Is This Ultimate High‑Yield Stock Actually Going to $0?

Key Points

Conagra makes packaged food products, which is normally a fairly reliable business model.

The company's portfolio of brands isn't industry-leading, and the company isn't performing well right now.

- 10 stocks we like better than Conagra Brands ›

For most investors, the main reason to look at Conagra (NYSE: CAG) today is likely the stock's shockingly high 9.8% dividend yield. That is way out of line with the average consumer staples stock's yield of 2.1%. Is this a huge opportunity, or is it a sign of risk?

Conagra's stock price probably won't fall all the way to zero. But investors will likely want to watch from the sidelines anyway. Here's why.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Conagra isn't an industry leader

Conagra owns brands you probably know, such as Slim Jim. However, when you step back and look at the full portfolio, it isn't really filled with industry-leading brands. In many ways, Conagra is a second-tier competitor. That's not a terrible thing, per se, but it increases risk because Conagra is following the consumer staples pack rather than leading it.

Notably, the company's financial performance has been weak. For example, after reporting a fairly strong fiscal third-quarter 2026 organic sales gain of 1.9%, the company said the full year would still be closer to break-even. And adjusted earnings would be at the low-end of management's guidance range of $1.70 to $1.85 per share. That means investors should expect a notable drop from the previous year's $2.30. In fiscal 2025, meanwhile, organic sales fell 2.9% and adjusted earnings dropped nearly 14%.

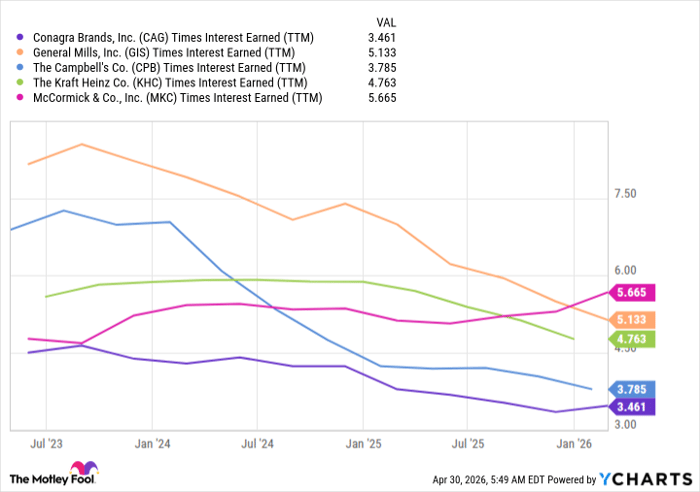

CAG Times Interest Earned (TTM) data by YCharts

If Conagra's adjusted earnings come in at $1.70, the bottom of management's guidance range, it will still cover its $1.40-per-share annual dividend. But there are other concerns to consider, such as the company's leverage, noting that its ability to cover its interest expenses is weaker than many of its packaged food peers. The company is actively working on debt reduction, but there's still more work to be done on the balance sheet. If push comes to shove, the dividend could end up being cut, just like it was in 2006 and 2017.

Conagra will survive, but a recession would likely hurt

It is highly unlikely that Conagra descends into bankruptcy anytime soon. However, changing consumer buying habits, belt-tightening consumers, energy price-driven margin compression, and the increasing risk of a recession are all big issues to consider before you buy this business.

Already struggling, Conagra would likely have an even more difficult time if the business environment worsened before it started to improve. Given the uncertainty in the market and the economy, such an outcome seems entirely possible. And that means conservative dividend investors should err on the side of caution, not take a risk on an industry laggard.

Should you buy stock in Conagra Brands right now?

Before you buy stock in Conagra Brands, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Conagra Brands wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $463,900!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,294,401!*

Now, it’s worth noting Stock Advisor’s total average return is 978% — a market-crushing outperformance compared to 211% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 31, 2026.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Recommended Articles