Is This Quantum Computing Stock a Buy Before the Sector's Next Major Catalyst?

Key Points

IBM CEO Arvind Krishna expects to see the first examples of quantum advantage in 2026.

As one of the leading quantum computing companies, IonQ would benefit from this.

IonQ is improving financially and rates highly with analysts, but it's expensive and risky.

- 10 stocks we like better than IonQ ›

The quantum computing industry is soaring after the Department of Commerce announced plans to provide $2 billion in federal incentives to nine quantum companies. IonQ (NYSE: IONQ) wasn't on the list, but it was the first publicly traded pure-play quantum computing company and has seen its share price increase 56% on the year (through May 28).

IonQ is arguably the most successful pure-play quantum company, too, as it was the first to surpass $100 million in annual revenue. Even though it's already up big, there's another major catalyst that could lift the entire industry higher this year.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

Quantum advantage in 2026

In a first-quarter earnings call, IBM CEO Arvind Krishna said he believes the company's partners will achieve the first examples of quantum advantage this year. The computing giant has also launched an open community quantum advantage tracker, where researchers can collect, validate, and compare results.

While there's no strict definition of quantum advantage, it generally refers to a demonstration that a quantum computer can solve a commercially relevant problem faster than a classical computer. This would essentially serve as validation for the entire quantum computing industry, as at the moment, there are still questions about its commercial applications.

IonQ would benefit the most if it were the company to demonstrate quantum advantage. Even if it weren't, this development would still likely boost all quantum computing stocks. If one company demonstrates quantum advantage, competitors will likely be able to do the same in time.

However, there's no guarantee quantum advantage will happen in 2026 or at all. Commercial uses for quantum systems are still largely theoretical. That's one of a few notable risks of investing in IonQ.

Why IonQ is a high-risk investment

Like other quantum computing pure plays, IonQ hasn't reached profitability yet. Its adjusted earnings before interest, taxes, depreciation, and amortization (EBIDTA) was a loss of $186.8 million in 2025 and $96.8 million in the first quarter of 2026. On a positive note, it had $3.1 billion in cash, cash equivalents, and investments as of March 31, enough to cover several years of operating expenses.

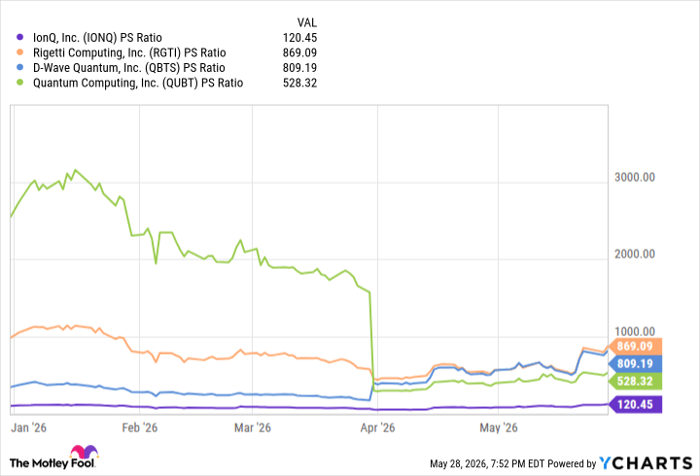

IonQ also has an extremely expensive valuation, trading at 120 times trailing sales. In fairness, its main competitors are even more expensive. Quantum Computing, Inc. trades at over 500 times trailing sales, while D-Wave Quantum and Rigetti Computing both trade at over 800 times trailing sales. IonQ is the better deal by this metric because of its higher revenue.

IONQ PS Ratio data by YCharts

But compared to other tech stocks, these quantum computing companies have stretched valuations. Nvidia trades at 21 times trailing sales.

IonQ is also betting on a specific approach to quantum systems based on a trapped-ion architecture. This has led to a notable advantage in accuracy over other quantum systems so far, including a 99.99% 2-qubit gate fidelity score -- meaning its system was 99.99% accurate. The downside is that trapped-ion quantum systems are much slower than systems using competing approaches, such as superconducting and photonics.

Accuracy is what matters most in quantum systems, so IonQ is in a good position. However, if other companies catch up, then processing speed could become more important, putting IonQ at a disadvantage.

Should you invest in IonQ?

IonQ is moving in the right direction financially. Revenue in Q1 2026 was $64.7 million, a 755% year-over-year increase and 30% higher than the midpoint of the expected range. Management also raised full-year revenue expectations to between $260 million and $270 million.

The analyst community rates IonQ highly, with most considering it a strong buy. However, the 12-month price target is $67.64, below the company's share price at the time of this writing, suggesting the price may have outrun analyst expectations.

Although I believe IonQ is the most interesting pure-play quantum company, I'm hesitant to invest right now, given its price appreciation and volatility. If you want to add IonQ to your portfolio, consider starting with a small position and gradually adding to it over time. It could continue to outperform, especially if quantum advantage becomes a reality this year, but there's also a good chance of a pullback that results in a better buying opportunity.

Should you buy stock in IonQ right now?

Before you buy stock in IonQ, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and IonQ wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $463,900!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,294,401!*

Now, it’s worth noting Stock Advisor’s total average return is 978% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of June 1, 2026.

Lyle Daly has positions in Nvidia. The Motley Fool has positions in and recommends International Business Machines, IonQ, and Nvidia. The Motley Fool has a disclosure policy.

Recommended Articles