Intuitive Surgical Has Dropped 20% This Year. Wall Street Says It's Time to Buy.

Key Points

Shares of Intuitive Surgical have fallen more than 20% so far in 2026, leaving the stock mired in its own bear market.

The stock has seen drawdowns like this many times before.

- 10 stocks we like better than Intuitive Surgical ›

Intuitive Surgical (NASDAQ: ISRG) is a leader in the still-emerging field of surgical robotics in healthcare. It has 11,395 of its da Vinci systems installed worldwide. That total is up 12% year over year, so the company continues to grow its business at a rapid clip. But Intuitive Surgical is only a good choice for more aggressive growth investors. Here's why and why now could be a good time to jump aboard.

Wall Street likes Intuitive Surgical

Two-thirds of the 33 analysts who cover Intuitive Surgical have it as a buy or strong buy. Only one analyst has the medical device company rated a sell, with the rest calling it a hold. The average price target is 33% above the current stock price. In other words, there's a notable upside opportunity here.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Valuation-wise, Intuitive Surgical's price-to-sales, price-to-earnings, and price-to-book ratios are all below their five-year averages. So the stock looks cheap relative to its own history, which also hints that there could be upside opportunity in the stock.

There's just one small problem: Intuitive Surgical has a long history of being a highly valued, volatile stock.

Lots of big drawdowns

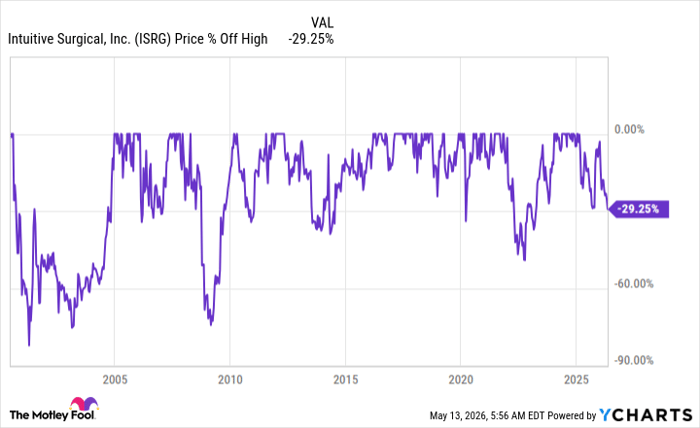

Intuitive Surgical is in the middle of a 20% drawdown, which means the stock is in its own bear market. That's a potential investment opportunity, but it has to be put into a broader context. For example, the stock has experienced at least eight drawdowns of a similar size since its initial public offering. If you can't handle that kind of volatility, you probably shouldn't own it.

ISRG data by YCharts

Meanwhile, the discounted valuation noted above is relative to Intuitive Surgical's own history. Just to use one measure, the P/E ratio is 52x today, compared to a five-year average of 70x. It is certainly cheaper than it has been, but the stock is still richly valued, noting that the S&P 500 index (SNPINDEX: ^GSPC) has an average P/E ratio of 26x. Value investors will not be interested, and neither will dividend lovers, given that the stock doesn't pay a dividend.

Intuitive Surgical has a great business, if you can stomach owning the stock

The truth is that Intuitive Surgical continues to grow its business at a rapid clip. And that doesn't seem likely to change anytime soon. But Wall Street knows this story well by now, so it is an expensive stock. It is also prone to volatile price swings. Buying during the current drawdown could be a great investment decision, but only if you are an aggressive growth investor who has the willpower to stick around for the long term.

Should you buy stock in Intuitive Surgical right now?

Before you buy stock in Intuitive Surgical, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Intuitive Surgical wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $472,205!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,384,459!*

Now, it’s worth noting Stock Advisor’s total average return is 999% — a market-crushing outperformance compared to 208% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

See the 10 stocks »

*Stock Advisor returns as of May 14, 2026.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Intuitive Surgical. The Motley Fool recommends the following options: long January 2028 $520 calls on Intuitive Surgical and short January 2028 $530 calls on Intuitive Surgical. The Motley Fool has a disclosure policy.

Recommended Articles