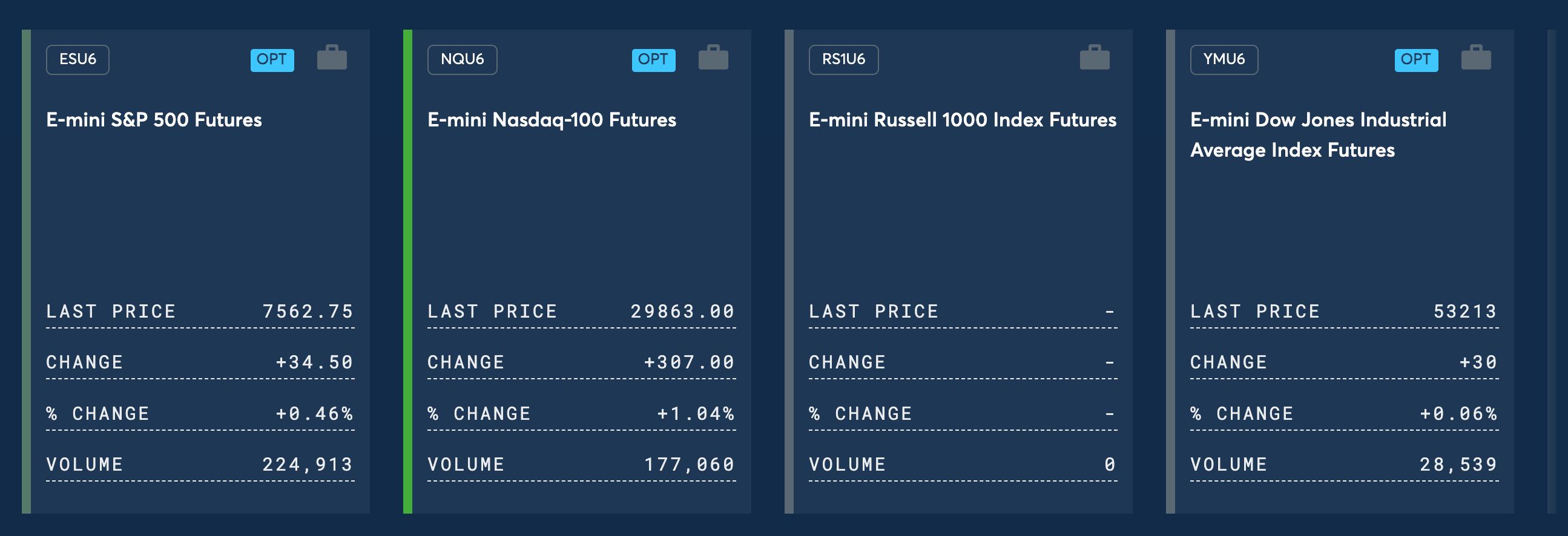

TradingKey - On July 6, Eastern Time, in pre-market trading, the three major U.S. stock index futures rose collectively, led by the technology sector. As of press time, Nasdaq 100 Index futures rose 1.05%, S&P 500 Index futures rose 0.46%, and Dow Jones Industrial Average futures rose 0.07%.

[Source: CME Group]

In commodities, gold and silver prices extended last week's gains. As of press time, spot gold ( XAUUSD) was trading around $4,150/oz; spot silver ( XAGUSD) was trading around $62.07/oz. In international oil prices, WTI crude oil futures were at $68.34/barrel, and Brent crude oil futures were at $71.72/barrel.

In the crypto market, Bitcoin (BTC) was trading around $62,950, and Ethereum (ETH) was trading around $1,770. The US Dollar Index was hovering around 101.07.

Market Volatility

The semiconductor storage sector rebounded collectively in pre-market trading. DRAM ETF rose nearly 7%, SanDisk ( SNDK ), Western Digital ( WDC ), and Seagate Technology ( STX) rose over 4%, while Micron Technology ( MU) rose over 2%.

The semiconductor sector broadly moved higher. Intel ( INTC) rose over 3.5% pre-market; on the news front, the company raised retail prices for some of its consumer-grade and server-grade CPUs, with consumer products increasing by about $30 to $50, and server products by hundreds to thousands of dollars.

The optical communications sector rebounded slightly pre-market. Marvell Technology ( MRVL) rose nearly 4%, while Corning ( GLW) and Coherent ( COHR) rose over 1%.

Computing power rental service providers edged higher pre-market. Oracle ( ORCL) rose over 3%, Nebius ( NBIS) rose over 2%, and Google ( GOOGL) and Microsoft ( MSFT) followed suit.

Mega-cap tech stocks generally gained pre-market. Meta ( META) and Tesla ( TSLA) rose over 1.5%, SpaceX ( SPCX) and Amazon ( AMZN) rose over 1%, while Apple ( AAPL) fell 0.96%.

Market News

Goldman Sachs ( GS) calls for an oversold rebound, opening a recovery window for the chip sector. The latest report from the Goldman Sachs trading desk points out that momentum stocks, which previously led the market rally, have shown preliminary dip-buying signals, leaving tactical room for a short-term rebound. In this cycle, the momentum factor has experienced a cumulative peak-to-trough decline of 24%, marking its largest drawdown since the first quarter of 2023 and far exceeding the historical average adjustment of 12%. Institutions judge that this major sell-off is not an absolute reversal of AI industry fundamentals, but rather a short-term amplification of volatility caused by quiet summer trading and insufficient liquidity. However, Goldman Sachs also warns of risks: positioning in momentum stocks remains highly crowded, and if market deleveraging continues, the subsequent maximum drawdown could reach twice the current decline.

SK Hynix to list on Nasdaq this Friday, with its $28 billion IPO taking center stage. SK Hynix is expected to list on Nasdaq on Friday, July 10, with its listing plan of over $28 billion potentially becoming the largest US IPO by a foreign company in history. SK Hynix is trading at 6.2 times its expected earnings for the next 12 months, lower than Micron Technology's valuation level of approximately 7 times. The listing is expected to narrow the valuation discount, allowing investors to directly trade this leading HBM play.

Samsung Electronics to release Q2 preliminary earnings tomorrow, with profit expected to hit an all-time high. Samsung Electronics will release its preliminary second-quarter earnings report this Tuesday (July 7). Wall Street generally expects that, driven by robust demand for AI memory chips (HBM) and continuously rising DRAM prices, Samsung Electronics' preliminary second-quarter profit will reach a record high. Following Samsung and SK Hynix's joint announcement in late June of a domestic investment plan exceeding 4,800 trillion Korean won, the market will closely monitor this earnings report for guidance on subsequent capital expenditure and capacity expansion.

Anthropic to invest $15 billion in Australia to deploy 1.4GW of computing power, as the AI infrastructure arms race escapes US domestic bottlenecks. According to Australian media reports, Anthropic plans to construct at least 1.4GW of data center computing resources in Australia, representing an infrastructure investment of $15 billion, with a target of having at least 1GW operational by the end of next year. This move comes against the backdrop of power shortages and community resistance faced by domestic data centers in the US, with Blackstone's QTS recently terminating a large-scale project in Virginia. Anthropic signed a Memorandum of Understanding on AI safety research with the Australian government in March this year. The company's annualized revenue has surged from $9 billion at the beginning of the year to over $44 billion, with its valuation soaring to $965 billion, and it has already filed for an IPO.

Key Events Calendar

Time | Event |

July 6, 10:00 AM ET | US June ISM Non-Manufacturing PMI |

July 7, Seoul Time | Samsung Electronics releases Q2 preliminary earnings (expected profit to hit a historic high) |

July 9, ET | PepsiCo ( PEP) Earnings |

July 10, ET | SK Hynix Nasdaq Listing; Delta Air Lines ( DAL) Earnings |

The semiconductor sector has found a breathing window after last week's intense sell-off. Goldman Sachs' short-term buy-the-dip signal has injected confidence into the market, but crowded positioning and liquidity risks remain underlying concerns. With economic data relatively light this week, market focus may center on the SK Hynix IPO and earnings from consumer giants. How far the rebound can go will depend on the speed and breadth of the subsequent recovery in market sentiment.

Recommended Articles